January 4, 2026

The sector opportunity set for 2026 is being shaped less by policy speculation and more by a clearer earnings bifurcation that has emerged across the market. While headline index returns in 2024–25 were dominated by a narrow leadership cohort, bottom-up estimates now suggest that earnings growth is broadening—but not evenly. According to FactSet, S&P 500 earnings are expected to grow roughly 15% in CY2026, with the S&P 493 still delivering low-double-digit EPS growth (~12–13%). That dispersion matters: sectors with genuine revenue and margin tailwinds are positioned to compound, while others are increasingly reliant on multiple expansion or defensive allocation flows.

At the macro level, consensus expectations have converged around a soft-landing regime—real GDP near trend (~2%), inflation continuing to cool, and policy rates drifting lower but remaining restrictive in real terms. This environment tends to reward earnings visibility, pricing power, and balance-sheet strength, while penalizing sectors that rely on either accelerating consumer leverage or sharply lower rates to justify valuations. Investor risk appetite reflects this nuance: credit spreads remain tight, and equity volatility subdued, but positioning is more selective than indiscriminately bullish.

Against that backdrop, three sectors stand out with the strongest structural setup heading into 2026.

Information Technology enters the year with the clearest earnings momentum. FactSet’s bottom-up data places Technology among the few sectors expected to deliver sustained double-digit earnings growth in CY2026, supported by both top-line expansion and margin durability. Importantly, revenue growth—not just operating leverage—is driving estimates higher, reflecting ongoing enterprise and hyperscaler investment tied to AI infrastructure, cloud optimization, and software productivity gains. While valuation risk remains elevated, Technology continues to benefit from falling inflation expectations and a rate environment that supports long-duration cash flows. Analyst sentiment reinforces this positioning: Technology carries one of the most favorable net rating outlooks across sectors, suggesting investors remain willing to underwrite growth even amid periodic AI-cycle skepticism.

Consolidation into year-end is a setup for potential accumulation in Technology shares to start 2026.

Communication Services shares many of Technology’s structural tailwinds but with a slightly different earnings profile. FactSet projects double-digit earnings growth in CY2026, driven by accelerating monetization of AI-enabled advertising, content distribution, and data-driven engagement platforms. Revenue growth expectations remain among the strongest in the market, while free-cash-flow generation provides downside support in risk-off episodes. Compared with pure Technology, Communication Services tends to be somewhat less sensitive to rate volatility and more directly linked to real-time consumer and advertiser demand—making it an attractive hybrid exposure in a late-cycle expansion.

Industrials represent the most compelling “real-economy” expression of the 2026 outlook. Earnings estimates point to double-digit EPS growth, supported by a multi-year backlog cycle tied to infrastructure investment, reshoring, automation, and energy-intensive AI data-center buildouts. Unlike prior cycles, margin resilience has remained strong despite easing pricing power, reflecting productivity gains and disciplined capital allocation. Industrials also screen favorably in a macro regime where growth moderates but does not contract—historically an environment where operating leverage is rewarded without the balance-sheet stress seen in downturns.

Beyond these leaders, several sectors show constructive but more conditional setups.

Health Care stands out as a defensive growth option. While not among the highest absolute earnings growers, the sector offers stable mid-single-digit to high-single-digit EPS growth with relatively low macro sensitivity. This becomes increasingly valuable if 2026 introduces volatility around fiscal policy, geopolitics, or election-year uncertainty. Analyst expectations have improved modestly, particularly in large-cap pharma and select medical technology segments, suggesting Health Care could outperform on a relative basis even if broader risk appetite softens.

Healthcare stocks traded into a technical bullish reversal pattern in the second half of 2025. Speculative Biotech exposures were a driver of outperformance as proxied here by the SBIO ETF.

Financials sit at the intersection of macro uncertainty and earnings durability. The sector’s outlook depends heavily on the path—not just the direction—of interest rates. A gradual easing cycle with resilient credit conditions would support returns via stable net interest income, improving capital markets activity, and contained loan losses. However, faster-than-expected cuts could pressure margins, while renewed growth scares would challenge credit assumptions. As a result, Financials appear well positioned for selective outperformance, but less compelling as a broad sector beta play.

Materials offer upside leverage to global growth and capital-spending cycles, with FactSet projecting double-digit earnings growth in CY2026. That said, the sector’s sensitivity to commodity prices, the U.S. dollar, and China-linked demand introduces volatility. Materials are best viewed as a risk-on cyclical complement rather than a core allocation unless global manufacturing momentum accelerates more decisively.

Several sectors appear less favorably positioned on a forward-looking basis.

Consumer Discretionary, despite forecast double-digit earnings growth, faces a narrowing margin for error. Earnings assumptions rely on continued labor-market resilience and stable real incomes—conditions that may be tested if wage growth cools faster than expected or if consumers become more price sensitive. Historically, late-cycle environments tend to produce greater dispersion within Discretionary, making it a potential source of volatility rather than consistent leadership.

Real Estate remains fundamentally tied to interest-rate expectations. While eventual rate cuts provide valuation support, the sector’s earnings growth is modest and financing conditions remain restrictive. In a scenario where rates decline slowly rather than sharply, Real Estate may lag more growth-oriented alternatives.

At the defensive end of the spectrum, Consumer Staples and Utilities exhibit the weakest forward setups. FactSet data shows these sectors carrying among the least favorable analyst sentiment, reflecting limited earnings growth and diminished appeal outside of outright risk-off episodes. While they retain value as portfolio stabilizers, they are unlikely to lead in a 2026 environment where growth remains positive.

Finally, Energy stands apart for structural reasons. FactSet identifies Energy as the only sector expected to see a revenue decline in CY2026, driven primarily by oil-price assumptions rather than cost inflation. While geopolitical risk and supply disruptions can always alter the near-term narrative, the baseline earnings trajectory suggests Energy is better suited for tactical positioning than strategic overweighting.

