April 17, 2026

The last week of equity market price action made one point hard to miss: the market has been acting like a Growth market, even if the macro environment itself is not yet clean enough to dismiss Value. That distinction matters. A style call should separate what the tape is rewarding now from what the broader economy and policy mix are likely to sustain over a longer horizon.

Based on this week’s developments, the near-term answer is that the macro backdrop is more supportive of Growth than Value, but in a selective, conditional way. This has not been a broad cyclical or deep-value revival. It has been a rally led by software, semiconductors, mega-cap technology, AI infrastructure, and other long-duration growth exposures, while breadth remained narrow and equal-weight performance often lagged the headline indexes. Across the market updates you shared, the consistent pattern was clear: software rebounded sharply, AI-linked beneficiaries regained leadership, and the biggest index gains were repeatedly concentrated in a small set of large-cap growth franchises. The headlines showed a tape being driven by a mix of AI enthusiasm, systematic re-risking, and falling near-term geopolitical fear rather than a classic value-led upswing in economically sensitive cheap sectors.

That conclusion starts with price action. Over the week, the S&P 500 and Nasdaq repeatedly pushed to fresh highs, while the Nasdaq logged an unusually long winning streak and software put together one of its strongest bursts in months. At the same time, several of the updates stressed that only a handful of sectors were doing the heavy lifting, with equal-weight indexes frequently lagging and breadth remaining unimpressive. That is usually not what a durable Value regime looks like. Value leadership tends to come with broader participation from banks, industrials, materials, energy, and other shorter-duration cash flow businesses. This week’s tape instead looked like a market rediscovering confidence in secular growth stories, especially those tied to AI demand, compute spending, and digital infrastructure.

The macro news helped enable that rotation. This week’s developments pointed to a market increasingly comfortable with a de-escalation narrative around the Middle East, or at minimum more comfortable that the worst-case outcomes were becoming less likely. In your updates, the dominant macro explanation for the rally was the same every day: expectations for a durable ceasefire, reduced immediate tail risk, and meaningful re-risking by systematic strategies after prior de-grossing. That matters for style leadership. When geopolitical fear recedes and investors become less worried about immediate downside shocks, the first beneficiaries are often the highest-beta and longest-duration parts of the market. This week, that meant Growth.

There was also enough in the economic data to justify the move. The March producer price report was softer than expected, with headline PPI up 0.5% month over month versus 1.1% expected and core PPI rising only 0.1%. Initial jobless claims remained low at 207,000, while the Philadelphia Fed’s April manufacturing index rose to 26.7, its highest reading since January 2025. The Fed’s Beige Book described activity as increasing at a slight to modest pace in much of the country. None of that describes a collapsing economy. Rather, it points to a still-functioning macro backdrop in which investors can continue paying for earnings visibility and secular growth, particularly when those earnings are linked to large capex cycles such as AI infrastructure and compute.

