March 8, 2026

The past week has forced investors to confront a macro regime that markets had largely managed to avoid for much of the cycle: the combination of geopolitical conflict, rising energy prices, and renewed inflation risk. Escalation between the United States, Israel, and Iran has injected a powerful supply shock into the global economy, with energy infrastructure under attack and the Strait of Hormuz effectively constrained. Oil prices surged more than 25% during the week, and analysts warned that crude could spike toward $150 per barrel if Gulf production disruptions persist. For equity investors, the immediate question is how these developments reshape sector positioning—and whether the recent rally in Growth stocks should continue or be faded.

The Macro Shock Favors Value—At Least Initially

Historically, energy-driven geopolitical shocks have tended to favor Value-oriented sectors. The logic is straightforward: higher oil prices feed directly into the earnings of Energy producers and commodity-linked industries while simultaneously pushing inflation expectations higher and lifting real yields. Rising discount rates typically pressure the valuation multiples of long-duration Growth stocks, particularly those concentrated in Technology and Communication Services.

This dynamic was evident in the immediate market reaction. Energy equities surged alongside crude prices, with Saudi Aramco posting its largest gain in nearly three years as supply disruptions intensified. Meanwhile, commodities-linked sectors—including Materials and Energy within the GICS framework—attracted heavy options activity as traders sought exposure to the tightening supply backdrop.

The energy shock also reverberates through other parts of the Value complex. Financials, particularly banks, often benefit from higher nominal yields that accompany inflation fears. Industrial companies tied to resource extraction, defense, and infrastructure may also see improved demand if geopolitical tensions remain elevated. These sectors collectively represent the core of the Value factor in equity markets.

But the Growth Narrative Is Not Dead

Despite the geopolitical turmoil, the structural forces supporting Growth sectors remain powerful. Artificial intelligence investment continues to dominate corporate capital allocation decisions, and the latest headlines reinforce the scale of that spending wave. Reports indicated that companies such as Broadcom and Marvell continue to guide for extraordinary data-center-related growth through 2027 and 2028, while firms like Anthropic and OpenAI are rapidly expanding their revenue run rates.

Even as the energy shock unfolded, software and semiconductor equities staged intermittent rebounds, supported by short covering and by investor confidence that AI-driven productivity gains remain intact. FactSet data show that Technology and Communication Services still account for the largest share of expected S&P 500 earnings growth over the coming year.

This resilience highlights the key difference between cyclical Value leadership and structural Growth leadership. Energy and commodity sectors benefit from supply shocks, but the Technology sector benefits from a long-term investment cycle that is largely independent of short-term geopolitical events.

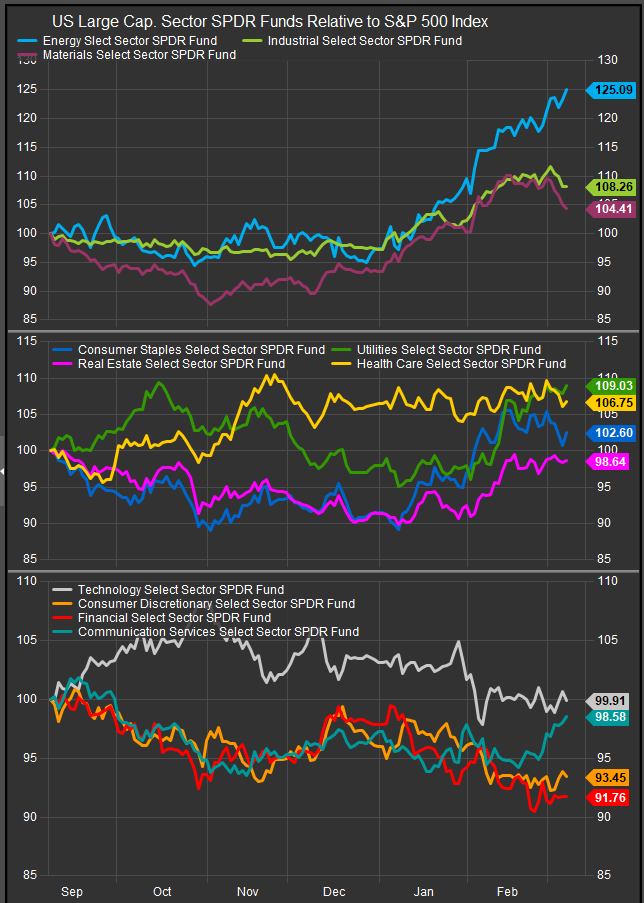

The Sector Map: Where Growth and Value Live

Understanding the Growth versus Value debate requires looking through the lens of sector composition.

Growth-oriented sectors are heavily concentrated in:

- Information Technology (semiconductors, software, cloud infrastructure)

- Communication Services (platform companies and digital advertising)

- Consumer Discretionary, particularly internet and e-commerce platforms.

These industries tend to have high margins, rapid revenue expansion, and significant sensitivity to interest-rate expectations.

Value-oriented sectors, by contrast, are typically concentrated in:

- Energy (oil producers, refiners, midstream infrastructure)

- Financials (banks, insurers, diversified financial institutions)

- Materials (metals, mining, chemicals)

- Industrials, particularly capital goods and defense manufacturers.

These sectors are more closely tied to the real economy, commodity cycles, and inflation dynamics.

The Iran conflict highlights how quickly the balance between these groups can shift. A spike in oil prices simultaneously boosts Energy earnings while increasing inflation risk—two developments that traditionally favor Value exposure.

