October 3, 2025

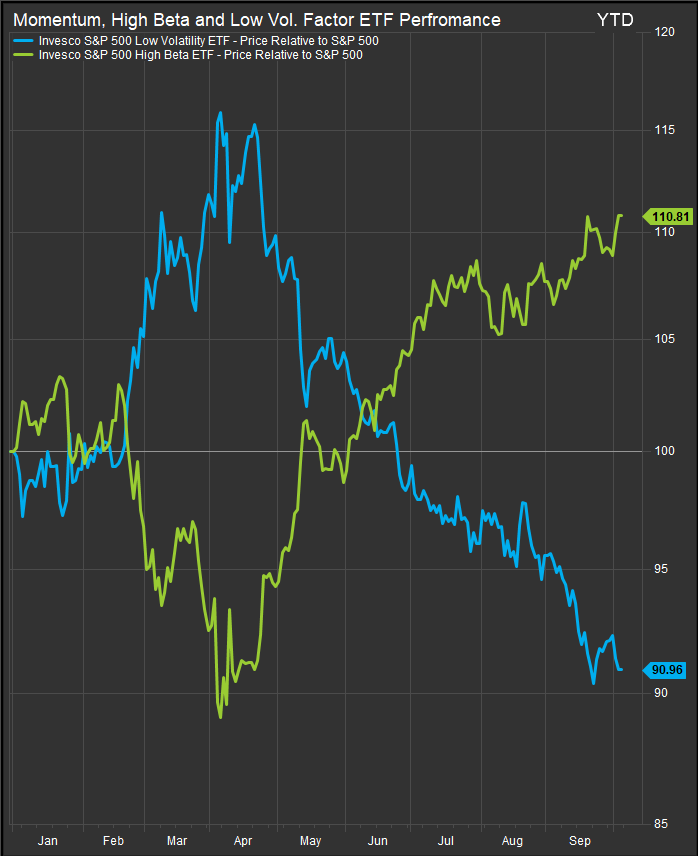

Equities continue to push higher as the calendar has flipped to October. The AI trade remains ascendant amidst a backdrop of an easing Fed, moderating rates and continued firm investor risk appetite. It should be no shock then that in 2025, high-beta stocks have strongly outperformed low-volatility names. We go a bit deeper into high beta investing in this week’s column.

High Beta vs. Low Vol.

A useful place to begin is by noting that beta is a measure of how much a stock’s returns move relative to the market: a beta above 1 suggests it is more volatile than the market, while below 1 suggests it is more defensive. Corporate Finance Institute+1

Across U.S. equities, the three sectors commonly identified as having the highest systematic beta are Information Technology, Financials, and Industrials (i.e. capital goods, machinery, aerospace, transportation, etc.). Many high-beta names cluster in these sectors because they have strong leverage to economic cycles, capital expenditure trends, and investor sentiment generally shapes their performance trends. Recent analyses from FTSE Russell show that sector betas shift over time in response to structural changes in the economy (for example, the increasing weight of technology or shifts in regulation) and that industries actively exposed to growth and disruption tend to move more aggressively with the market. LSEG

In the Technology / IT sector, some of the highest-beta equities cited in screens and commentary include Super Micro Computer (SMCI), Palantir Technologies (PLTR), NVIDIA (NVDA) and Broadcom (AVGO) as part of crowded high-beta technology exposure. JPMorgan’s crowding analysis flagged SMCI as having a beta ~3.37 and also called out PLTR, Coinbase, NVIDIA, and Broadcom as among the most crowded high-beta names. Business Insider SMCI, in particular, has been highlighted in investment media as a “hyper-growth” tech stock riding AI / infrastructure demand. The Motley Fool+1

SMCI

PLTR

In the Financials sector, elevated betas tend to arise in asset managers, private equity / alternative firms, and capital markets–sensitive businesses. Publicly cited high-beta financial names include KKR & Co. (KKR) and Blackstone (BX), which benefit from volatility in deal activity, capital raising, and credit markets. (These names also feature in high-beta stock rankings such as those on SureDividend’s 2025 list.) Sure Dividend. Asset managers like BX and KKR are often seen as bellwethers for the “risk on” trade. This is because they are involved with funding and credit for a broad range of businesses through credit issuance and private equity. If consolidations in these stocks resolve negatively, that may be an indication that investor sentiment is weakening.

