Upside momentum for the S&P 500 off the March 31, 2026 low has given way to consolidation as the market looks for bullish confirmation. This week’s headlines leave sector investors with a constructive but selective macro backdrop. The most powerful investment themes are AI infrastructure, power demand, energy security, defense, workflow automation, supply-chain efficiency, and cash-flow discipline. The biggest concerns are inflation persistence, long-yield pressure, AI crowding, geopolitical fragility, and consumer fatigue.

The central message is that AI is no longer just a semiconductor story. It is becoming a full value-chain cycle that reaches into data centers, networking, power generation, grid equipment, cooling, software automation, cybersecurity, logistics, enterprise workflows, and corporate M&A. This week’s headlines also show that AI is already reshaping business models: Nvidia continues to convert AI demand into revenue and cash returns; Anthropic’s reported compute-cost leverage points to improving AI unit economics; Workday’s results suggest agentic AI can support software value rather than simply cannibalize it; and lower model pricing from DeepSeek could make AI adoption cheaper for downstream users.

The offset is that AI is not yet clearly solving the market’s macro problem. Inflation remains elevated, long-term Treasury yields remain under pressure, and the Fed is less willing to promise rate relief. The April FOMC minutes showed that a majority of participants believed some policy firming could become appropriate if inflation continued to run persistently above 2%. That means sector investors should still favor areas with visible earnings, pricing power, strategic scarcity, and cash-flow durability.

AI Is the Strongest Growth Theme, but the Winners Are Broadening

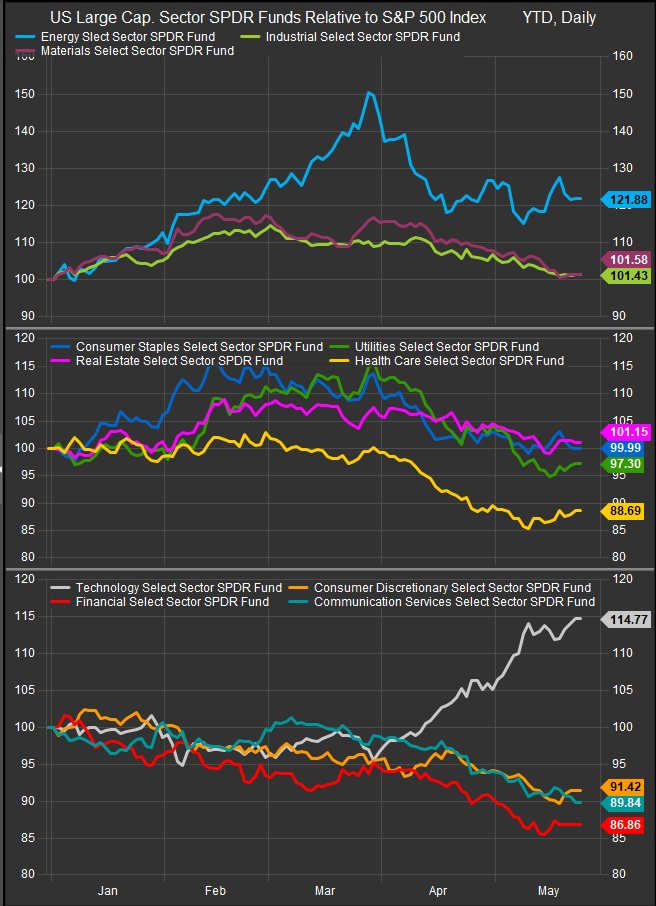

The most direct beneficiary remains Information Technology, especially semiconductors, networking, cloud infrastructure, cybersecurity, data-center hardware, and software platforms with measurable AI monetization. Nvidia reported record first-quarter revenue of $81.6 billion, up 85% year over year, with GAAP and non-GAAP gross margins of 74.9% and 75.0%, respectively.

But the more interesting sector message is that AI is spreading beyond Technology. This week’s headlines highlight energy and infrastructure deals, AI-driven M&A, and strong demand across the AI compute ecosystem. That supports Industrials through electrical equipment, grid infrastructure, engineering and construction, automation, cooling, power systems, and data-center construction. It also supports Utilities, but selectively: the sector benefits from data-center load growth and power scarcity, though higher yields and regulatory pushback remain risks.

The AI value chain is also becoming more efficient. Workday reported total revenue of $2.542 billion, up 13.5% year over year, subscription revenue up 14.3%, and non-GAAP operating income equal to 31.8% of revenue. This is important because it shows how AI can improve workflow software economics rather than simply disrupt software incumbents. Similarly, Accenture research found that companies with the most mature supply chains are 23% more profitable than peers and are far more likely to use AI and generative AI widely across supply-chain functions.

The investment implication is to own AI where it is already improving economics: chips, networking, cloud infrastructure, cybersecurity, enterprise workflow software, supply-chain optimization, industrial automation, and power infrastructure. Be more cautious where AI is only a narrative or where the business model is vulnerable to pricing pressure, seat compression, or model commoditization.

Energy Security Remains a Tailwind, Even with Peace Headlines

This week’s headlines point to tentative progress on a U.S.-Iran framework that could reopen the Strait of Hormuz, but they also show unresolved issues around uranium stockpiles, sanctions relief, missiles, and regional proxies. Energy markets may respond favorably to de-escalation headlines, but the supply system remains tight.

