December 14, 2025

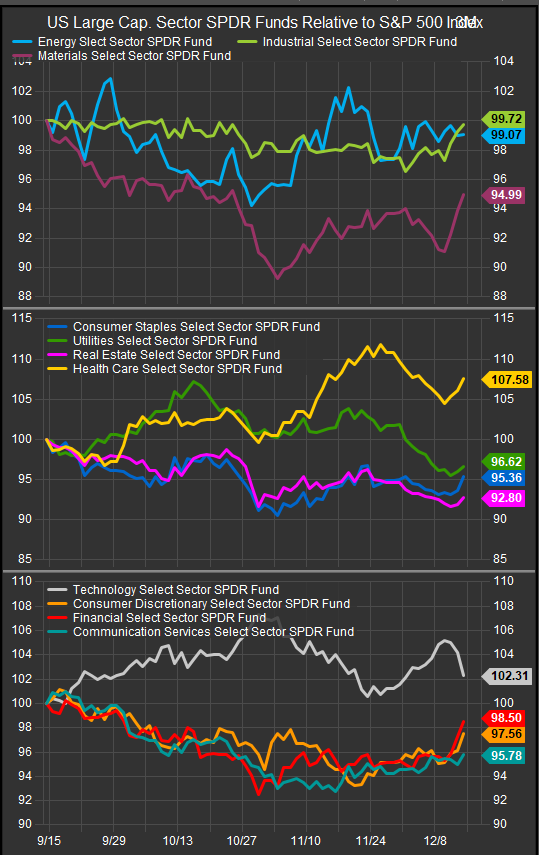

U.S. equities are closing the year at an inflection point that feels deceptively calm. Markets have absorbed a December 25 bp Federal Reserve rate cut and a renewed Treasury bill purchase program designed to stabilize reserves, while risk assets have responded with improved sentiment, better breadth, and renewed inflows. On the surface, this looks like the familiar late-cycle handoff: monetary policy easing just as growth slows. The real question for investors, however, is whether Federal Reserve action alone is enough to tip the scales in favor of sustained equity upside—or whether the economy still needs several other things to go right. At present market breadth is expanding (chart below) as rotation out of the Technology sector has benefitted a broader group of companies with investors seeing the recent rate cut as a boost.

The Fed’s latest move was deliberately calibrated. Policymakers emphasized that bill purchases—running at roughly $40 billion per month, with reinvestments pushing near-term liquidity additions higher—are reserve management, not quantitative easing. Chair Powell also pushed back against fears of renewed inflation, highlighting productivity gains and a still-functional labor market. Yet at the same time, he acknowledged growing uncertainty in the data, notably suggesting that recent payroll figures may be systematically overstated, potentially by as much as 60,000 jobs per month. If accurate, that would imply the economy is closer to flat or slightly contracting job growth than headline numbers suggest.

This ambiguity shows up clearly in the labor-market mosaic. Weekly initial jobless claims jumped to 236,000, the highest since early September, while continuing claims fell to their lowest level since April, underscoring how noisy and difficult-to-interpret the data have become around the holidays. Surveys tell a similarly mixed story. Small business optimism improved modestly in November, but pricing pressures surged: the share of firms raising average selling prices posted the largest monthly increase on record, hinting that inflation risks tied to tariffs and supply chains may not be fully extinguished.

Earnings, for now, remain the market’s strongest pillar. According to FactSet, Q4 S&P 500 earnings growth is tracking near 8% year-over-year, and—unusually—the bottom-up estimate has risen during the quarter rather than falling. That supports equity valuations in the near term, but it also raises the bar. With estimates no longer being sanded down, companies now need to deliver. Any broad-based disappointment would quickly revive concerns that monetary easing is arriving too late to prevent a profit slowdown.

Trade and geopolitics remain another swing factor. Recent reporting suggests that tariff carveouts now exempt roughly half of U.S. imports, muting the near-term inflation impact of existing trade measures. That is constructive, but it also creates legal and political uncertainty—particularly as courts review executive authority and as trade policy becomes increasingly entangled with election-year politics. Meanwhile, U.S.–China tensions have eased at the margin, including approvals related to advanced chip exports, but scrutiny around AI supply chains and national security remains intense.

