November 23, 2025

The coming Thanksgiving week finds investors in an uneasy place: the AI trade has been shaken, but not broken, and the macro data emerging since the federal government reopened paints a picture of an economy that is cooling unevenly rather than rolling over. From a sector perspective, the key question is not simply whether equities rebound, but which sectors investors should be overweight or underweight as the market decides whether the AI-led bull narrative still has legs.

On the macro side, the post-shutdown dataflow has been messy but instructive. The delayed September nonfarm payrolls report surprised to the upside at 119K versus expectations of 50K, the strongest print since April, but under the surface it looked more like a late-cycle plateau than a re-acceleration. August was revised down into negative territory, unemployment ticked up to 4.4%, and wage growth decelerated to 0.2% month-over-month with year-over-year earnings stuck around 3.8%. Job gains were concentrated in leisure, health care, and construction, while transportation, manufacturing, and federal government shed jobs. That mix, combined with rising continuing claims and a spike in WARN notices, leaves investors with the sense of a labor market that is loosening, not collapsing—enough to keep recession fears at bay, but not enough to give the Fed a blank check to slash rates aggressively.

Other prints since the reopening support that “muddling through” narrative. The Empire State Manufacturing Index jumped to its highest level since late 2024, with new orders, shipments, and workweek all improving and price indices still elevated but edging lower. The NAHB housing index has crept to its best level since April, yet a record share of builders is cutting prices by roughly 6%, a sign that demand is being nursed along with discounts rather than booming on its own. Delayed factory orders and durable goods data showed transportation-led strength and modest core gains, while initial jobless claims remain low even as continuing claims sit at multi-year highs. Overall, the data tell equity investors that the US economy still supports earnings growth, but also that profit expansion will be more about productivity, pricing power, and cost discipline than volume.

Layered on top of that is a Federal Reserve that is visibly divided. October’s FOMC minutes confirmed an internal split over the wisdom of a December rate cut, even after the earlier 25 bp move: some members argued to hold policy steady through year-end, while others were willing to entertain an additional cut. Subsequent comments from Fed officials have only added to the ambiguity. New York Fed President Williams has allowed that there is room for another rate adjustment “in the near term” to bring policy closer to neutral, while Boston’s Collins and Dallas’s Logan continue to emphasize caution, arguing that moderately restrictive policy remains warranted and that inflation risks have not fully receded. With key jobs and inflation reports delayed or rescheduled, the Fed is flying partially blind, and markets are trading each speech rather than a clean economic roadmap. For sector allocators, that means rate-sensitive groups—Financials, Real Estate, Utilities, and long-duration Tech/growth—will remain highly sensitive to day-to-day swings in rate-cut probabilities.

Against this backdrop, the AI complex has been through a psychological and technical stress test. Fundamentally, the story remains exceptionally strong. Nvidia’s latest quarter delivered another massive beat and raise, with data-center revenues surging, margins tracking in the mid-70s, and management pointing to a multi-hundred-billion-dollar Blackwell/Rubin pipeline that stretches through 2026. Cloud GPUs are effectively sold out, sovereign and hyperscaler demand remains intense, and older-generation chips are still fully utilized. At the same time, big Tech platforms continue to fold AI deeper into their product stacks, and capital spending plans from hyperscalers indicate that this is a structural investment wave rather than a short-lived fad.

Yet the price action has forced investors to question the trade’s durability. After Nvidia’s blowout results, the broader AI complex sold off as much as it rallied, with the S&P and Nasdaq breaking below key moving averages and systematic strategies forced to unwind crowded longs. The mere hint of “AI skepticism”—concerns about capex sustainability, capital constraints, widening credit spreads at large software and infrastructure names, and the circularity of AI companies investing in each other—was enough to flip flows. Fund-manager surveys now show the “AI bubble” as the single biggest perceived tail risk even while a majority of those same investors acknowledge that AI already boosts productivity. In other words, the narrative has decoupled from the fundamentals, and sector positioning has become the shock absorber.

For a durable rebound in AI-linked equities—especially within Information Technology, Communication Services, and parts of Industrials and Utilities tied to data-center build-out—investors will need to see three things. First, continued validation from earnings, not just from Nvidia but across the AI value chain: semis, hyperscalers, enterprise software, cloud, and the physical infrastructure behind data centers. That means revenue and order growth that still comfortably outpaces capex and opex, plus guidance that frames AI spending as margin-accretive over a reasonable time horizon. Second, investors need clearer evidence that AI investment is producing measurable productivity and cash-flow gains: rising free cash flow, disciplined buybacks, and less reliance on debt or equity issuance to fund capex would go a long way toward deflating bubble fears. Third, they need stability in the macro and policy backdrop—no sharp deterioration in labor or consumption data, and a Fed that signals enough easing over 2026 to avoid choking off long-duration growth without reigniting inflation.

From a sector-allocation lens, this argues for staying overweight Information Technology and select Communication Services, but with a sharper focus on quality. Within Tech, investors are likely to favor semiconductor leaders, diversified software platforms with proven AI monetization paths, and cloud/service names with strong balance sheets and high recurring revenue. Within Communication Services, the tilt may lean toward platforms with proven ad-tech or subscription-based AI tools rather than pure social-media beta. Conversely, the more speculative periphery of the AI trade—unprofitable small-cap software, levered hardware pivots, and story-only infrastructure names—should remain underweight until capital markets and credit spreads calm down.