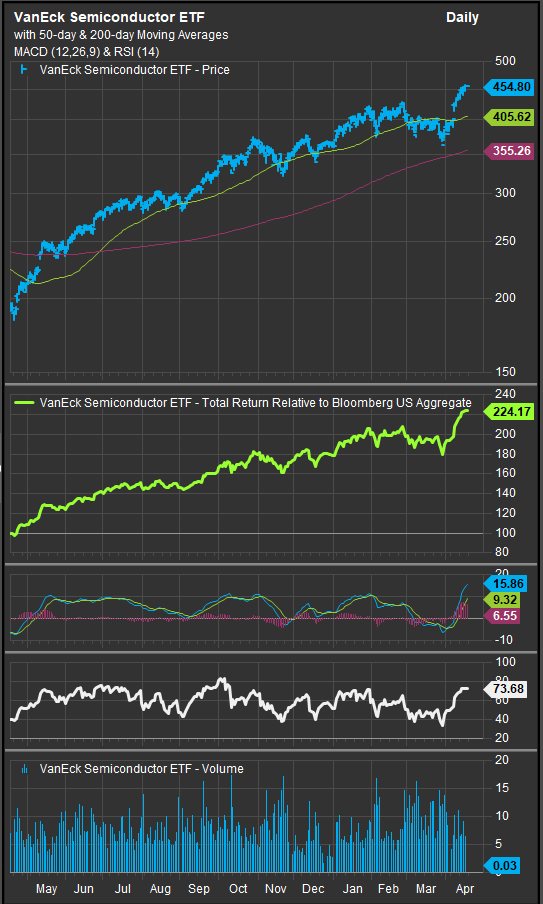

This week’s developments also reinforced the specific thematic areas that favor Growth over Value. The headlines repeatedly emphasized better AI demand commentary, chip and compute partnerships, software rebounds, and renewed confidence in private credit and capital markets. TSM raised guidance and talked up robust AI demand. AVGO extended its partnership with META. ORCL announced a multicloud collaboration with AWS. GTLB rallied on its Google Cloud tie-up. Software as a group staged a dramatic rebound after having been one of the market’s major pressure points. This is a critical point for style analysis: the market is not just buying “technology” in a vague sense. It is buying the belief that AI capex remains real, broad, and durable enough to support premium multiples. That is one of the strongest macro-to-style transmission channels favoring Growth today.

Semiconductors have remained the core of the AI trade.

Software funds are bouncing from deeply oversold conditions. The technical setup remains challenged, as there are likely plenty of trapped longs that may look to any relief rally as a chance to exit positions.

Still, the argument is not one-sided. The broader macro regime remains mixed enough that Value retains an important strategic case. Treasury yields moved higher on several days, oil remained elevated even after some pullbacks, and inflation-sensitive components of regional surveys were not especially comforting. Consumer and housing signals were also less clean. Homebuilder sentiment weakened, and policymakers continued to emphasize uncertainty. Reuters reported that the University of Michigan’s preliminary April consumer sentiment gauge fell sharply, while inflation expectations moved higher, underscoring that households are still uneasy about the outlook. Reuters also reported that Fed officials remain cautious, with the policy path still clouded by war-related uncertainty and the inflation implications of tariffs and energy. A higher-for-longer rate environment is rarely an unqualified tailwind for Growth, especially after a rapid rally in long-duration equities.

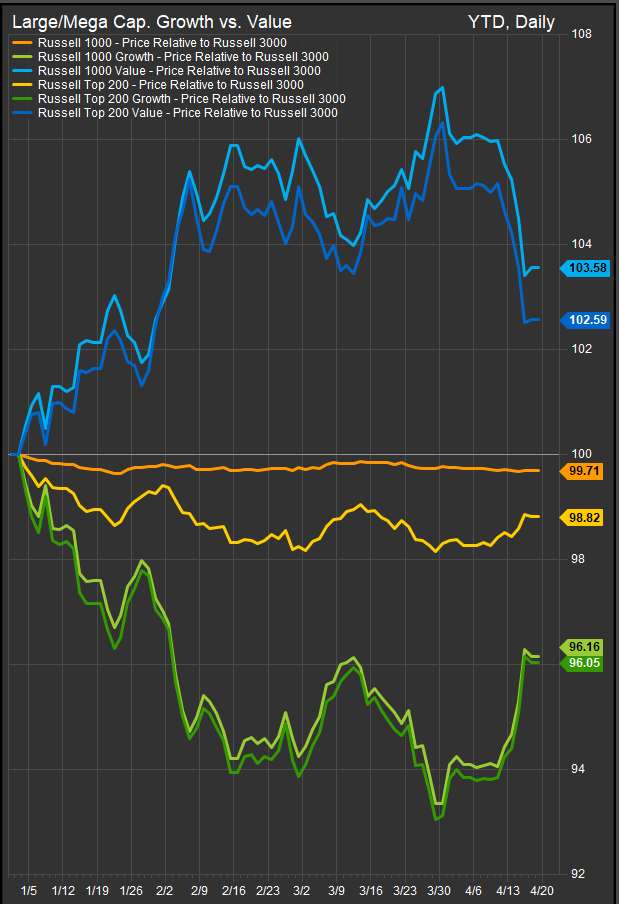

That is why the most useful answer is not binary. Tactically, the macro environment supports Growth. Strategically, it still argues for balance. The official ETF performance data tell that story well. Even after this week’s surge in Growth leadership, style benchmarks still show that Value had maintained an edge year to date through mid-April. The iShares S&P 500 Growth ETF showed a 2.60% YTD NAV total return as of April 15, while the iShares S&P 500 Value ETF was at 3.22%. Vanguard’s large-cap style proxies showed an even bigger gap, with Vanguard Growth slightly negative year to date while Vanguard Value remained strongly positive. In other words, the tape this week favored Growth, but the broader 2026 environment has not been uniformly growth-friendly.

