Performance Summary: Week Ending March 20th, 2026

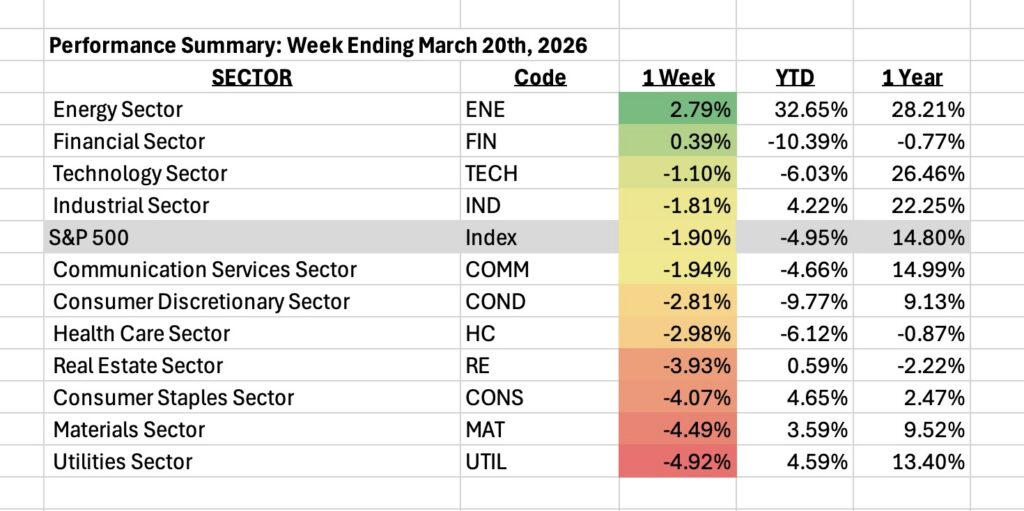

The S&P 500 declined 1.9% for the week, reflecting a combination of macroeconomic uncertainty and geopolitical risk. The primary driver was a renewed rise in inflation concerns, largely tied to a sharp increase in oil prices amid escalating Middle East tensions. Higher energy prices raised concerns that inflation could remain elevated, reducing the likelihood of near-term interest rate cuts. At the same time, central banks—including the Federal Reserve—signaled a more cautious policy stance, reinforcing a “higher for longer” rate environment.

Energy (+2.8%) was the clear outperformer, benefiting directly from rising crude oil and natural gas prices. Supply disruptions tied to geopolitical conflict pushed oil prices above $100 per barrel during the week, driving strong earnings expectations across the sector. Key contributors included Exxon Mobil and Chevron, which carry significant index weight, along with strength in companies such as ConocoPhillips and EOG Resources. The sector’s performance reflects its leverage to commodity prices, which acted as a hedge against broader market weakness.

Financials were the only other sector to finish the week in positive territory, with the up 0.4%. Performance was supported by relatively stable economic data, including resilient labor market indicators, which helped ease near-term credit concerns. Gains were led by large, diversified banks such as JPMorgan Chase and Bank of America, as well as strength in capital markets firms like Goldman Sachs. Despite underlying concerns about economic slowing, the sector showed relative resilience versus the broader market.

Materials lagged significantly, down 4.5%. The decline was driven by falling prices in precious and industrial metals, alongside concerns about slowing global growth. Weakness was most pronounced in mining stocks, with companies such as Newmont and Freeport-McMoRan experiencing notable declines. The sector remains highly sensitive to global demand expectations, and rising recession concerns weighed heavily on investor sentiment.

Utilities were the weakest sector for the week, falling 4.9%. Rising bond yields and interest rate expectations pressured the sector, which is typically viewed as a bond proxy due to its income-oriented characteristics. Higher yields reduce the relative attractiveness of utility dividends, leading to outflows. Additionally, investors rotated away from defensive sectors toward energy exposure as commodity prices surged. Key detractors included large regulated utilities such as NextEra Energy, Duke Energy, and Southern Company.

Bottom Line:

The week highlighted a market increasingly driven by macro forces—particularly inflation and geopolitics—with energy acting as a key beneficiary, while rate-sensitive and growth-dependent sectors faced renewed pressure.