S&P futures up 0.2% in Tuesday morning trading. Comes after US equities finished mostly lower in quiet, lower volume session on Monday. Banks, credit cards, power, airlines, hotels and select managed care lagged. Energy, REITs, retail, builders, autos and solar outperformed. Treasuries weaker after strengthening on Monday. Dollar index down 0.2%. Gold up 0.1%. Bitcoin futures up 2.6%. WTI crude up 0.5%.

It’s a waiting game for election results. Still very busy in terms of earnings with the usual moving pieces. AI secular growth theme the bright spot. However, also some focus on weak guidance out of the semi space and continued softness in auto and industrial segments. Companies continue to implement cost-cutting/restructuring programs to protect margins. Overseas, China services growth rose to three-month high and Premier Li expressed confidence in hitting 5% growth target, helping drive a rally in Greater China shares. RBA left rates unchanged and South Korea inflation weakest since January 2021.

ISM services the highlight on the economic calendar this morning. Street looking for headline reading to slip to 53.8 from 54.9 in September, which was the highest since February of 2023. Treasury also selling $42B of 10-year notes today. On Wednesday, Treasury will sell $25B of 30-year bonds. Thursday brings Q3 nonfarm productivity and labor costs and initial claims. FOMC announcement and Powell press conference set for Thursday afternoon. Preliminary University of Michigan consumer sentiment (and inflation expectations) cap off the week on Friday, while Fed Governor Bowman is also scheduled to speak.

PLTR-US up big on “unrelenting” AI demand. NXPI-US guided below for Q4, flagging weaker macro. LSCC-US also guided Q4 below on continued industry headwinds. CRUS-US guided well below with some focus on tough comps. AZPN-US had a big miss on License and Solutions revenue, but EMR-US offered to acquire. MQ-US down big on regulatory drag. CE-US down big on miss, weak guidance and dividend cut with pressure on autos. CLF-US noted drag from two of its top four auto clients. JELD-US missed and cut guidance, noting deterioration in market conditions. WYNN-US EBITDA missed on Macau. BOWL-US up big on F&B revenue traction. VRTX-US beat and raised with focus on CF franchise strength and pipeline expansion. ILMN-US beat but tweaked down FY revenue guide on macro. HIMS-US had a big EBITDA beat and raised guidance. Outside of earnings, BA-US union approved new contract. DLTR-US announced CEO departure but reiterated Q3 outlook.

US equities were mixed on Monday, with the Dow down 0.61%, S&P 500 down 0.28%, Nasdaq down 0.33%, and the Russell 2000 up 0.40%. Despite starting lower, stocks recovered from their worst levels, following a Friday session where the S&P 500 marked its second straight weekly decline and the Nasdaq broke a seven-week winning streak. The weakness on Monday was concentrated in big tech, with underperformance across sectors such as banks, credit cards, hotels, media, airlines, energy (following FERC’s nuclear decision), tobacco, and some managed care stocks. Conversely, sectors including energy, REITs, agricultural chemicals, homebuilders, retail, beauty, industrial metals, autos, trucking, hospitals, and solar saw gains.

Treasuries strengthened, but yields flattened after a recent uptick. The Dollar Index fell by 0.4%, while Gold ended down 0.1% and Bitcoin futures declined 1.9%. WTI crude climbed 2.9% due to geopolitical concerns and delays in OPEC+ production plans. The market remained relatively subdued, awaiting key catalysts such as the US election, an anticipated 25 basis point rate cut from the Fed, the China NPC meeting, and earnings reports from 103 S&P 500 companies. Geopolitical tensions were also in focus, particularly with Iran potentially intensifying its response to Israeli airstrikes.

In economic data, factory orders saw a decline in line with expectations, marking the fourth drop in five months. The Treasury’s $58 billion 3-year note auction tailed, with strong foreign demand, and more auctions for 10-year and 30-year bonds are scheduled this week. Other upcoming data highlights include ISM services on Tuesday, Q3 nonfarm productivity and labor costs on Thursday, along with the FOMC announcement and Powell’s press conference. The University of Michigan consumer sentiment report is due Friday.

Company News by GICS Sector

Communication Services

- Fox Corp. (FOXA): Up 2.7% following a quarterly earnings and revenue beat, driven by record political advertising and accelerated revenue growth at Tubi. Affiliate fee revenues also increased, with notable growth in both television and cable networks.

- New York Times (NYT): Fell 7.7% despite a revenue and earnings beat, as digital subscription growth decelerated. A potential strike by the company’s tech union could affect its election coverage.

Consumer Discretionary

- Tesla (TSLA): Declined 2.5% as China-made electric vehicle sales dropped over 5% year-over-year in October, with additional reports noting increased competition from Chinese EV manufacturers.

- Yum China Holdings (YUMC): Gained 7.2% on better-than-expected Q3 EPS and revenue, despite missed comparable sales at both KFC and Pizza Hut. The company plans to double capital returns by 2026.

- Chewy (CHWY): Rose 6.3% after the announcement of its addition to the S&P MidCap 400, replacing Stericycle.

- Peloton Interactive (PTON): Up 3.6% after an upgrade to “Buy” from Bank of America, citing potential Q1 EBITDA upside and improved FY25 guidance.

