S&P futures are up 0.35% Tuesday morning after U.S. equities finished lower Monday, with parcel/logistics, transports, travel/leisure, homebuilders, retailers, industrial conglomerates, precious metals, chemicals, and banks among the laggards. Energy, memory, software, biotech, and exchanges outperformed. Global risk tone is mixed, with Asia mostly lower overnight, Hong Kong lagging, and Europe up more than 1%. Treasuries are firmer after Monday’s selloff, the dollar is slightly higher, gold is up 0.8%, Bitcoin futures are up 1.1%, and WTI crude is down 2.2% after Monday’s 4%+ rally.

The macro tone is quieter, with markets taking some relief from the lack of further Middle East escalation after Monday’s ceasefire cracks. Rhetoric remains measured, keeping hopes alive for a diplomatic path. Lower oil and yields are helping ease Monday’s stagflation concerns and refocus attention on strong Q1 earnings, AI compute demand, infrastructure capex, and the broader growth/momentum rebound. Today’s data calendar includes ISM services, expected to slip to 53.7 from 54.0, new home sales, and JOLTS job openings. Fed officials Bowman and Barr speak today, with ADP payrolls Wednesday and the April employment report Friday. Consensus expects April payrolls up roughly 65K after March’s 178K gain, with unemployment unchanged at 4.3%.

Information Technology

- PLTR: Lower despite another large beat-and-raise, with positive commentary around continued AI-driven demand but high expectations into the print.

- ON: Beat and raised, though shares were constrained by a high bar following other analog semiconductor reports.

- FN: Weaker despite a beat-and-raise, with investor focus on Datacom revenue decline and valuation.

- INTC: Higher on reports of chip-related talks with Apple.

- NOW: Projected better-than-expected subscription revenue of $30B by 2030, supported by AI product momentum.

Communication Services

- PINS: Big gainer, with U.S. momentum the key bright spot.

- DUOL: Under pressure on MAU deceleration and updated bookings guidance.

Financials

- FIS: Higher after announcing a partnership with Anthropic to develop new AI tools for banks.

- Exchanges: Among the better-performing groups Monday.

- Banks: Among Monday’s laggards.

Healthcare

- EW: Announced a new CFO.

- Biotech: Among the better-performing groups Monday.

Consumer Discretionary

- POOL: Announced a CEO transition.

- Travel/leisure, homebuilders, retailers: Among Monday’s laggards as higher yields and geopolitical uncertainty weighed on cyclicals.

Industrials

- Parcel/logistics and transports: Underperformed Monday, still pressured after Amazon’s supply-chain-services announcement.

- Industrial conglomerates: Also among the weaker groups.

U.S. equities finished lower Monday, though off worst levels, with the Dow down 1.13%, S&P 500 down 0.41%, Nasdaq down 0.19%, and Russell 2000 down 0.60%. The session was pressured by renewed Middle East concerns, higher oil, higher yields, and a firmer dollar. WTI crude rose 3.2% to $105.24 as weekend headlines kept focus on Strait of Hormuz risk, the potential return of kinetic activity, and the broader economic impact of an extended U.S.-Iran conflict. Treasuries weakened with the curve flattening, as the 2-year yield rose 6 bp to 3.95%, the 10-year rose 6 bp to 4.44%, and the 30-year rose 5 bp to 5.02%, its highest level since July 2025. The dollar index gained 0.3%, while gold fell 2.6%, silver dropped 3.8%, and Bitcoin futures rose 2.0%. Fed pricing also turned more hawkish, with the market moving to price roughly 9 bp of hikes through year-end versus 0 bp on Friday. March factory orders rose 1.5% m/m, well ahead of the 0.5% consensus, while the Fed’s latest SLOOS showed tighter business lending standards, weaker or unchanged residential real estate loan demand, and tighter standards for other consumer loans. Treasury also raised its Q2 borrowing estimate to $189B from $109B, keeping focus on Wednesday’s quarterly refunding announcement.

