The market’s message this week was clear: investors are still willing to look through geopolitical risk, sticky inflation concerns and weak consumer sentiment when the AI capex story is accelerating. Friday’s session reinforced that point, with the S&P 500 and Nasdaq closing at fresh records, semiconductors and memory leading the tape, and the broader market still showing signs of concentration as equal-weight S&P lagged the cap-weighted index. StreetAccount framed the path of least resistance as higher, powered by another semi-led rally and continued confidence in AI compute and capex demand.

The latest news flow also suggests the AI story is evolving from a narrow “own the chips” trade into a broader infrastructure cycle. Broadcom was reportedly in talks for a $35B financing package to help fund AI-chip development, Anthropic struck a $1.8B computing deal with Akamai, AMD’s post-earnings strength was tied to datacenter momentum and agentic AI server CPU demand, and Nvidia’s ecosystem continues to expand through AI cloud and data-center partnerships.

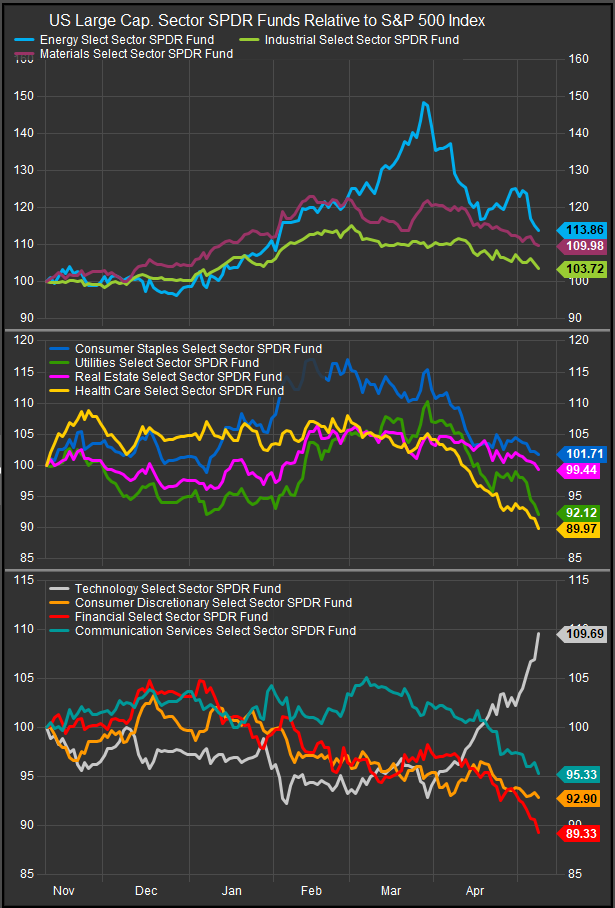

For sector investors, the key takeaway is that the AI halo is broadening, but not evenly. Technology remains the center of earnings momentum, and select Industrials remain the cleanest “picks and shovels” exposure through electrical equipment, cooling systems, construction services and grid contractors. However, the next stage of the trade increasingly points toward Utilities, Energy, Real Estate, Materials, Communication Services and select Financials as secondary beneficiaries.

Chart: Despite the S&P 500 trading to fresh all-time highs in May, only one sector is outperforming the broad market.

The Bull Case: AI Demand Is Pulling Capital Into the Real Economy

The AI trade increasingly looks less like a software cycle and more like a capital-spending supercycle. That distinction matters. Software cycles can be disrupted by model compression, cheaper inference and changing application economics. Infrastructure cycles require land, power, cooling, transmission, copper, substations, financing and long-term contracted capacity. That makes the beneficiary set broader, more asset-heavy and more tied to real-world bottlenecks.

This is why Akamai’s move was important. A seven-year, $1.8B compute capacity deal is not simply a cloud headline; it is a signal that model developers are reaching beyond the traditional hyperscaler stack to secure capacity. Likewise, IREN’s AI cloud contract with Nvidia, CoreWeave’s backlog commentary and the continued focus on datacenter supply all point to a market where compute scarcity is becoming a business model.

The broader implication is that AI is becoming a demand shock for physical infrastructure. It requires electricity, grid modernization, backup generation, cooling equipment, engineering services, copper, transformers, switchgear and financing. This makes the AI trade increasingly relevant for sector investors who may not normally view themselves as investing in “technology.”

Utilities: The Clearest Non-Tech Beneficiary

Utilities are arguably the cleanest non-Technology beneficiary of the AI buildout. For years, regulated utilities were treated primarily as bond proxies, punished when rates rose and rewarded when yields fell. AI changes that framework by adding a structural load-growth story to a sector that had spent much of the prior decade managing relatively muted demand growth.

The sector’s opportunity is tied to datacenter electricity demand, transmission investment and rate-base expansion. Utilities with exposure to regions seeing hyperscaler or AI-campus growth — including parts of PJM, ERCOT, the Mid-Atlantic and other power-constrained markets — may be positioned for higher long-term investment needs.

