The sector outlook is improving, but the market is no longer responding to AI as a narrow semiconductor story. The latest news points to a broader investment theme: AI electricity consumption is becoming a forward-demand driver for Technology, Industrials, Utilities, Financials and select Materials.

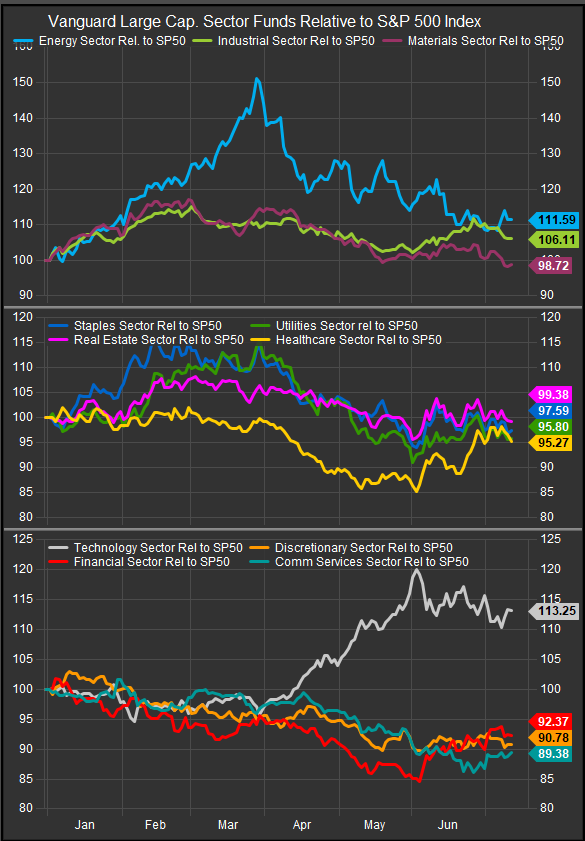

Chart: The AI/Technology Trade has been on pause since June, but Industrials, Healthcare, Financials and Utilities have firmed in the interim.

That is the most important sector takeaway from the week. Momentum has stabilized, Meta is reportedly looking to expand compute capacity to 14GW by 2027, Mark Zuckerberg pushed back against excess-capacity concerns by saying the company needs all the compute it can get, and Nvidia rallied on reports China may permit limited purchases of H200 chips by top AI firms. At the same time, the Fed is increasingly focused on whether AI-related demand becomes an inflationary force, with NY Fed President Williams flagging AI as both a potential productivity boost and a possible upside risk to inflation if demand outpaces supply.

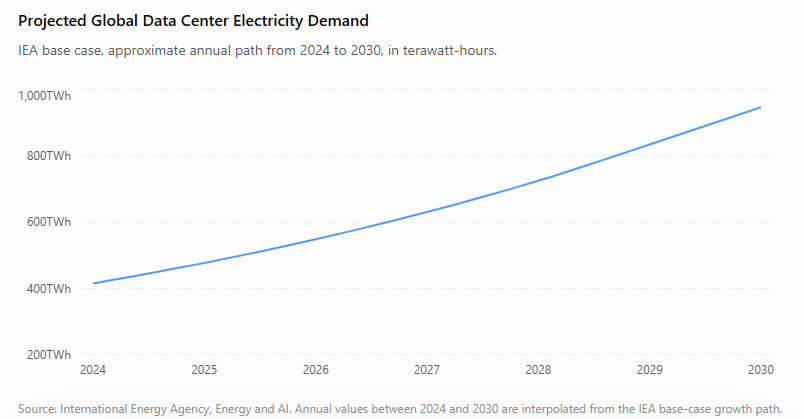

The electricity math helps explain why this matters. The International Energy Agency’s base case projects global data-center electricity consumption more than doubling to roughly 945 TWh by 2030, up from about 415 TWh in 2024. That implies data centers move from roughly 1.5% of global electricity demand toward just under 3% by 2030, growing far faster than overall electricity consumption.

Chart: AI-related data center demand is set to more than double by 2030 from 2024.

For sector investors, that changes the AI playbook. The first phase of the AI trade rewarded compute. The next phase has to fund power, cooling, grid access, transmission, backup generation, electrical equipment, and data-center construction. That means AI demand is moving from the income statements of a few megacap technology companies into the order books of industrial, utility and infrastructure companies.

Vanguard Information Technology (VGT) still sits at the center of the trade. Semiconductors, memory, equipment, networking and hyperscale platforms remain the cleanest beneficiaries of AI capex. Nvidia, Broadcom, AMD, Micron, Applied Materials, Lam Research, KLA, Microsoft, Meta, Alphabet and Amazon remain core examples. However, the bar is higher than it was earlier this year. Samsung’s weakness despite a large profit increase shows that investors now need upside that beats already-elevated expectations. The Technology opportunity remains strong, but it is narrower: favor AI hardware and hyperscale platforms over software businesses that could be disrupted by in-house AI tools.