Consumer Staples

- Freshpet (FRPT): Increased 12.6% on Q3 earnings and revenue beats, citing improved household penetration and lower input costs, leading to raised FY guidance.

Energy

- Constellation Energy (CEG): Dropped 12.5% following a regulatory decision against Talen’s supply plan to Amazon’s data center, impacting power stocks broadly. The company raised FY EPS guidance by 2.5%.

Financials

- Affiliated Managers Group (AMG): Decreased 8.6% on weaker-than-expected Q3 earnings and revenue, with lower performance fees and softer net inflows.

Health Care

- Zoetis (ZTS): Fell 3.7% despite a beat on Q3 revenue and earnings, driven by Companion Animal and Livestock segments, though FY guidance raised less than expected.

- DigitalOcean Holdings (DOCN): Down 13.5% despite positive Q3 earnings, as Q4 guidance missed consensus and growth in high-spending customer segments flagged below historical levels.

Industrials

- Air Transport Services Group (ATSG): Jumped 26.4% on news of a $3.1 billion acquisition offer from Stonepeak, pricing the stock at $22.50 per share.

Information Technology

- Entegris (ENTG): Declined 5.7% after missing Q3 revenue, earnings, and margins, with a longer-than-expected market recovery and weaker tech transitions.

- Intel (INTC): Down 2.9% as the company will be removed from the Dow Jones Industrial Average on November 8.

Materials

- Chemours (CC): Rose 15.5% on Q3 EPS and revenue beats, with strong growth in Opteon Refrigerants. The company outlined a strategy including $250 million in cost savings over three years.

- Mosaic (MOS): Increased 5.4% following comments from Belarus regarding a potential 10-11% potash output cut, which could significantly impact potash markets.

- Sherwin-Williams (SHW): Gained 4.6% as the company was announced to replace Intel in the Dow Jones Industrial Average starting November 8.

Real Estate

- Retail Opportunity Investments (ROIC): Up 7.8% on news that Blackstone is in advanced talks for a potential acquisition, which could be finalized in the coming weeks.

Eco Data Releases | Tuesday November 5th, 2024

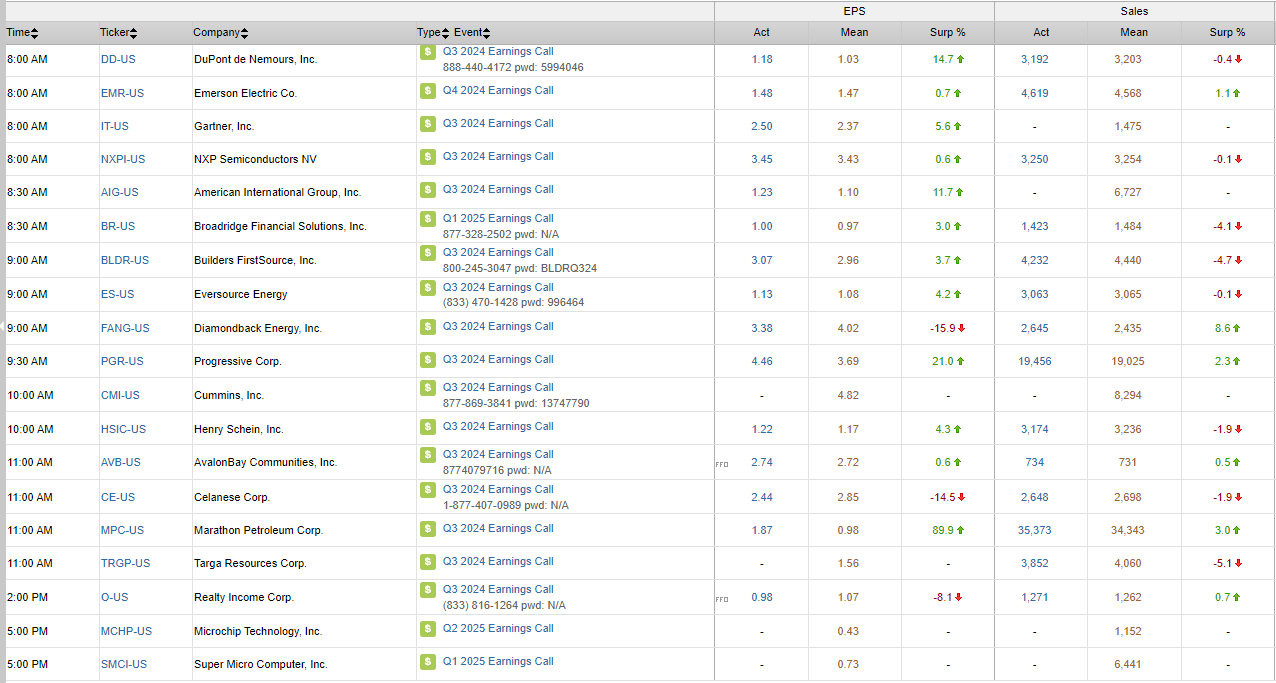

S&P 500 Constituent Earnings Announcements | Tuesday November 5th, 2024

Data sourced from FactSet Research Systems Inc.