The profit taking motive surfaced quickly with selling in TSLA and NVDA sparking broader redemptions in Mag7 positioning for the first time in July. The Dow led on the day adding 0.08% while big Tech and Mag7 selling contributed to a -1.95% correction for the Nasdaq while the S&P 500 was off 0.88%. With the performance spread between Growth and Value and Mega-Cap. and everything else so wide a day like this was a long time in coming. What remains a pertinent question is whether any rotation away from Mega-Cap. momentum leaders is sustainable. At first blush we would expect any near-term correction to be bought given the strength of the recent uptrend and the potential that FOMO buyers will see a correction as an opportunity to join the dominant trend. That view pre-supposes that earnings will continue to be robust for Mega-Cap. Growers and at present we support that view based on our work at ETFSector.com.

At the sector level the phrase “the first shall be last and the last shall be first” was apropos today. Real Estate led the Sectors higher backed by other YTD laggards XLU, XLB, XLI and XLE. Recent leaders XLK, XLC and XLY lagged the S&P 500 in a sharp reversal from YTD trends. Small and Mid-cap’s outperformed Mega-Cap’s and es-US stocks got a bid as well with the Russell 2000 adding 3.57% today. As always, we need to see some follow-through from laggard areas of the market to take them seriously, but today’s tape has our attention.

Away from equities, Crude climbed to $83.11 on the WTI contract while the Bloomberg Commodities Index added 0.32% and the 10yr yield ticked higher to 4.21% as high beta led the tape.

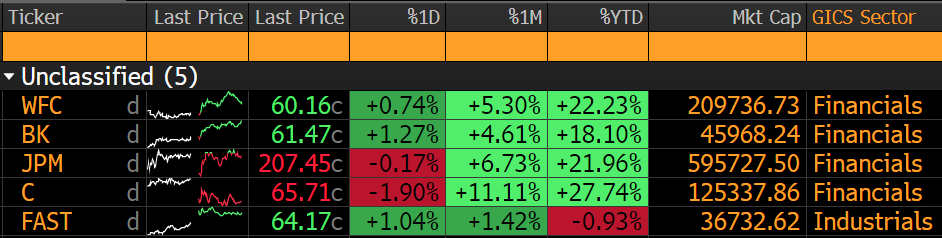

Producer Price Indices and University of Michigan surveys are on the economic calendar for Friday along with earnings releases from some of the biggest banks, JPM, WFC and C. The recent bank rally will be put to the test!

Eco Data Releases | Friday July 12th, 2024

| Date Time | Event | Survey | Actual | Prior | Revised | |

| 07/12/2024 08:30 | PPI Final Demand MoM | Jun | 0.10% | — | -0.20% | — |

| 07/12/2024 08:30 | PPI Ex Food and Energy MoM | Jun | 0.20% | — | 0.00% | — |

| 07/12/2024 08:30 | PPI Ex Food, Energy, Trade MoM | Jun | 0.20% | — | 0.00% | — |

| 07/12/2024 08:30 | PPI Final Demand YoY | Jun | 2.30% | — | 2.20% | — |

| 07/12/2024 08:30 | PPI Ex Food and Energy YoY | Jun | 2.50% | — | 2.30% | — |

| 07/12/2024 08:30 | PPI Ex Food, Energy, Trade YoY | Jun | — | — | 3.20% | — |

| 07/12/2024 10:00 | U. of Mich. Sentiment | Jul P | 68.5 | — | 68.2 | — |

| 07/12/2024 10:00 | U. of Mich. Current Conditions | Jul P | 66 | — | 65.9 | — |

| 07/12/2024 10:00 | U. of Mich. Expectations | Jul P | 69.3 | — | 69.6 | — |

| 07/12/2024 10:00 | U. of Mich. 1 Yr Inflation | Jul P | 2.90% | — | 3.00% | — |

| 07/12/2024 10:00 | U. of Mich. 5-10 Yr Inflation | Jul P | 3.00% | — | 3.00% | — |

S&P 500 Constituent Earnings Announcements by GICS Sector | Friday July 12th, 2024

Factor Friday

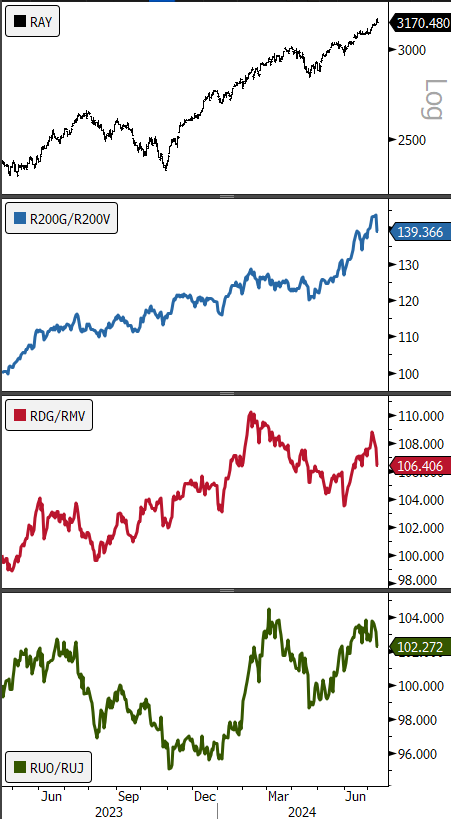

Thursdays reversal in big Tech was pervasive up and down the market cap. tiers as Value surged vs. Growth in each cohort.

- Russell 3000, 1yr, daily

- Panel2: Russell 200 Growth vs. Value

- Panel 3: Russell Mid-Cap Growth vs. Value

- Panel 4: Russell 2000 Growth vs. Value

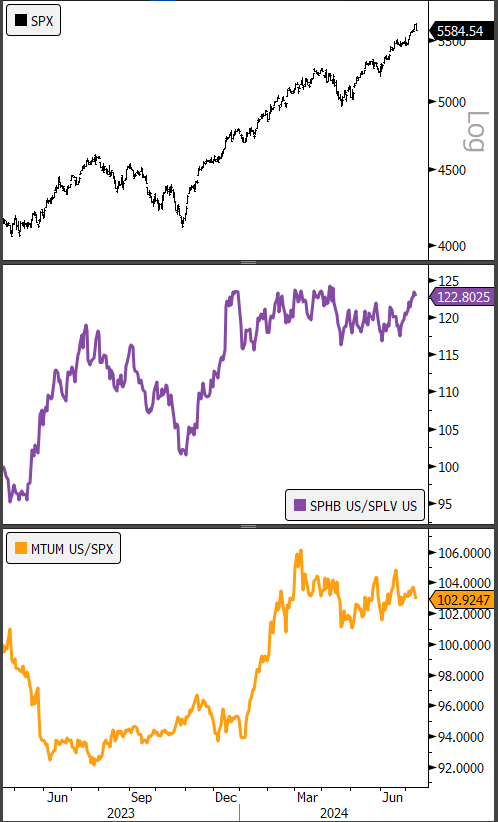

High-beta continues to gain the upper hand vs. min vol. stocks as the bull trend is spurring rotation into higher beta cyclicals over low vol. sectors. However we can see that Momentum is taking it on the chin with the relative performance of MTUM looking potentially distributional vs. The S&P 500. We aren’t ready to throw in the twol in the big momentum names just yet, but we would lower exposure on a break-down in the factor.

- S&P 500, 1yr, daily

- Panel2: High Beta vs. Low Vol.

- Panel 3: MTUM vs. S&P 500

Sources: Bloomberg