Vanguard Industrials (VIS) may be the most important second-order beneficiary. AI data centers require transformers, switchgear, cooling, engineering, construction, automation, turbines, backup systems and transmission infrastructure. That supports companies such as Eaton, Vertiv, Quanta Services, GE Vernova, Hubbell, Caterpillar, Emerson and Parker-Hannifin. Industrials are becoming the practical expression of AI demand: less about model capability and more about whether the grid can physically support the next wave of compute.

Vanguard Utilities (VPU) deserves a more nuanced upgrade. Utilities remain rate-sensitive, so elevated yields can still cap near-term multiples. But AI load growth creates a structural demand story that the sector has not had in years. Regulated utilities with strong grid-investment pipelines, independent power producers, nuclear-linked names and gas-fired generation beneficiaries should see better forward demand if data-center growth continues. Constellation Energy, Vistra, NextEra Energy, Southern, Duke and other power providers tied to load growth should remain on sector investors’ radar.

Vanguard Materials (VAW) also becomes more relevant, but selectively. AI power demand requires copper, aluminum, specialty chemicals, aggregates, steel, electrical components and construction materials. The better Materials exposure is not broad commodity beta; it is infrastructure-linked demand. Freeport-McMoRan, Southern Copper, Nucor, Vulcan Materials, Martin Marietta and select specialty chemical companies are better aligned with AI buildout than gold/mining hedges or purely cyclical commodity exposure.

Vanguard Financials (VFH) benefits indirectly. The AI power buildout is capital intensive, and the market brief points to bank earnings focus on capital markets, investment banking, trading, loan growth and AI-related equity and debt issuance. If data-center financing remains active, large banks, brokers, exchanges and insurers can participate through advisory fees, underwriting, lending, trading activity and capital-market infrastructure. JPMorgan, Bank of America, Wells Fargo, Goldman Sachs, Morgan Stanley, CME, ICE, Chubb and Progressive remain the more relevant Financials exposures.

The inflation and Fed angle is the main constraint. ISM Services still shows resilient demand, and prices paid eased but remained elevated. The June FOMC minutes kept rate hikes in play, and inflation risks tied to AI demand, Middle East conflict and tariffs remain part of the policy discussion. A cooler CPI print would help rate-sensitive sectors such as Vanguard Real Estate (VNQ), Vanguard Utilities (VPU) and biotech within Vanguard Health Care (VHT). A hotter print would likely push investors back toward quality balance sheets, banks, profitable AI infrastructure and companies with pricing power.

Consumer sectors look more mixed. Delta’s guidance reinforces that travel demand remains healthy, which supports selective exposure within Vanguard Consumer Discretionary (VCR). But Pepsi’s comments about tighter U.S. consumer budgets and Costco’s slower comp growth show inflation fatigue is still a headwind. Vanguard Consumer Staples (VDC) provides defensive stability, but the group is not immune to valuation pressure or margin scrutiny when rates stay elevated.

Energy remains tactical. Strait of Hormuz tensions create optionality for Vanguard Energy (VDE), but oil upside has been limited despite renewed conflict, and the market still appears skeptical that the latest flare-up will become a sustained supply shock. Energy can work as a hedge, but it does not have the same forward-demand clarity as AI power infrastructure.

The conclusion is that AI interest has returned after a one-month pause, but the market is no longer buying AI as a single theme. The more durable opportunity is in the electricity and infrastructure layer beneath AI. That keeps Vanguard Information Technology (VGT) in leadership, but it also strengthens the case for Vanguard Industrials (VIS), selective Vanguard Utilities (VPU), infrastructure-linked Vanguard Materials (VAW), and capital-markets-driven Vanguard Financials (VFH).

Chart: market breadth has improved since late May. Energy demand, power generation and financing for the build out are broadening the sector tailwinds from the AI trade.

For sector investors, the key question for the second half is no longer just “who sells the chips?” It is “who supplies the power, builds the facilities, finances the capex, and earns regulated or contractual returns from the load growth?” That is where AI demand is becoming a broader sector rotation story.

Sources

- International Energy Agency, Energy and AI — Used for the data-center electricity-demand exhibit and the view that AI demand is becoming a power/grid/infrastructure theme; the IEA base case projects global data-center electricity consumption doubling to around 945 TWh by 2030.

- Federal Reserve, June 16–17, 2026 FOMC Minutes — Used for the Fed-policy framing around elevated inflation, AI-related investment, Middle East conflict, tariffs, and the possibility that policy firming could be warranted if inflation remains persistent.

- ISM, June 2026 Services PMI — Used for the services-sector backdrop, including resilient activity, employment moving back into expansion, and prices paid easing but remaining elevated.

- New York Fed, June 2026 Survey of Consumer Expectations — Used for the inflation-expectations backdrop, including the rise in one-year inflation expectations to 3.7% and improving household/labor-market perceptions.

Disclaimer: This material is for informational and educational purposes only and should not be considered investment advice, a recommendation, or a solicitation to buy or sell any ETF, security, sector exposure, or investment strategy. Sector performance, earnings expectations, interest rates, inflation trends, and fund flows can change quickly. Past performance is not indicative of future results. Investors should consider objectives, risk tolerance, liquidity needs, and consult a qualified financial professional before making investment decisions.