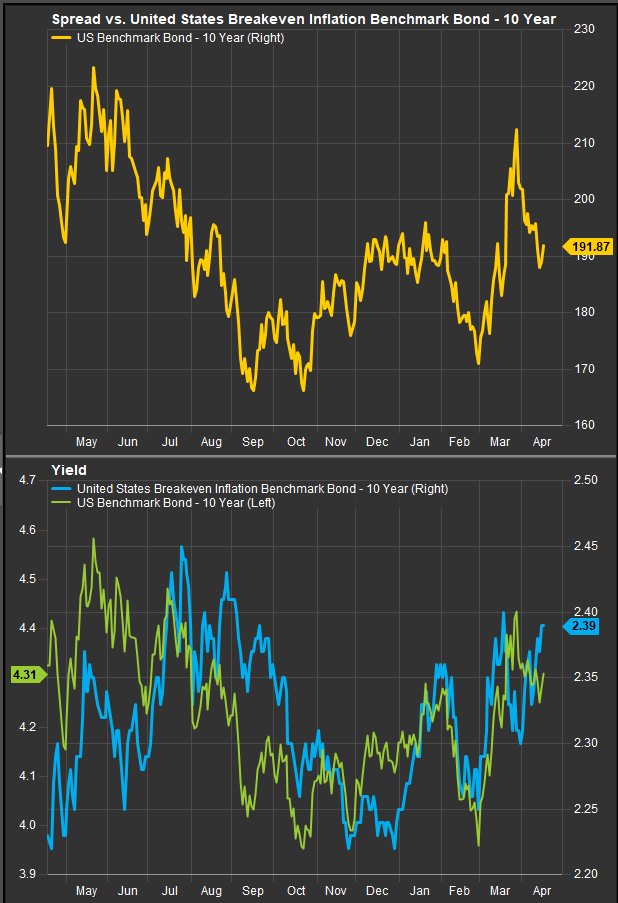

From a macro perspective, Growth stocks have typically outperformed when real rates (top panel) move lower.

That divergence is the heart of the editorial judgment. The market’s recent behavior says investors are willing to pay up again for growth when three conditions hold: first, geopolitical risk is moving from escalation toward containment; second, macro data are good enough to keep recession fears from dominating; and third, AI demand remains strong enough to justify a premium multiple structure. All three conditions were visible in this week’s developments. But none of them has been secured beyond doubt. Breadth was still narrow. Equal-weight indexes often lagged. Several sessions depended heavily on big tech and software. That is not the profile of a fully healthy style rotation. It is the profile of a market embracing selective Growth leadership while still hedging, implicitly, against a more difficult macro path.

Our conclusion is that the macro environment, as reflected in this week’s developments and corroborated by current market and style data, supports Growth over Value right now, but mainly as a tactical call rather than a regime call. The combination of softer inflation data, resilient activity, easing geopolitical anxiety, systematic re-risking, and powerful AI capex headlines has created a window in which Growth can outperform. But the persistence of higher yields, uneven breadth, and unresolved inflation and policy risks means Value should not be dismissed. Growth is winning the current vote of the market. Value still has a claim on the longer-term debate. Market internals also show a setup where investors have been pushing the index higher, but stock level trends still show negative breadth divergence.

Participation in the rally has remained narrow relative to April/May of 2025. Only 50% of stocks are with the index above their respective 200-day moving averages.

For professional investors, that means resisting the temptation to frame the choice too cleanly. The better formulation is that this week’s headlines favored Growth, while the broader macro environment still demands some Value discipline. That is why the most credible stance today is not an outright abandonment of Value, but an acknowledgment that the market’s center of gravity has shifted back toward Growth leadership for as long as de-escalation, macro resilience, and AI demand remain intact.

Data sourced from FactSet Research Systems Inc., Reuters, Blackrock

Note: The contents of this article are for informational purposes only and do not constitute investment advice.