KKR

BX

Within the Industrials sector—the classic providers of machinery, aerospace, defense, and infrastructure exposure—some high-beta names emerge. For example, Caterpillar (CAT) is frequently used as a bellwether for cyclical industrial demand tied to infrastructure, mining, and heavy equipment spending. Deere & Co. (DE), with exposure to agricultural and construction equipment cycles, also tends to exhibit above-average beta in periods of industrial expansion. Boeing (BA), though also tied to aerospace and supply chain cyclicality, often moves with amplified volatility in response to order cycles, global trade sentiment, and defense spending. (Note: exact contemporary beta figures vary depending on lookback window and data source.)

CAT

BA

In U.S. equity markets, the Energy sector carries one of the highest betas among the S&P 500 groups, reflecting its amplified response to swings in oil and gas prices. Sector-level studies put Energy’s beta at roughly 1.2 versus the S&P 500 benchmark【icfs.com】, meaning that a 1% market move tends to translate into a 1.2% move in Energy stocks on average. The Materials sector also runs above market beta, with NYU Stern’s data showing Building Materials companies at ~1.36 and Basic Chemicals at ~1.15【pages.stern.nyu.edu】.

This elevated beta is driven by direct exposure to commodity cycles. In Energy, shifts in crude oil and natural gas prices flow immediately through revenues and earnings for exploration, production, and services firms, amplifying equity volatility. In Materials, copper, steel, and chemical producers exhibit similar leverage to commodity price changes, outperforming sharply during upcycles but underperforming when prices weaken. Commodity exposure thus acts as a structural driver of higher beta, making Energy and Materials sectors more cyclical and more volatile than the market as a whole

Why are high-beta names outperforming now? First, the broader equity environment has been favorable—strong upward trends amplify the leverage inherent in high-beta names. Second, investor flows and factor rotations have skewed towards momentum, growth, and thematic exposures (e.g. AI, semiconductors, fintech), which disproportionately inhabit the high-beta space. Third, expectations for monetary easing or lower discount rates reward growthier, more volatile equities more than stable, defensive ones. And finally, many of the names now trading with extreme beta are subject to crowded positioning. JPMorgan’s research warns that “extreme crowding episodes,” particularly in tech and high beta names, raise downside risk if sentiment reverses. Business Insider

If selecting among high-beta names, the ideal candidates pair volatility with structural tailwinds, resilient balance sheets, and potential for durable earnings upside. For example, SMCI is compelling due to its direct tie to AI and data infrastructure growth, though risk is high. PLTR is attractive for its positioning in government / enterprise AI and data contracts, but faces dependency on contracts and regulatory sentiment. KKR offers a way to play beta through financial cycles and alternative asset exposure, with more diversified business lines. On the industrial front, CAT or DE may offer more durable exposure to infrastructure and cyclicality than purely speculative names. Regardless of choice, understanding the drivers of the high beta trade and taking some precautions to balance out a portfolio when those drivers change are important components of successful high beta investing.

Conclusion

When high beta outperforms, investors are demonstrating confidence in the sustainability of current conditions. Elevated confidence risks crowding into certain stocks, sectors and industries, but crowds also push stocks to their best performance. Investors need to be able to manage risk by understanding the drivers of enthusiasm for outperforming high beta cohorts. In the current environment, the AI trade and tariff implementation are two sources of volatility and outperformance. They are viewed optimistically because there is an expectation that rates are moving lower to support moderating economic growth in the US. If those underlying macro conditions change and rates start moving higher on inflation, or the cadence of economic data releases shows a change in behavior, the high beta trade could move from a boon to a bust. We think investors should be focusing on the level of interest rates and risk appetite gages to evaluate whether the environment continues to be right for high beta investing. The behavior of banks and asset managers who provide the credit mechanism for speculative investments are also useful as a sentiment indicator.

Bibliography

- “2025 High Beta Stocks List | The 100 Highest Beta S&P …”, SureDividend (June 2025) Sure Dividend

- “Why JPMorgan says it’s getting riskier to hold the market’s most popular stocks,” Business Insider Business Insider

- “US equity market betas – why they matter and how they are changing,” FTSE Russell / LSEG LSEG

- “Beta – What is Beta (β) in Finance? Guide and Examples,” Corporate Finance Institute Corporate Finance Institute

- “3 Hyper-Growth Tech Stocks to Buy in 2025,” Yahoo Finance / media references ICFS: S&P 500 Sectors: Beta, Correlation, R² & Weightings (icfs.com)

- NYU Stern: Betas by Sector (pages.stern.nyu.edu

Other Data sourced from FactSet Research Systems Inc.