February 25, 2026

S&P futures are up 0.3% following Tuesday’s tech-led rally. Software (short covering), Mag 7, and semis drove gains, alongside strength in travel & leisure, homebuilders, credit cards, PE, and machinery. Banks, managed care, parcels/logistics, and energy lagged.

Overnight, Asia rallied sharply with Japan up over 2% on dovish BoJ nominations. Europe is higher by ~0.6%. Treasuries are weaker with yields up ~2 bp in the belly. The dollar is up 0.2%, again driven by yen weakness. Gold +0.3%, silver +2.8%, Bitcoin +1.4%, and WTI crude +0.4%.

The firmer tone comes despite softer guidance from Workday (WDAY), where FY27 subscription growth and margins disappointed, though some see conservatism under returning leadership. Software sentiment improved Tuesday following Anthropic’s enterprise event, where collaboration themes overshadowed displacement fears and pushback emerged against more deflationary AI scenarios cited earlier in the week.

Focus now shifts to NVIDIA (NVDA) earnings after the close, with expectations for another ~$2B beat and raise and continued strong demand commentary. Asia tech strength (notably South Korea) reinforces that optimism. Elsewhere, HP Inc. (HPQ) cited margin pressure from higher memory costs.

No major macro data this morning. Fed’s Barkin, Schmid, and Musalem are scheduled to speak. Treasury auctions $70B of 5-year notes today, with claims Thursday and PPI Friday (Street looking for +0.3% m/m headline and core).

Earnings & Corporate Highlights

Notable Gainers:

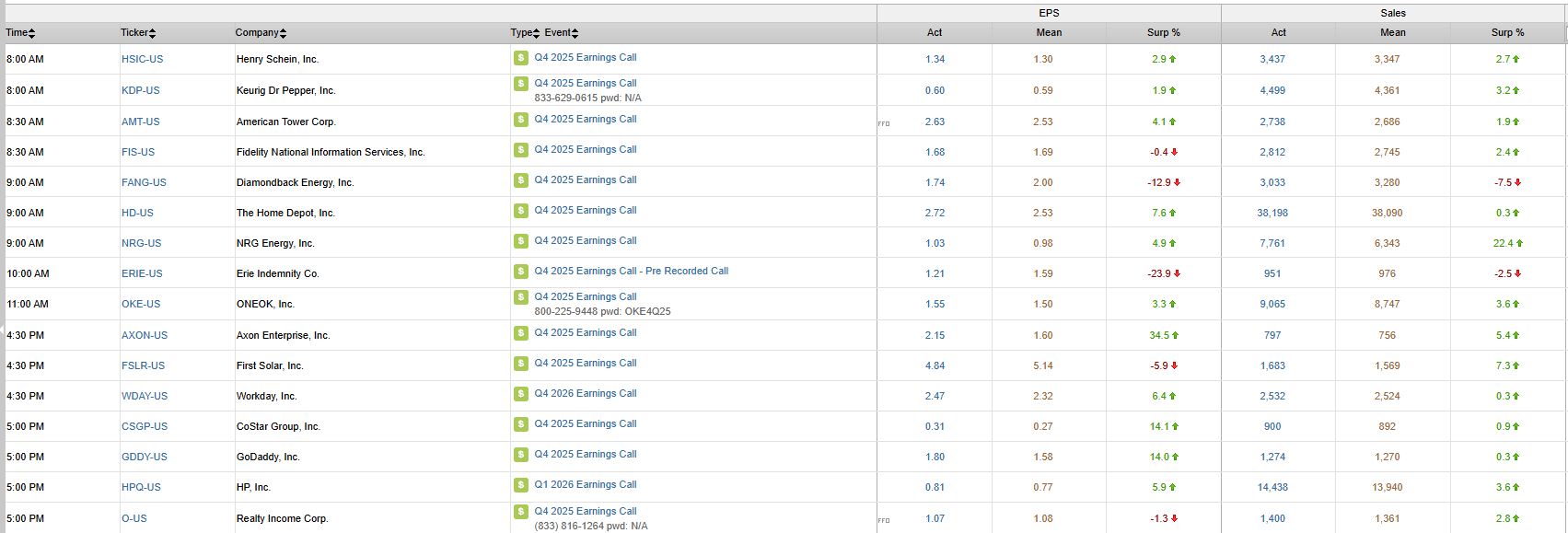

- Axon Enterprise (AXON) – Strong outlook (29% CAGR through FY28), AI traction highlighted.

- Cava Group (CAVA) – Positive brand momentum commentary.

Notable Decliners:

- Workday (WDAY) – Light FY27 subscription growth guide.

- Lowe’s (LOW) – Softer 2026 guidance.

- MercadoLibre (MELI) – Strong GMV/TPV but margin miss on investment spend.

- First Solar (FSLR) – Weaker margins and softer 2026 guide.

- CoStar Group (CSGP) – Sequential bookings decline, weaker Q1 guide.