The risk is regulatory. Higher capex can support earnings growth, but customer affordability, local opposition, interconnection delays and political scrutiny could limit how quickly that growth is monetized. In other words, AI can improve the demand outlook for Utilities, but it does not remove the sector’s dependence on regulators, financing costs and execution.

Energy: AI Reintroduces Power Security as an Investment Theme

The AI trade is also reviving parts of the Energy sector. This is not simply a crude oil call. The relevant exposure is natural gas generation, midstream infrastructure, LNG optionality, backup power, fuel security and, over a longer horizon, nuclear and geothermal.

The StreetAccount weekend headlines already pointed to a fragile energy backdrop, with the Iran conflict keeping energy security in focus and depleted stockpiles potentially keeping oil prices high even after Hormuz reopens. That geopolitical overlay intersects with AI because the power grid is already tight. As datacenter demand rises, the market is likely to place a premium on companies that can deliver reliable, dispatchable power and the infrastructure needed to move it.

That makes Energy a tactical AI-adjacent beneficiary, particularly in natural gas, midstream and power-linked assets. The offset is inflation risk. Higher energy costs can support Energy earnings, but they can also pressure datacenter economics, corporate margins and the Fed’s ability to ease policy.

Real Estate: Data Centers Are the Growth Pocket

Real Estate remains a divided sector. Traditional office still faces structural headwinds, residential affordability remains constrained and higher rates continue to pressure valuations. But data centers remain a rare growth vertical with demand visibility.

The most valuable real estate in the AI economy is not simply land; it is powered land. Sites with access to electricity, transmission, permitting and hyperscaler demand should command a premium. That favors data center REITs, powered-land developers and specialized real estate platforms with execution capabilities.

This is not a blanket bullish call on Real Estate. The sector’s AI beneficiaries are highly specific. The winners are likely to be companies with power access, interconnection rights, scale, low-cost capital and credible development pipelines. Assets without a direct link to digital infrastructure may continue to behave more like traditional rate-sensitive REIT exposure.

Materials: Copper and Grid Inputs Are Hidden AI Beneficiaries

Materials should not be ignored. AI infrastructure is copper-intensive because the buildout requires power generation, transmission, distribution, substations, switchgear, transformers, busbars, cooling systems and server farms.

This creates a potential structural tailwind for copper miners, electrical metals, specialty materials and companies exposed to grid modernization. The AI trade is often discussed in terms of GPUs and cloud platforms, but the physical buildout requires a deep industrial supply chain. That makes Materials an underappreciated AI-adjacent sector, particularly where companies are tied to electrification, grid reliability and datacenter infrastructure.

The risk is cyclicality. Materials companies remain exposed to China demand, global manufacturing trends, currency effects and commodity-price volatility. But within the sector, AI adjacency may increasingly separate companies with structural demand from those that remain purely macro-sensitive.

Communication Services: AI Monetization and Platform Power

Communication Services is an overlooked AI beneficiary because many investors mentally classify Alphabet and Meta as “tech,” even though they sit in Communication Services. The latest headlines around Alphabet’s AI momentum and Alibaba’s integration of Qwen AI into Taobao highlight how AI is becoming embedded in search, advertising, commerce and content distribution.

For Communication Services, the AI question is less about infrastructure and more about monetization. Search, digital advertising, recommendation engines, streaming, gaming, creator tools and agentic commerce can all benefit from improved targeting, automation and user engagement.

But the sector also faces disruption risk. AI agents could change how users search, shop and consume media. The best-positioned companies are those with distribution, proprietary data, ad networks, cloud infrastructure and the ability to convert AI features into incremental revenue rather than simply higher costs.

Financials: The Capital Stack Behind the AI Buildout

Financials are not a front-line AI sector, but the capital intensity of the buildout creates opportunities for asset managers, private credit, infrastructure finance and banks with project-finance capabilities. The reported Broadcom discussions with Apollo and Blackstone around a $35B AI-chip financing package highlight how AI infrastructure increasingly requires large, structured pools of capital.

This makes Financials a second-derivative beneficiary. The opportunity is strongest where capital is tied to durable infrastructure, long-term contracts and high-quality counterparties. The risk is that parts of the AI buildout eventually resemble a capital-heavy commodity cycle, where financing grows quickly before investors fully understand utilization, depreciation and return-on-capital dynamics.

The Main Risk: Froth, Rates and Market Concentration

The bullish story is powerful, but the risks are not trivial. StreetAccount noted renewed froth concerns around the semiconductor rally, including comparisons to prior momentum extremes, while also flagging AI-related layoffs and rising token-cost pressures as emerging corporate themes. Friday’s tape also showed narrow breadth, with cap-weighted indexes outperforming equal-weight benchmarks even as headline indexes made new highs.

The macro backdrop is also more complicated than the index price action suggests. April payrolls were stronger than expected, but consumer sentiment hit a record low, inflation expectations remain elevated and Fed commentary continues to push back against an easy-cut narrative. If AI-driven productivity optimism supports growth while inflation remains sticky, rates could stay higher for longer. That would be a particular challenge for Utilities, REITs and other capital-intensive AI-adjacent beneficiaries that depend on financing costs.