A critical risk to the 2026 base case is a renewed rise in interest rates, or even a prolonged period of rates remaining higher than currently discounted, because the direction of rates—not just their level—plays an outsized role in shaping investors’ Growth versus Value positioning calculus. When yields are falling or clearly trending lower, investors are generally willing to underwrite longer-duration cash flows, favoring Growth sectors such as Information Technology and Communication Services, where a greater share of valuation rests on earnings expected several years out. Conversely, when rates back up or policy expectations shift toward “higher for longer,” the market’s discounting mechanism becomes less forgiving, compressing multiples on Growth equities even if near-term earnings remain intact. In those environments, capital often rotates toward Value-oriented sectors—such as Financials, Energy, and certain Industrials—where cash flows are more front-loaded, dividends provide a tangible return component, and valuation sensitivity to discount rates is lower. Importantly, history shows that rate volatility itself, rather than absolute yield levels, can be the most destabilizing force: abrupt moves in Treasury yields tend to trigger rapid style rotations, elevate equity risk premia, and reduce tolerance for richly valued growth franchises. As a result, a scenario in which rates drift modestly higher or remain range-bound but volatile would likely lead to more frequent Growth–Value regime shifts, compressing index-level returns and increasing the importance of active sector allocation and balance between duration-sensitive growth exposure and cash-flow-oriented value ballast.

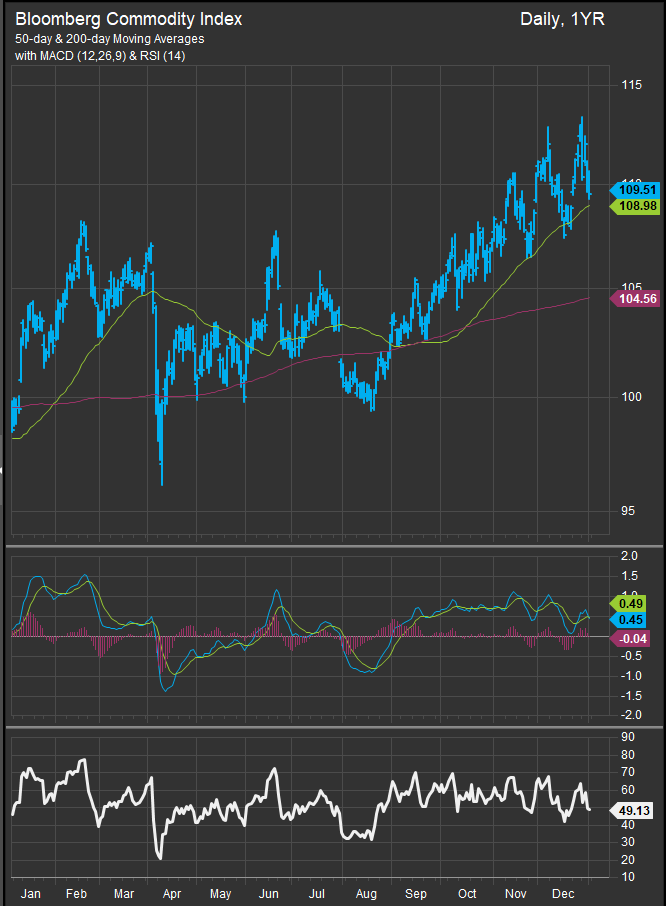

Commodities prices closed 2025 on the upswing. We’re watching this price action closely as inflation remains a potential spoiler.

Interest rates have firmed in the past month. We think 4.4% is a key level to watch in Q1

Or course we need only turn on the news to see situations evolving in Venezuela, the Middle East, Ukraine and on global topics like global trade and beyond. Sector funds offer a key tool to adapt to changing conditions and we will be here to share our take macro and sector focused developments throughout 2026.

Bottom Line

While we remain vigilante for changes in the landscape that could tilt our base case, we think the present environment continues to favor a slight Growth oriented tilt to equity portfolios. The 2026 sector landscape is likely to favor earnings visibility over outright defensiveness given an economy near full employment and a Fed inclined towards accommodation. Technology, Communication Services, and Industrials offer the strongest alignment between earnings trends, macro conditions, and investor risk appetite. Health Care and Financials provide selective opportunities, while Staples, Utilities, and Energy appear positioned as hedges rather than leaders. In a market increasingly focused on how earnings are generated—not just how fast—sector selection is likely to matter more than broad beta exposure. We start with a constructive outlook for 2026 with inflation continuing to cool and the fruits of the AI technology build-out potentially still to be harvested.

Sources:

Bank for International Settlements. Quarterly Review. Basel, Switzerland: BIS, various issues.

BlackRock Investment Institute. Global Investment Outlook. New York, NY: BlackRock, various editions.

Federal Reserve. Federal Open Market Committee Statements, Press Conferences, and Summary of Economic Projections. Washington, DC: Board of Governors of the Federal Reserve System.

Federal Reserve Bank of St. Louis. FRED Economic Data Database. St. Louis, MO.

FactSet Research Systems Inc. Earnings Insight and Equity Market Analytics. Norwalk, CT.

Goldman Sachs Group, Inc. U.S. Equity Strategy and Macro Research Reports. New York, NY.

Morgan Stanley. Cross-Asset Strategy and Equity Factor Research. New York, NY.

MSCI Inc. MSCI Growth and Value Index Methodology and Performance Reports. New York, NY.

S&P Dow Jones Indices. Style Indices Methodology and Factor Attribution Reports. New York, NY.

Vanguard Group. Market Perspectives and Valuation Research. Valley Forge, PA.

Additional data from this report was compiled through FactSet Research Systems Inc.