The next test for the AI trade may not come from Nvidia, memory stocks, or the hyperscalers. It may come from everyone else.

That is the key frame for sector investors this week. The market already believes AI infrastructure demand is real. It sees the order books, the chip demand, the data-center buildout, the power constraints, and the pressure on memory supply. What it still needs to see is whether non-AI companies can turn AI adoption into better margins, better productivity, better revenue growth, and better returns on capital.

In other words, the AI trade now needs validation from outside the AI trade.

The weekend headline package still supports a constructive Growth backdrop. AI demand remains powerful, with Foxconn reporting a 40% year-over-year jump in Q2 revenue on strong AI product demand, ARM highlighting “off the charts” CPU demand from agentic AI, and continued headlines around Meta, Anthropic, Samsung, TSMC, SK Hynix, and custom AI chips. But the same package also shows the risk: Tesla is reportedly limiting employee AI spending because of rising token costs, frontier models face cheaper competition from China, and investors are increasingly worried about excess compute capacity and crowded memory exposure.

That makes the next phase less about whether AI infrastructure gets built and more about whether AI creates enough economic value for the broader corporate sector to justify the buildout.

The Macro Setup Still Favors Growth, but the Bar Is Rising

The macro backdrop remains good enough for Growth leadership, but no longer simple enough to reward every Growth stock equally.

June ISM manufacturing remained in expansion at 53.3, with new orders still healthy at 56.0 and prices paid falling sharply from 82.1 to 73.0. That is a supportive combination for equities: demand is still expanding, input inflation is easing, and the industrial economy is not rolling over.

But the labor data complicates the story. June payrolls rose just 57K, well below expectations, with prior months revised down and labor-force participation falling to 61.5%, its lowest level since March 2021. Consumer confidence remains soft, and the labor-market differential deteriorated to its weakest level since early 2021.

That mix keeps the market tilted toward quality Growth, but it also creates room for Value to matter again. If growth becomes scarcer, investors will keep paying for companies with clear earnings momentum. If rates stay elevated and labor softens, investors will also want cash flow, dividends, balance-sheet strength, and lower valuation risk.

So the sector question is not simply Growth versus Value. It is whether AI can broaden from a capital spending boom into a productivity cycle. If it can, Growth remains the leadership factor. If it cannot, the market may rotate toward Value, defensives, and cyclical sectors with more tangible earnings support.

What Non-AI Companies Need to Show

The market does not need every company to become an AI company. It does need non-AI companies to show that AI is moving through the income statement in measurable ways.

The first thing investors need to see is cost savings. If AI tools are truly improving productivity, companies outside of technology should begin showing slower headcount growth, better operating leverage, shorter service times, lower customer-support costs, faster software development, improved logistics, and higher revenue per employee. The market will be watching margin commentary from retailers, banks, insurers, industrials, healthcare services, and consumer platforms for evidence that AI is reducing expense growth rather than simply adding another technology budget line.

The second thing investors need to see is revenue lift. Cost savings alone would help justify AI adoption, but revenue growth would validate the larger investment cycle. Non-AI companies need to show that AI is improving conversion rates, personalization, fraud detection, pricing, demand forecasting, customer retention, product design, drug discovery, underwriting, or advertising yield. That is how AI moves from a tool into a growth driver.

The third thing investors need to see is capex discipline. The market is already nervous about whether compute supply could outrun demand. Meta’s potential cloud infrastructure push was initially interpreted as a monetization opportunity, but it also triggered excess-capacity concerns and a sharp selloff in the AI trade, with the SOX down nearly 6.5% during the week.

That means investors will reward companies that can explain why AI spending is necessary, what return it should generate, and when those returns should show up. Vague AI spending plans will not be enough.

The fourth thing investors need to see is model-cost control. Tesla’s reported limits on employee AI spending matter because they point to a broader issue: AI usage is expensive. If companies are going to scale AI across workflows, they need to show they can match the right model to the right task, use cheaper models where appropriate, and prevent inference costs from eating the productivity gains. The weekend package also noted growing discussion that Chinese models are closing the frontier-model gap at lower cost, which could pressure expensive AI services while improving adoption economics for users.

The fifth thing investors need to see is better earnings breadth. If AI remains concentrated in semiconductors, memory, and hyperscaler capex, the trade can still work, but it becomes increasingly crowded and fragile. If AI benefits begin showing up in Financials, Industrials, Healthcare, Consumer Discretionary, Communication Services, and even Staples, the market can treat AI as a productivity cycle rather than a narrow infrastructure bubble.

What Would Keep Momentum Behind the AI Trade?

Momentum behind AI remains durable if earnings season confirms that the theme is moving from capex intensity to economic return.