Sector Highlights

Sector performance was mostly negative. Energy was the only S&P 500 sector to finish higher, rising 0.85% as crude rallied. Technology was a relative outperformer, down just 0.15%, supported by memory/HDDs, software, networking, and communications equipment. Consumer Discretionary fell 0.22%, Healthcare declined 0.29%, and Utilities slipped 0.34%, all outperforming the broader tape. Materials was the weakest group, down 1.57%, followed by Industrials down 1.17%, Consumer Staples down 0.73%, Financials down 0.72%, Communication Services down 0.57%, and Real Estate down 0.57%. The tape favored energy leverage, select AI infrastructure, software, payments, exchanges, private equity, and biotech, while logistics, trucking, banks, investment banks, building materials, homebuilders, industrial metals, retail/apparel, casual diners, travel/leisure, and household/personal care lagged.

Information Technology

- AMZN +1.4%: Announced Amazon Supply Chain Services, extending Amazon’s freight, distribution, fulfillment, and parcel-shipping capabilities to businesses of all types and sizes. The announcement weighed on traditional logistics names.

- GFS +4.4%: Upgraded to overweight from neutral at Cantor Fitzgerald, with the firm citing secular drivers including silicon photonics, satellite communications, physical AI, and edge-computing opportunities.

- Memory / HDDs: Outperformed within Technology, continuing to benefit from AI-driven data creation, hyperscaler storage demand, and positive investor sentiment toward memory pricing.

- Software: Outperformed despite the weaker tape, reflecting ongoing support from earnings resilience and selective optimism around AI-related demand.

Communication Services

- CCOI -29.3%: Q1 revenue and adjusted EBITDA missed consensus. Corporate and Enterprise revenue were weaker than expected, Net-centric was better, customer count declined 0.1% q/q, capex was higher than expected, and gross margin missed.

- EBAY +5.1%: Rose after GameStop offered to acquire eBay for $55.5B in cash and stock, or $125/share, representing roughly a 20% premium to Friday’s close. GameStop said it already owns about a 5% stake and has a TD Bank commitment letter for up to $20B of debt financing.

Consumer Discretionary

- GME -10.1%: Fell after offering to acquire eBay for $55.5B in cash and stock. Investors appeared skeptical of the deal given eBay’s much larger scale and the financing complexity.

- NCLH -8.6%: Q1 revenue missed, EPS beat, Q2 guidance came in below consensus, and FY26 guidance was lowered. Management cited higher fuel-cost estimates, execution missteps, and softer demand tied to geopolitical uncertainty from the Iran war.

- LCII -8.6%: Fell after LCI Industries and Patrick Industries terminated merger-of-equals discussions that had been confirmed on April 17.

- Travel / leisure: Underperformed as Middle East-related demand and fuel-cost concerns weighed on the group.

- Retail / apparel and casual diners: Among the broader market laggards as risk appetite faded.

Consumer Staples

- TSN: Fiscal Q2 beat, driven by pricing-led revenue growth and strength in Chicken. The company raised FY profit and free-cash-flow guidance while leaving its revenue outlook unchanged.

- VITL -8.3%: Downgraded to neutral from buy at DA Davidson, with the firm citing rising egg supply pressure on prices as the company accelerates supply and capacity expansion.

- Household and personal care: Underperformed within Staples.

Energy

- Energy sector +0.85%: The only positive S&P 500 sector, supported by WTI crude’s 3.2% gain to $105.24 as geopolitical risk and Strait of Hormuz concerns remained elevated.

Financials

- BRK.B: Q1 revenue and EPS beat expectations, with insurance underwriting income up nearly 30%. Berkshire’s cash hoard stood just below $400B, nearly 40% of market cap.

- COIN +6.1%: Rose on reports that Senators Thom Tillis and Angela Alsobrooks reached a compromise on the Clarity Act to restrict stablecoin rewards equivalent to interest, potentially allowing the crypto legislation to advance.

- Banks / investment banks: Underperformed as higher yields, weaker risk sentiment, and tighter lending standards from the Fed’s SLOOS weighed on the group.

- Exchanges / private equity: Relative outperformers within Financials despite the sector’s broader weakness.

Healthcare

- CELC +15.4%: Phase 3 VIKTORIA-1 trial met its primary endpoint, showing clinically meaningful progression-free-survival improvement in the PIK3CA mutant cohort.

- AXSM +8.1%: Q1 revenue was in line and earnings were light, but analysts were positive on strong Auvelity and Sunosi results. The move followed Friday’s 11%+ gain after FDA approval of Auvelity for Alzheimer’s disease agitation.