Chart: Market internal trends reinforce the narrow participation message. Despite new index level price highs, only 53% of S7P 500 constituents are trading above their 50 and 200-day moving averages.

Sector Positioning Takeaway

For sector investors, the AI trade should be viewed in three rings.

The first ring remains Technology: semiconductors, memory, networking, cloud infrastructure, cybersecurity and power semis. This is still where the cleanest earnings revisions sit, but valuation and concentration risk are rising.

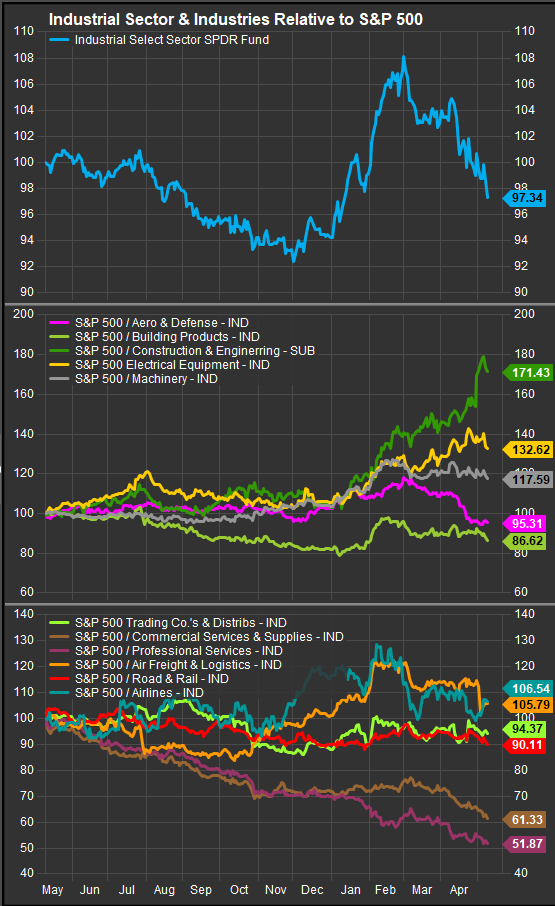

The second ring is Industrials plus Utilities: electrical equipment, cooling, engineering, grid contractors and regulated utilities with credible load-growth exposure. This is where the AI trade is becoming most tangible.

Chart: Construction & Engineering and Electrical Equipment stocks have been key AI trade components with performance to reflect it.

The third ring is the broader halo: Energy, Real Estate, Materials, Communication Services and select Financials. These sectors may not screen as obvious AI winners, but they are increasingly tied to the physical, financial and commercial architecture needed to turn AI demand into deployable compute.

The best sector strategy is not to abandon Technology, but to broaden the AI lens. The market is no longer only rewarding companies that design chips or train models. It is beginning to reward companies that can power, cool, finance, house and connect the AI economy.

Conclusion: AI Adjacency Is the Litmus Test for Leadership

The most important sector message from the week is that market breadth remains narrow, but the reason for that narrowness is changing. The S&P 500’s leadership is still concentrated, and Friday’s lag in equal-weight performance showed that the average stock is not participating to the same degree as the index leaders. Yet this concentration is not random. It increasingly reflects the market’s belief that earnings growth is clustering around the AI trade and the infrastructure required to support it.

That has major implications for stock, industry and sector selection. If earnings growth remains concentrated in companies with direct or indirect AI exposure, then AI adjacency may become one of the most important determinants of relative performance. Companies do not need to be semiconductor designers or cloud platforms to benefit, but they do need a credible connection to the AI value chain — whether through power demand, grid investment, data center capacity, copper intensity, cooling systems, infrastructure finance, digital advertising or agentic commerce.

In that environment, winners and losers are likely to be determined less by traditional sector labels and more by proximity to the AI spending cycle. The market’s narrow breadth is therefore both a warning and a roadmap. It warns that the index is increasingly dependent on a concentrated earnings engine, but it also identifies where investors should look for the next layer of opportunity. The broader the AI infrastructure halo becomes, the more important AI adjacency will be in separating sector leaders from laggards.

Sources:

International Energy Agency, Energy and AI

Reuters reporting on hyperscaler AI capex, U.S. power demand, Exelon, Nvidia/IREN, Flex, Quanta, Schneider Electric, Dover and copper demand

CBRE 2026 U.S. Data Center Outlook

S&P Global research on copper demand in the age of AI

Additional charts and data sourced from FactSet Research Systems Inc.

Disclaimer: This article is for informational and educational purposes only and does not constitute investment advice, a recommendation, or an offer to buy or sell any security, ETF, sector, or investment strategy. Sector views and market commentary are based on current information and may change without notice. Investors should consider their own objectives, risk tolerance, time horizon and financial circumstances before making investment decisions. Past performance is not indicative of future results.