For the infrastructure providers, that means continued order strength, higher backlog, pricing power in memory and advanced chips, demand for CPUs and custom silicon, and positive commentary from suppliers tied to data centers, optical connectivity, electrical equipment, and grid infrastructure.

For the hyperscalers, it means clearer monetization. Meta’s reported cloud-infrastructure plans matter because they give investors a possible bridge from AI spending to AI revenue. If large platforms can show that AI improves advertising, cloud consumption, model access, enterprise tools, and user engagement, investors will remain more tolerant of elevated capex.

For the rest of the market, it means operating leverage. The next bullish leg would come from companies saying something like this: “AI is helping us do more with less, serve customers faster, price better, sell more efficiently, or reduce labor intensity.”

That is the evidence that would validate the AI trade beyond semiconductors.

In that scenario, the sector leadership map could broaden. Information Technology would remain the core Growth exposure, but Communication Services could benefit from AI monetization, Industrials from automation and electrification, Financials from underwriting and productivity gains, Healthcare from workflow and discovery tools, and Consumer Discretionary from better personalization and inventory management.

That would be the healthiest version of the AI bull market: not just bigger data centers, but better businesses.

What Would Spur Rotation Away From AI?

The most likely catalyst for rotation away from AI would be evidence that the infrastructure buildout is running ahead of customer economics.

The first warning sign would be more excess-capacity headlines. If investors begin to believe that hyperscalers, neoclouds, and AI infrastructure companies are overbuilding compute before demand is mature enough, the market will question margins across the stack. That would hit semiconductors, AI servers, networking, power equipment, and speculative data-center beneficiaries.

The second warning sign would be AI as cost burden rather than productivity tool. If non-AI companies talk about rising AI expenses without corresponding margin benefit, the market will begin to ask whether AI adoption helps users or mostly enriches infrastructure suppliers. Tesla’s token-cost discipline headline is an early example of the question investors will keep asking: is AI usage scaling profitably?

The third warning sign would be cheaper model disruption. Lower-cost Chinese models and more efficient open models are bullish for adoption, but they can be bearish for companies monetizing expensive frontier models. If AI becomes cheaper faster than expected, some infrastructure demand may remain strong, but pricing power in parts of the software and model layer could come under pressure.

The fourth warning sign would be higher rates. Rates moved higher this week despite lower oil and softer payrolls, and that matters. A sticky-rate backdrop reduces the market’s willingness to underwrite long-duration Growth stories. If yields remain firm while labor data weakens, investors may rotate toward Value, dividends, Financials, select Industrials, and defensive cash-flow sectors.

The fifth warning sign would be earnings concentration. Q2 earnings are expected to show strong growth, with AI infrastructure playing an outsized role in S&P 500 earnings momentum. That is bullish if the numbers keep improving. It is a risk if investors decide too much of the market’s profit growth depends on one theme.

Sector Implications

The best sector stance remains pro-Growth, but not indiscriminately pro-Growth.

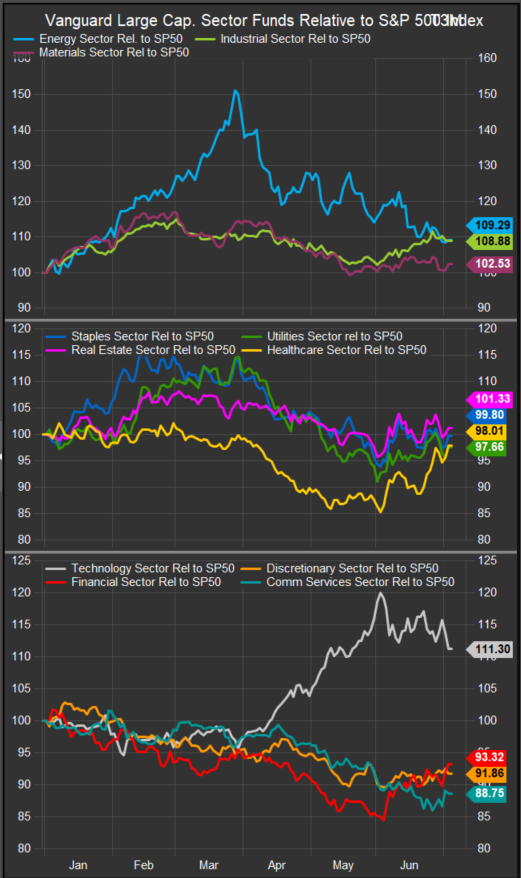

Information Technology remains the center of the AI trade, but leadership needs to stay tied to companies with pricing power, order visibility, and clear exposure to AI bottlenecks. Semiconductors, memory, custom silicon, CPUs, AI servers, optical connectivity, and infrastructure software remain better positioned than speculative software with unclear AI monetization.