The EIA’s May outlook estimated that Iraq, Saudi Arabia, Kuwait, the UAE, Qatar, and Bahrain collectively shut in 10.5 million barrels per day of crude oil production in April, while assuming the Strait of Hormuz remains effectively closed until late May and only begins to see traffic recover in June. Reuters also reported that oil fell nearly 5% as optimism rose around a possible U.S.-Iran deal, while noting that full restoration of oil production and transport could still take months.

That keeps Energy in a tactical overweight position. Integrated oil, exploration and production, oilfield services, LNG, midstream, and MLPs remain useful inflation and supply-security exposures. The risk is that a credible and durable reopening of Hormuz compresses the geopolitical premium. But while inventories remain tight and production recovery is uncertain, Energy remains one of the few sectors where the macro problem can become an earnings tailwind.

The Consumer Is Holding Up, but the Winners Are Narrowing

This week’s headlines still show areas of consumer resilience, particularly in payments, off-price retail, and select home-improvement demand. Visa and Mastercard commentary pointed to resilient spending, while TJX and Ross showed continued strength in off-price retail. Home Depot also suggested underlying demand remained stable despite gas-price and housing-affordability pressure. Census data support the idea that the consumer has not broken: April retail trade sales rose 0.5% from March and 5.2% from a year earlier, while nonstore retailers rose 11.1% year over year.

But this is not a broad Consumer Discretionary bull case. This week’s headlines also flagged pressure at Walmart, Target, and Chewy tied to higher fuel costs, weaker sentiment, fading tax-refund support, and a more stretched low-end consumer.

For sector investors, the distinction matters. Favor off-price retail, premium brands with pricing power, digital platforms with scale, and companies using AI to improve fulfillment, inventory, personalization, and labor productivity. Avoid broad exposure to autos, travel, restaurants, housing-linked retail, and lower-income discretionary categories until fuel, financing, and real-income pressure ease.

Inflation and Long Yields Remain the Biggest Macro Constraint

The market’s biggest concern is that inflation is not falling fast enough to restore a clear easing cycle. April CPI rose 3.8% year over year, core CPI rose 2.8%, energy rose 17.9%, and food rose 3.2%. Producer-price pressure also remains significant: final-demand PPI rose 1.4% in April and 6.0% year over year, with services up 1.2% and goods up 2.0%.

This week’s headlines reinforce the same concern: long yields remain under upwards pressure from inflation, fiscal deficits, geopolitical risk, and a hawkish policy shift, even if oil retreats. That creates a valuation ceiling for rate-sensitive and speculative sectors. It also makes cash flow more valuable. We see credit tightening most clearly in the behavior or US 10yr real yields (below) which have tightened since the beginning of May. If Real Yields keep moving higher, we’d expect some rotation from Growth to Value exposures.

Under present conditions, the sector playbook is therefore clear. Overweight Information Technology tied to AI infrastructure, Industrials tied to power and automation, Energy as a tactical inflation hedge, and select Utilities tied to data-center load growth. Keep Communication Services neutral to modestly overweight where platforms have AI distribution advantages and strong free cash flow. Keep Financials selective, favoring insurers, large banks, exchanges, and asset managers while avoiding weaker credit-sensitive and consumer-finance exposure.

Underweight Consumer Discretionary, traditional Real Estate, and broad Materials. Maintain a selective underweight in Consumer Staples and Health Care: Staples face food, freight, and volume pressure, while Health Care has defensive value but less direct support from the dominant AI-energy-infrastructure themes.

Bottom Line

This week’s headlines confirm that the most powerful themes are AI infrastructure, workflow automation, power demand, energy security, defense, supply-chain efficiency, and cash-flow discipline. AI disruption remains a risk, but the market is increasingly rewarding companies that turn AI into lower unit costs, better logistics, faster software workflows, improved margins, and stronger returns on capital.

For sector investors, this is not a market to buy uniformly. It is a market to own sectors where AI, energy security, or infrastructure spending are already improving earnings visibility. The winners are companies with pricing power, capex leverage, data scale, power access, operational complexity, and cash-flow durability. The losers are companies that need lower rates, cheaper energy, stronger low-end consumer demand, or speculative capital to work.

Sources

- Latest weekend headlines and this week’s market commentary provided by FactSet/StreetAccount, including AI, Iran/Hormuz, Energy, Markets, Economy, Central Banks, Trade, Geopolitics, and sector-relevant corporate headlines.

- Latest AI, Energy, central-bank, market, housing, and corporate headlines provided by FactSet/StreetAccount

- Nvidia — Fiscal Q1 2027 earnings release and guidance commentary.

- Federal Reserve — April 28–29, 2026 FOMC minutes.

- U.S. Bureau of Labor Statistics — April 2026 CPI report.

- U.S. Bureau of Labor Statistics — April 2026 PPI report.

- U.S. Energy Information Administration — May 2026 Short-Term Energy Outlook.

- U.S. Census Bureau — April 2026 retail sales report.

- Workday — Fiscal Q1 2027 financial results.

- Accenture — Research on AI-enabled supply-chain maturity and profitability.

- Reuters — Oil, U.S.-Iran, AI, markets, and macro reporting.

Disclaimer: This commentary is for informational and educational purposes only and does not constitute investment advice, a recommendation, or an offer to buy or sell any security, ETF, sector, thematic strategy, or investment product. Views are based on current market conditions, news flow, company reports, macroeconomic data, and third-party sources that may change without notice. Sector positioning comments are not tailored to any investor’s objectives, risk tolerance, or financial situation. Investors should conduct their own research and consult a qualified financial professional before making investment decisions. Past performance is not indicative of future results.