XLP Consumer Staples SPDR June Outlook—Staples bottoming process relative to the broad market is still intact. The weaker seasonal period and the slowing consumer have us preferring XLP or XLY for June.

Price Action & Performance

XLP outperformed the S&P 500 Index in April on a monthly basis for the first time since October of 2023. May started with continuation of outperformance and ended with a pull-back as a lighter than expected inflation print spurred rotation into riskier assets. After 2-weeks of retracement the XLP popped again on the last day of May. The ongoing market debate between Growth, Inflation and Stagnation scenarios is unresolved. In the weaker summer seasonal period we have a modest preference for defensive exposures to complement our bigger OW’s in XLC, XLK and XLI.

Economic and Policy Drivers

Inflation is a dominant theme across all sectors, but with very different implications. XLP outperformance would likely be driven by a hotter inflation print and a more Hawkish Fed. This may seem counter-intuitive, but the more Hawkish the Fed becomes, the more likely investors are to price in recession which would benefit low vol. sectors that historically act as defense. From an economic perspective, we are seeing signs of consumers trading down to more value-oriented spending. Strength in staples retailers like TGT, COST and WMT is reflective of this. May’s earnings releases from COST and WMT reflected this as more affluent consumer segments spent an increasing share of their budgets at the discount retail giants. This aligns with our own deep dive into the consumer which shows many important fundamental metrics deteriorating for the consumer. And we’ve seen this in discretionary areas of the stock market as well with Airlines, cruise-lines, homebuilders and assorted retail stocks weaker in the near-term on fading fundamental results.

How Can XLP Help?

XLP has several characteristics that make it attractive to investors when there is expectation of equity price correction, volatility, or economic decline into late cycle or recession. It is comprised exclusively of Large Cap. US stocks which generally offer a lower volatility profile to the broad market. It has one of the highest dividend yields among the 11 GICS sectors which offers income and stability when markets are falling on price. It also contains many of the companies that have been and would continue to benefit from a tightening consumer. TGT COST and WMT mentioned above are prominent weights in the Sector and have outperformed in 2024 in aggregate as well as in April. They are major beneficiaries of economic substitution. Personal products like toothpaste, soap, laundry detergent and deodorant are seen as non-cyclical products that people need regardless of recession. Food is clearly a necessary and Tobacco has very strong customer loyalty.

In Conclusion

Weak seasonals, an oversold entry point and a flagging consumer have us preferring a long position in XLP over XLY. We debut our Elev8 Sector Model with an OVERWEIGHT position in XLP of 1.98%

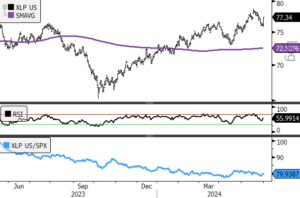

Chart | XLP Technicals

- XLP 12-month, daily price (200-day m.a. | Relative to S&P 500)

- Price and relative curves approach the weaker summer seasonal period from a better tactical position after a pull-back at the end of May