Beyond AI, the recent data and earnings signal a barbell approach to sectors. On the cyclically exposed side, Consumer Discretionary looks bifurcated. Value-oriented retail and off-price names have been clear winners, with Walmart, TJX and others demonstrating resilient comps and solid margins as consumers trade down and hunt bargains. At the same time, mid-tier discretionary retailers and housing-sensitive categories face softer traffic, rising markdowns and heavier capex plans into 2026, as seen in recent Home Depot and Target reports. For sector allocators, that points toward a modest underweight in broad Discretionary but selective overweights in value-oriented, scale advantaged retailers and travel-related plays that benefit from still-strong demand for experiences, as confirmed by airline expectations for a record Thanksgiving travel period.

Financials sit at the intersection of the Fed debate and credit-cycle anxieties. Banks, insurers, and asset managers will benefit if the Fed manages a gentle glide path of modest cuts through 2026 without reigniting inflation or triggering a spike in defaults. However, ongoing headlines around private credit stress, fund restructurings, and over-collateralization tests being breached are a reminder that the cycle is not risk-free. In this environment, investors may reasonably stay neutral to slightly underweight broad Financials, favoring higher-quality, well-capitalized banks and fee-driven asset managers over more levered credit-sensitive names.

Rate sensitivity also makes Real Estate and Utilities nuanced calls. On one hand, any stabilization or modest decline in long yields into year-end, combined with the Fed’s reluctance to re-tighten, supports the case for closing some underweights in high-quality REITs and regulated Utilities, especially those that benefit from the data-center and grid-upgrades themes. On the other hand, with inflation still above target and Fed messaging mixed, investors are unlikely to fully embrace these sectors until they see clearer evidence of a dovish trajectory in 2026. For now, the likely stance is tactical, not strategic, overweight—using pullbacks in yields to add selectively rather than committing to a wholesale rotation.

Meanwhile, Energy and Materials remain tethered to both traditional demand and the AI build-out’s massive power and metals requirements. The IEA’s upward revision to oil demand, with explicit reference to AI and data centers as drivers, underscores that even a “digital” boom is resource-intensive. At the same time, global growth uncertainties, energy-transition politics, and geopolitical risk in Eastern Europe and the Middle East complicate the outlook. For sector allocators, that suggests neutral to modest overweight Energy and select Materials, emphasizing integrated majors and low-cost producers rather than highly levered exploration or speculative miners.

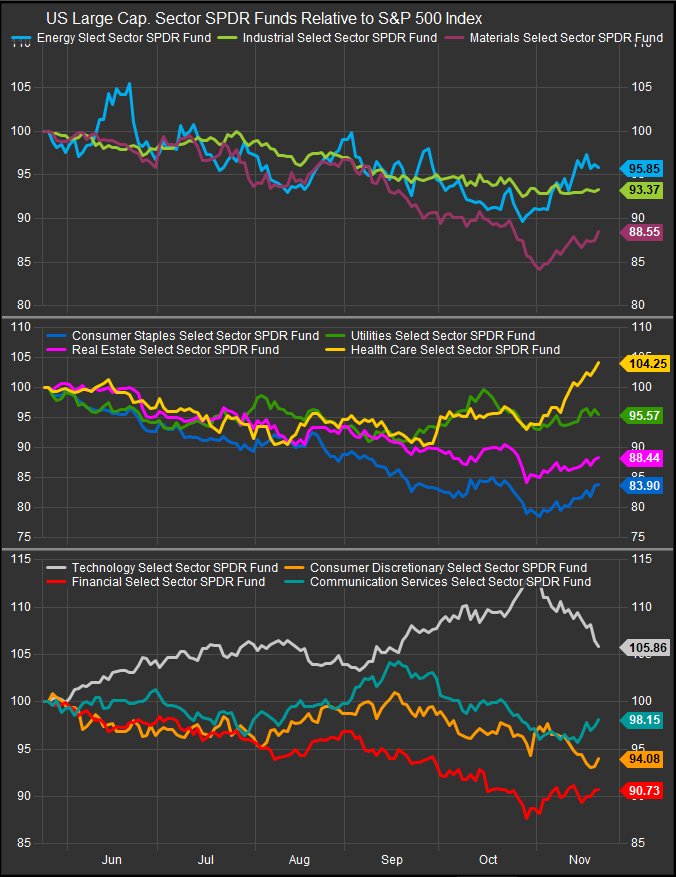

At ETFsector.com, we continue to see a path forward for Growth stocks over longer timeframes. The current correction and rotation is a healthy part of the equity market’s discounting mechanism. Our guard-rails remain concern for rising interest rates and commodities prices. So far, despite some concerns about AI overvaluation rates have remained towards the lower end of their long-term range. This keeps the Fed in a potentially supportive position with employment and earnings still in relatively strong positions. We are most concerned about the health of the broad consumer segment, and we think Discretionary and Staples Sector underweights should fund low vol. exposure in other sectors to offset the risk of holding Technology stocks which we think are likely to rebound from present selling. As we can see from the chart above, the XLK has retraced more than half of its outperformance over the past 6 months with lagging sectors moving towards par over the same timeframe. We can talk about bubbles and tail-risk all we want, but it is clear that AI stocks have been growing faster than any other category over the short, intermediate and long-term. Too much near-term discounting will be seen as opportunity very quickly if macro conditions remain stable. There’s upside risk as well as downside risk present in the current setup.

Data sourced from:

News & Data Aggregators / Major Financial Outlets

Reuters

Bloomberg

CNBC

Financial Times (FT)

Yahoo Finance

TechCrunch

Politico

Economic Times

FreightWaves

BBC

AP News (Associated Press)

The Hill

The Guardian

Japan Times

OilPrice.com

New York Times (NYT)

NBC / Newsmax (broadcast + digital news)

ABC News

BofA Global Fund Manager Survey (reported by multiple aggregators)

Additional charts and data sourced from FactSet Research Systems inc.