- Biotech: Outperformed within Healthcare, helped by stock-specific trial and product news.

Industrials

- FDX -9.1%: Fell after Amazon announced Amazon Supply Chain Services, which expands Amazon’s logistics offering across freight, distribution, fulfillment, and parcel shipping.

- Logistics / trucking: Among the market’s weakest groups on the Amazon announcement and broader cyclical pressure.

- Building products: Laggards as higher yields and weaker housing sentiment weighed on the group

Eco Data Releases | Tuesday May 5th, 2026

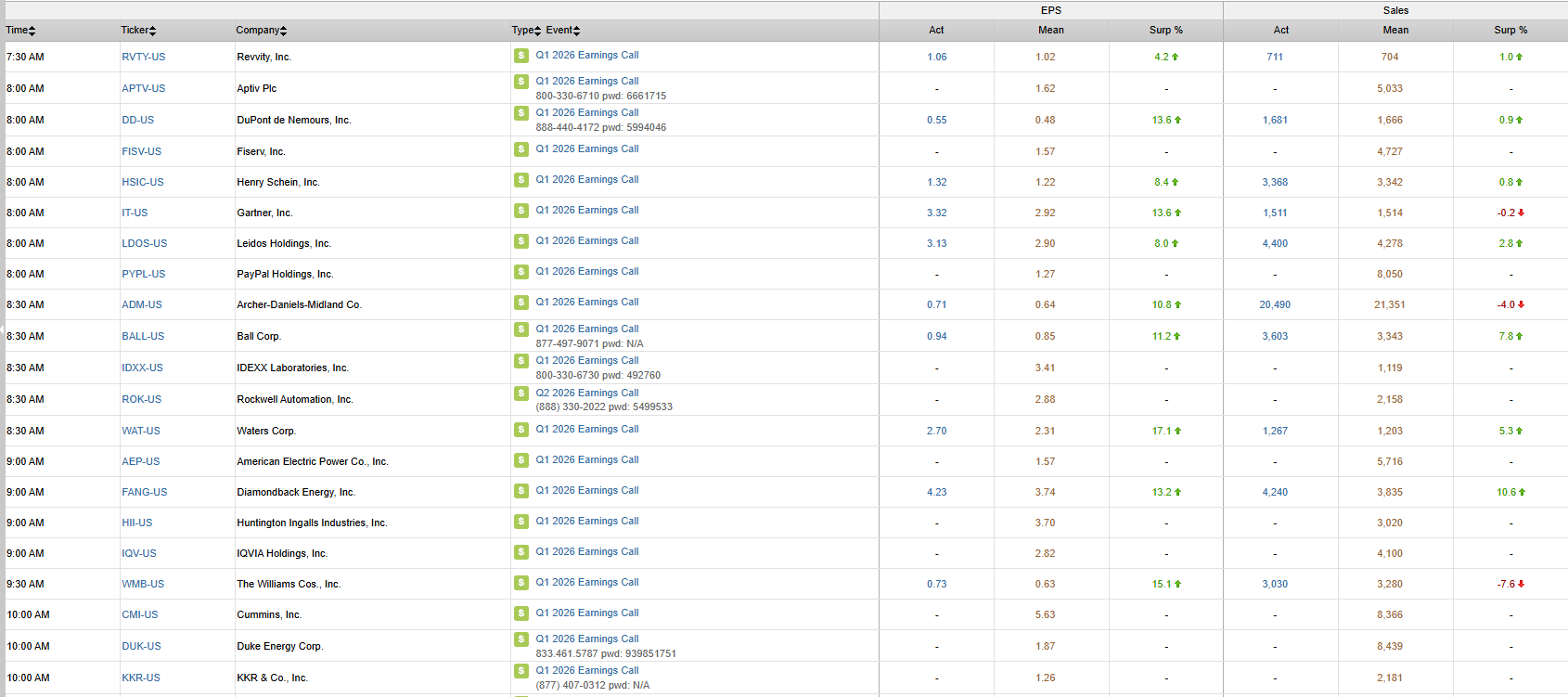

S&P 500 Constituent Earnings Announcements | Tuesday May 5th, 2026

Data sourced from FactSet Research Systems Inc.