- GoDaddy (GDDY) – Weaker outlook tied to product/marketing changes.

- Lucid Group (LCID) – Lower 2026 production guide.

- HP Inc. (HPQ) – EPS guided to lower end due to memory cost pressures.

Other Headlines:

- Anthropic reportedly eased some safety policies amid competitive pressures.

- Warner Bros. Discovery (WBD) said a new proposal from PSKY could be superior to the current bid from Netflix (NFLX).

Overall tone remains constructive ahead of NVDA earnings, with tech sentiment stabilizing after earlier AI-disruption-driven volatility.

U.S. equities rebounded Tuesday (Dow +0.76% | S&P 500 +0.77% | Nasdaq +1.04% | Russell 2000 +1.20%), finishing just off session highs as risk appetite improved following Monday’s AI-driven selloff. Treasuries were mixed with modest curve flattening; the 2-year yield rose 2 bp to 3.46% while the 10-year was unchanged at 4.03%. The Treasury’s $69B 2-year auction tailed slightly with lighter foreign demand. The dollar index rose 0.1%, driven by yen weakness after reports that Sanae Takaichi expressed concern to BOJ Governor Ueda about further tightening. Gold fell 0.9%, silver gained 1.1%, Bitcoin ended flat after dipping below $63K, and WTI crude declined 1%.

On the data front, February consumer confidence rose to 91.2 from 89.0, with improved labor-market differentials. ADP weekly private payrolls averaged 12.75K per week, marking a fourth straight increase. The Richmond Fed manufacturing index fell to -10.0, missing expectations. December FHFA home prices rose 0.1% m/m while Case-Shiller increased 0.5%. Wholesale inventories rose 0.2%, in line.

Fedspeak leaned cautious. Chicago Fed President Goolsbee said inflation progress has stalled and policy may not be clearly restrictive. Atlanta Fed’s Bostic warned structural employment pressures may not be solvable via rates alone. President Trump is scheduled to deliver his State of the Union address tonight, expected to emphasize economic strength and affordability initiatives.

Sector Highlights

Leadership rotated back toward growth and cyclicals. Consumer Discretionary (+1.58%), Industrials (+1.23%), Technology (+1.17%), Utilities (+1.09%), and Materials (+0.79%) led. Healthcare (-0.53%) and Energy (-0.11%) lagged, while Communication Services (+0.22%), Real Estate (+0.23%), Financials (+0.47%), and Consumer Staples (+0.69%) posted more muted gains. The rebound was driven largely by a software bounce and semiconductor strength, alongside solid showings in housing-related retail and machinery.

Information Technology

- Advanced Micro Devices (AMD) +8.8% after announcing a six-gigawatt AI compute agreement with Meta Platforms (META) potentially worth $100B+, with META holding an option to acquire up to 10% of AMD.

- Qualcomm (QCOM) +3.1% on upgrade citing underappreciated data-center opportunities.

- Keysight Technologies (KEYS) +23.1% on FQ1 beat and strong guidance.

- Ultra Clean Holdings (UCTT) +17.2% on improved WFE outlook.

- DigitalOcean (DOCN) +5.9% despite mixed EPS guide, highlighting long-term growth targets.

Consumer Discretionary

- Home Depot (HD) +2.0% after Q4 revenue beat (~5%) and unexpected +0.4% comp growth.

- Planet Fitness (PLNT) -9.0% on light FY26 guidance.

- Dillard’s (DDS) -7.8% on Q4 miss, citing winter storm disruption.

- Whirlpool (WHR) -13.9% after announcing $800M stock and convertible offering.

Healthcare

- Vir Biotechnology (VIR) +27.7% on positive Phase 1 data and $335M Astellas partnership.

- Novo Nordisk (NVO) -2.6% after announcing plans to cut U.S. GLP-1 prices up to 50%.

- Eli Lilly (LLY) -1.6% on competitive pricing concerns.

- Henry Schein (HSIC) +3.5% on earnings beat and solid guidance.

Financials

- PayPal (PYPL) +6.7% on reports Stripe is exploring acquisition interest.

- JPMorgan Chase (JPM) modestly raised 2026 NII guidance at analyst meeting.

- Citigroup (C) announced sale of 24% stake in Banamex for $2.5B.

Industrials

- BWX Technologies (BWXT) +3.0% on earnings beat and strong backlog growth (+50% y/y).

- Primoris Services (PRIM) -8.3% despite revenue beat, on margin concerns.

- Kratos Defense & Security Solutions (KTOS) -3.9% on softer Q1 guide.

Materials

- Westlake (WLK) +12% on Q4 earnings beat driven by profitability initiatives.

Tuesday’s session reflected a relief rally in software and semiconductors, constructive housing-related earnings, and improved risk sentiment ahead of key AI-related earnings later this week.

Eco Data Releases | Wednesday February 25th, 2026

No high-level releases scheduled for today

S&P 500 Constituent Earnings Announcements | Wednesday February 25th, 2026

Data sourced from FactSet Research Systems Inc.