January 19, 2026

Rising tariffs alongside higher interest rates create a defensive problem that cannot be solved by simply rotating into Utilities, Real Estate, or broad Consumer Staples. In this regime, investors are not being compensated for yield or earnings stability alone. What the market has historically rewarded instead are pricing power, short cash-flow duration, balance-sheet flexibility, and inflation resilience. The practical question, then, is straightforward: if traditional low-vol sectors are compromised, what replaces them?

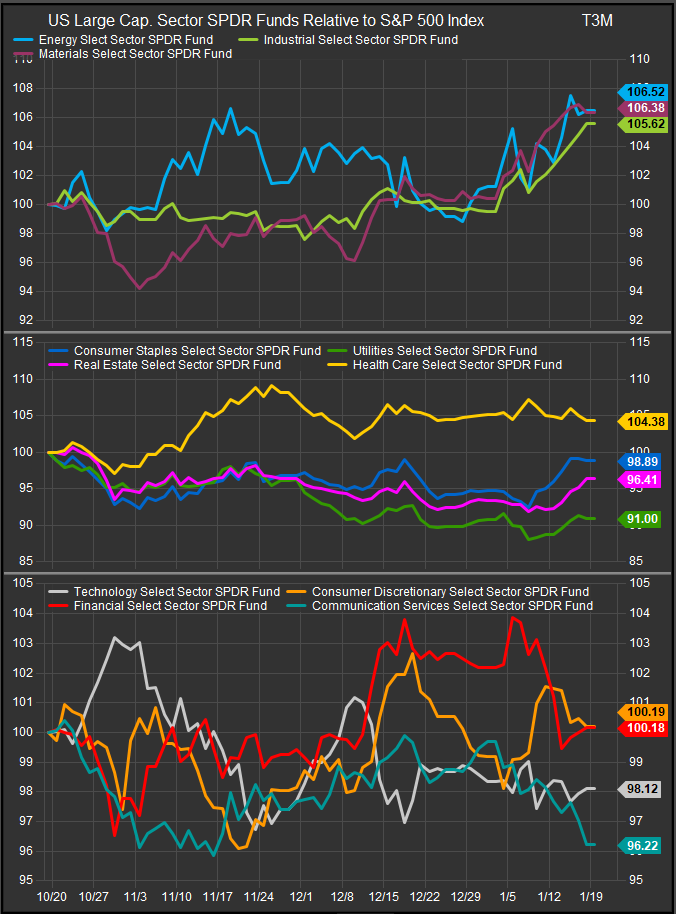

Chart: 11 sector SPDR funds vs. the S&P 500 index on a trailing 3-month basis.

The first place investors have historically found those characteristics is Health Care, particularly large-cap pharmaceuticals, managed care, and medical services. Health Care combines relatively inelastic demand with domestic revenue exposure and earnings streams that are far less dependent on interest-rate levels. Importantly, cash flows are realized in the near and intermediate term, not pushed far into the future, which reduces valuation sensitivity when rates rise. While supply chains can face cost pressure, Health Care has historically retained its defensive qualities in inflationary tariff regimes better than Utilities or REITs.

A second substitute for classic defensives has been select Industrials, not the globally exposed, capital-goods exporters, but domestically oriented segments with contractual pricing, government-backed demand, or infrastructure exposure. Defense, aerospace services, grid modernization, and industrial services businesses tend to exhibit steady demand and cost-pass-through mechanisms that protect margins. In tariff regimes, these areas benefit from reshoring incentives, fiscal support, and long-dated contracts that explicitly account for inflation. Historically, these “industrial defensives” have behaved more like stability assets than growth cyclicals when trade policy tightens.

Energy, particularly integrated and infrastructure-oriented exposure, has also served as a functional replacement for traditional low-vol sectors when tariffs are inflationary. Energy is not low volatility in a statistical sense, but it provides something Utilities and Staples cannot in this regime: protection against rising input costs and geopolitical supply risk. When tariffs reinforce inflation and disrupt global trade flows, Energy cash flows often adjust upward rather than being capped. Investors have historically been better served treating Energy as an inflation hedge that offsets the weaknesses of rate-sensitive defensives, rather than avoiding it altogether.

Within Financials, the traditional money-center banking exposure is often too cyclical for defensive use, but other parts of the sector have offered more resilient characteristics. Insurance—particularly property & casualty—has historically benefited from pricing cycles that respond positively to inflation, while asset managers with diversified fee streams and strong balance sheets can maintain earnings durability even as rates rise. These exposures lack the bond-proxy problem that undermines Utilities and REITs when yields increase.

Another important area is Communication Services, specifically businesses with subscription-based or usage-driven revenue models and limited physical supply-chain exposure. While advertising-sensitive platforms can be cyclical, telecom infrastructure and certain media distribution models have historically provided stable cash flows without the same degree of rate sensitivity seen in Utilities. In tariff regimes, these businesses tend to behave more defensively than headline volatility would suggest.

What unites these replacement defensives is not low beta, but economic characteristics. They share some combination of pricing power, domestic demand, contractual revenues, balance-sheet strength, and the ability to adjust to inflation. They are less reliant on yield substitution and less vulnerable to rising discount rates. As a result, they have historically provided better downside protection than Utilities, Real Estate, or broad Staples when tariffs and rates rise together.

The implication for investors is that defense in this environment must be intentional rather than traditional. Instead of buying low-volatility sectors by label, portfolios should be tilted toward Health Care, selective Industrials, Energy, parts of Financials, and stable segments of Communication Services—areas where earnings durability is supported by real economic leverage rather than by low rates.

In short, when tariffs are imposed and interest rates move higher, the defensive toolkit shifts. Utilities, Real Estate, and Staples lose their historical advantage. The better substitutes are sectors that can absorb inflation, reprice revenues, and generate cash today, not sectors whose defensive reputation was built in a world of falling yields and benign trade policy.

Data Sources

- U.S. International Trade Commission (USITC), Harmonized Tariff Schedule of the United States

- U.S. Census Bureau, U.S. International Trade in Goods and Services

- Federal Reserve, Beige Book (multiple editions referencing tariff cost pass-through)

- Federal Reserve Economic Data (FRED), Treasury yield and inflation expectation series

- S&P Dow Jones Indices, sector and factor total return histories

- Academic and sell-side research on 2018–2019 U.S.–China trade war market impacts (e.g., IMF, BIS, major investment bank strategy notes)

- Bloomberg, Reuters reporting on tariff policy, inflation dynamics, and sector performance during trade disputes

Additional data from this report was compiled through FactSet Research Systems Inc.