XLV spent August in consolidation, but its bullish pivot from early July is still intact. Similar to the Staples Sector it is a long-term underperformer which is overbought near-term. XLV registered more positive inputs in our model based on the broader outperformance at the industry level. That said we start September near benchmark weight in the XLV.

Price Action & Performance

In absolute terms, XLV is near-term overbought on price and has outperformed the S&P 500 since early July. That said, the sector remains in a long-term underperformance trend vs. the benchmark with only trace signals of bullish reversal. In this context, a near-term overbought signal is actually a welcome development.

At the industry level performance has been tepid. Over the trailing 12 months none of the industries has outperformed the S&P 500 though 4 of 5 have closed to within single digits of the index. Among them Biotechnology has been the best performer followed by the Providers & Services Industry. Over the past 3-months relative performance has improved at the Sector and Industry level, and we would expect any potential corrective action at the Index level to be a tailwind to the sector.

Given persistent underperformance at the sector level, strong health care stocks are few and far between. Our favorites are BSX, ISRG, PODD, HCA, UHS, VRTX, REGN and LLY. We are also constructive on ABBV, AMGN and UNH among the Mega Cap’s in the sector.

Economic and Policy Drivers

The emergence of GLP1 drugs has had a profound impact on the Healthcare sector. However, after 2+ years of dominance by manufacturers like LLY, there has been a shift in performance driven by expectations of interest rate policy easing. Easing typically drives a bid for stocks, industries and sectors. It remains to be seen how the XLV will react to the upcoming election. Historically there have been components of both party’s platforms that have been seen as tailwinds to the industry, whether Democratic candidates mandating universal coverage, or Republicans proposing to boost efficiency by allowing insurance companies prerogative over who they cover.

In Conclusion

We are near market weight in our XLV allocation for September. Model inputs have improved marginally, but the sustained consolidation in equity prices that typically catalyze performance for the sector have remained elusive. Our Elev8 Sector Model is OVERWEIGHT XLV with a +0.35% allocation vs. our benchmark S&P 500

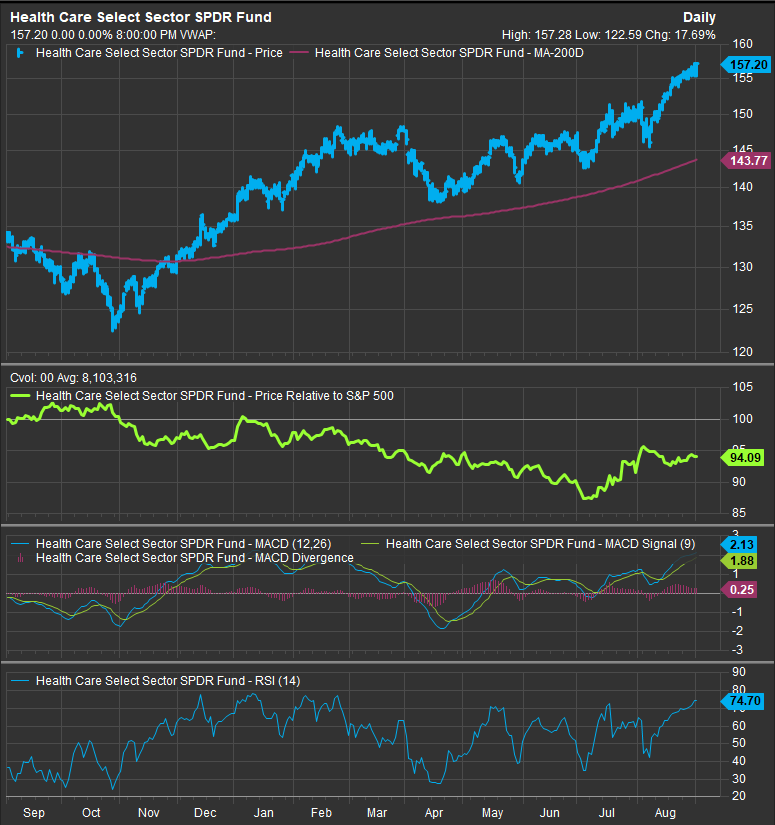

Chart | XLV Technicals

- XLV 12-month, daily price (200-day m.a. | Relative to S&P 500 | MACD | RSI)

- Finally seeing some evidence of bullish reversal on the chart, still not totally convinced

XLV Relative Performance | XLV Industry Level Relative Performance | 3m

- Strong Relative performance on improving industry level breadth is an encouraging sign

Data sourced from FactSet