Communication Services becomes more important if AI monetization improves. Meta’s cloud and AI infrastructure narrative could help the sector if investors see a revenue path rather than only a spending cycle.

Industrials remain one of the cleanest ways to own AI outside traditional Technology. Electrification, grid equipment, automation, aerospace, defense, drones, and data-center infrastructure all benefit if AI spending continues moving into the physical economy.

Financials could become a key validation sector. If banks, insurers, payment networks, and exchanges show AI-driven productivity, fraud reduction, underwriting improvement, or customer-service efficiency, that would support the idea that AI is spreading into mainstream corporate profitability.

Healthcare is another important test. Investors need to see whether AI can reduce administrative complexity, speed discovery, improve diagnostics, or help providers manage labor constraints. Without that evidence, the sector remains more defensive than AI-leveraged.

Consumer Discretionary needs proof that AI can drive conversion, personalization, logistics efficiency, or inventory improvement. Without labor strength, the sector is vulnerable to softer consumer confidence.

Energy is less compelling as a broad sector call despite geopolitical risk, given falling oil prices, OPEC+ output increases, high inventories, and supply-glut concerns.

Utilities are split between traditional rate-sensitive defensives and the more attractive power-demand beneficiaries tied to data centers, electrification, and grid investment.

Bottom Line

The AI trade is no longer just waiting for more AI headlines. It is waiting for proof from non-AI companies.

If Q2 earnings show that AI is helping companies outside Technology cut costs, grow revenue, improve productivity, and defend margins, the Growth trade can broaden and the AI cycle will look more like a durable productivity boom. If earnings show rising AI costs without visible returns, the market may begin rotating toward Value, dividends, defensives, and lower-multiple cyclicals.

That is the sector investor’s test for the second half: not whether AI infrastructure demand is real, but whether the rest of the market can turn that infrastructure into better business economics.

Sources

- Charts sourced from FactSet Research Systems Inc.

- TechCrunch — Anthropic’s early-stage work on its own AI chip and reported Samsung discussions.

- The Information — Tesla limits on employee AI spending amid rising token costs.

- Reuters — Anthropic/White House equity-stake clarification; Uber Europe expansion update; JPMorgan gold forecast; Iran leadership coverage; Russia oil-terminal drone attack; Qatar maritime activity resumption.

- Yahoo Finance — Meta considering Samsung over TSMC for next-generation AI chips.

- Bloomberg — SK Hynix AI valuation/listing story; Indian equities regaining favor as a shelter from AI volatility; Iran/China Strait of Hormuz service-fee concessions; oil-glut concerns; Total CEO comments on excess crude inventories.

- U.S. News — Foxconn Q2 revenue growth tied to strong AI product demand.

- CNBC — Kalshi/Polymarket volume surge; Red Sea vessel attack; OPEC+ August output-target increase.

- Financial Times — Uber Europe expansion pause; Ukraine strikes on Russian energy assets.

- Washington Post — Iran’s new hardline regime structure.

- Axios — Trump administration skepticism toward the Netanyahu relationship.

- New York Times — China pressure on Taiwan via expanded coast-guard patrols; retail losses in Trump-branded crypto coins.

- Goldman Sachs — Hedge-fund gross and net exposure positioning referenced in the market talking points.

- JPMorgan / Citi sell-side commentary — Labor-market interpretation, Fed-policy implications, earnings setup, and gold/rate-risk framing.

- ISM Manufacturing — June manufacturing index, new orders, production, employment, prices paid, and respondent commentary.

- S&P Global PMI — Final June manufacturing PMI, output, new orders, pricing, and employment commentary.

- ADP — June private payrolls and wage-growth data.

- BLS / Nonfarm Payrolls — June payroll gain, revisions, unemployment rate, labor-force participation, and wage data.

- BLS / JOLTS — May job openings, hiring, quits, separations, layoffs, and labor-market indicators.

- Conference Board — June consumer confidence, Present Situation Index, Expectations Index, and labor-market differential.

- Chicago PMI — June Chicago PMI, new orders, production, backlogs, employment, and prices-paid detail.

- Dallas Fed Manufacturing Survey — June Dallas Fed index, production, new orders, employment, prices, and future activity expectations.

- U.S. Supreme Court / Trump v. Cook — Fed Governor Cook ruling and central-bank-independence implications.

Disclaimer: This material is for informational and educational purposes only and should not be considered investment advice, a recommendation, or an offer to buy or sell any security, ETF, sector exposure, or investment product. Market conditions, sector leadership, fund flows, earnings expectations, interest rates, and macroeconomic data can change quickly. References to specific sectors, companies, or themes are illustrative only. Past performance is not indicative of future results. Investors should conduct their own research and consult a qualified financial professional before making investment decisions.