Labor Market and Consumer Signals Complicate the Outlook

Beyond geopolitics, the economic data released during the week added further complexity to the macro picture. February payrolls unexpectedly declined by 92,000 jobs, and the unemployment rate rose to 4.4%. At the same time, wage growth remained firm at 0.4% month-over-month. That combination—weak employment but persistent wage pressures—raises the specter of a stagflationary environment. A stagflationary environment describes a macroeconomic situation where economic growth is weak or slowing, inflation remains elevated, and unemployment begins to rise simultaneously. It is considered one of the most difficult conditions for policymakers and investors because the usual policy tools that fix one problem can worsen the others.

Consumer behavior is also showing signs of caution. The Federal Reserve’s Beige Book highlighted increased price sensitivity and delayed large purchases, reinforcing concerns that higher energy costs could weigh on household spending in the months ahead.

For the Federal Reserve, this environment is challenging. Energy-driven inflation may limit the central bank’s ability to cut rates even as labor market momentum softens. Market pricing now suggests the Fed will remain on hold at the upcoming March meeting, with only two rate cuts expected later in the year.

Should Investors Buy Growth or Rotate to Value?

In the near term, the macro environment argues for caution toward the Growth rally. Rising energy prices, geopolitical risk, and renewed inflation concerns are classic ingredients for Value outperformance. If oil prices remain elevated and bond yields continue to rise, sectors such as Energy, Financials, and Materials could remain leadership areas.

However, investors should avoid assuming that Value will dominate indefinitely. Geopolitical shocks have historically produced only temporary disruptions to equity markets. Strategists note that the S&P 500 has historically been higher six and twelve months after major Middle East conflicts, reflecting the resilience of corporate earnings and global economic activity.

Ultimately, the trajectory of interest rates will determine which factor prevails. If energy-driven inflation pushes yields higher, Value sectors are likely to outperform. If the shock proves temporary and yields stabilize or fall, Growth sectors—particularly Technology and AI-related industries—could quickly regain leadership.

Where Do Low Volatility Sectors Fit Into This?

In a market defined by competing macro forces—geopolitical conflict, rising energy prices, and uncertainty around interest rates—low volatility sectors occupy an increasingly important middle ground between Growth and Value exposures. Sectors such as Utilities, Real Estate, Healthcare, and Consumer Staples typically exhibit lower earnings cyclicality and more stable cash flows, making them natural refuges when macro volatility rises.

From a factor perspective, these sectors tend to sit outside the traditional Growth–Value debate. They are not driven primarily by technological innovation or rapid earnings expansion, nor are they directly leveraged to commodity cycles or financial conditions in the way Energy or Financials are. Instead, their investment case rests on earnings stability, dividend income, and balance-sheet durability.

Utilities are perhaps the clearest example. The sector benefits from regulated revenue streams and relatively predictable demand, characteristics that tend to attract investors during periods of economic uncertainty. At the same time, Utilities are not entirely insulated from the current macro narrative. The accelerating buildout of AI infrastructure and data centers is significantly increasing electricity demand, creating a structural growth tailwind for power generation and grid infrastructure companies.

Real Estate occupies a more complex position. The sector struggled earlier in the cycle as higher interest rates pushed financing costs sharply higher. However, if economic growth slows and bond yields stabilize—or begin to fall—Real Estate investment trusts (REITs) could become attractive again due to their yield profile and sensitivity to declining interest rates. In that sense, Real Estate behaves as a hybrid between a defensive sector and an interest-rate proxy.

Healthcare and Consumer Staples also serve a stabilizing role in portfolios. Healthcare companies benefit from relatively inelastic demand tied to demographics and medical innovation, while Staples firms provide essential goods that consumers continue to purchase even when discretionary spending slows. These sectors often outperform when investors become more concerned about economic growth or when volatility rises across the broader market.

In the current environment, low volatility sectors function as a portfolio shock absorber. They provide diversification from both the macro-sensitive Value sectors and the rate-sensitive Growth sectors, helping to stabilize portfolio returns during periods of heightened uncertainty.

The Bottom Line: A Three-Way Allocation Framework

The current investment landscape is best understood not as a binary contest between Growth and Value, but as a three-way allocation framework that includes defensive, low-volatility sectors.

Geopolitical tensions and surging oil prices create a favorable backdrop for Value sectors, particularly Energy, Materials, and parts of Industrials. These industries benefit directly from commodity price strength and inflation-linked revenue streams.

At the same time, the long-term investment cycle around artificial intelligence and digital infrastructure continues to support Growth sectors, especially within Information Technology and Communication Services. These companies remain the primary drivers of earnings growth for the broader equity market.

Low volatility sectors—including Utilities, Real Estate, Healthcare, and Consumer Staples—serve as the stabilizing third pillar. In periods of heightened macro uncertainty, they offer reliable cash flows, defensive earnings profiles, and attractive dividend yields.

For investors, the implication is clear. Rather than making an aggressive bet on one factor dominating the next phase of the cycle, a balanced portfolio may be the most effective approach. Exposure to Growth captures the structural technology cycle, Value provides leverage to inflation and commodity trends, and low volatility sectors offer resilience if economic growth slows or market volatility increases.

In an environment shaped simultaneously by geopolitical shocks, inflation risks, and technological transformation, diversification across all three pillars may prove to be the most durable investment strategy.

Elev8 Model Positioning Context:

The Elev8 model is positioned in the near-term for Value sectors to continue outperforming. We’ve shifted capital from cyclical and Growth sectors towards resource focused and low vol. sectors for March. However, we maintain 20% of the portfolio in Technology stocks. We feel, based on our indicators that a correction in the near-term for equities remains an elevated risk with the uncertainty surrounding AI disruption in tandem with a volatile geopolitical situation. We think Growth shares offer potential down the road, but uncertainty around the direction of interest rates remains a headwind.