This tension is especially visible in the technology and AI complex. On one hand, earnings momentum and capital investment remain strong, with AI demand continuing to drive order books and revenue guidance. On the other, recent disappointments—most notably in cloud and infrastructure capex profitability—have reminded investors that not every dollar of AI spending converts cleanly into free cash flow. With positioning elevated and sentiment recently rebounding sharply, the AI trade is increasingly sensitive to marginal negative surprises.

At the sector level we can see near-term rotation out of the Tech sector flowing through to Commodities, Cyclicals and some low vo. Exposures.

So, should investors be defensive?

An outright defensive posture risks missing continued upside if easing financial conditions, resilient earnings, and fading inflation fears reinforce the rally. But a fully aggressive stance ignores the growing list of late-cycle vulnerabilities: softer labor trends, rising political and trade uncertainty, crowded positioning, and a market increasingly reliant on a narrow set of earnings drivers. The more prudent approach appears to be selective defense—we think low vol. equity sectors remain near-term accumulation opportunities. We also like Energy and Materials sectors as they’ve historically worked when commodities prices rise as they are currently. While the strongest long-term trend remains with Growth and Technology shares. We think a rebound there remains in play as long as interest rates don’t move sustainably higher.

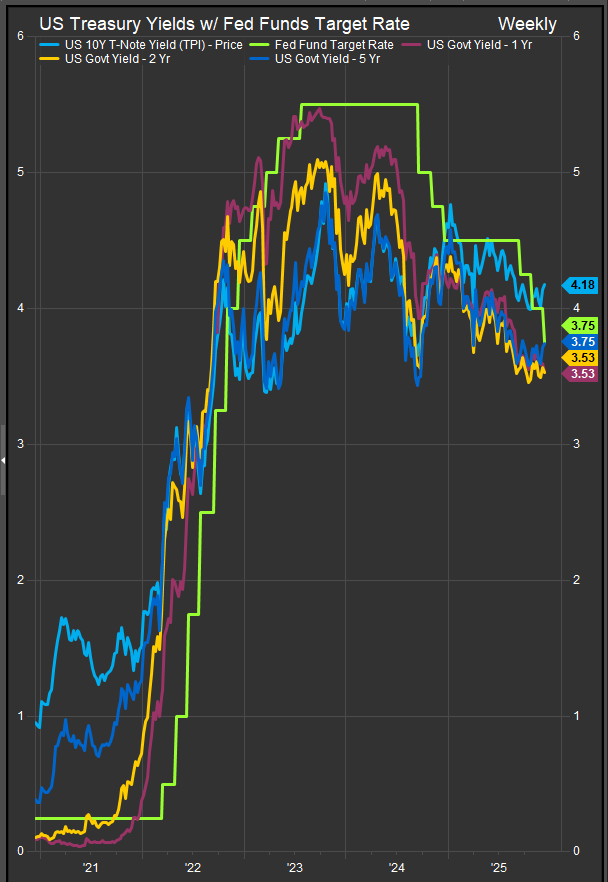

Our near-term concern is that the Fed is somewhat boxed in. Longer duration yields are already above the target rate, commodities prices are rising and costs are stubbornly high. The chart below shows how tight the market has interest rates to the policy rate. There isn’t much margin for error.

Ultimately, Federal Reserve policy can tilt the playing field, but it cannot carry the market alone. For equities to extend gains meaningfully from here, earnings must validate optimism, inflation must continue to cool without reaccelerating, and trade policy must avoid reintroducing a cost shock. If those conditions hold, risk assets can grind higher. If they don’t, the gap between supportive policy and a sagging economy will become harder for markets to ignore.

Endnotes / Sources

- Federal Reserve, December FOMC statement, press conference, and Summary of Economic Projections (December 2025).

- Bloomberg; Reuters – coverage of December FOMC, Treasury bill purchases, and Fed commentary on labor-market data quality.

- U.S. Department of Labor – Weekly Initial and Continuing Jobless Claims (December 2025).

- FactSet Research Systems – Earnings Insight: S&P 500 Q4 2025, estimate revisions and growth rates.

- National Federation of Independent Business (NFIB) – Small Business Optimism Index, November 2025.

- Financial Times; Politico – reporting on U.S. tariff carveouts, refund risks, and trade-policy mechanics.

- Bloomberg – AI sector sentiment, earnings reactions, and positioning commentary.

- Goldman Sachs – sentiment and positioning indicators (AAII, NAAIM, hedge fund exposure summaries).

Charts and additional data sourced from FactSet Research Systems inc.