The latest weekend news flow leaves sector investors with a market that is strong on the surface but still narrow underneath. The bullish case is clear: earnings have been better than feared, large-cap inflows remain supportive, retail participation is rising, Nvidia has again become an index-level driver, Cisco’s AI order guidance broadened the infrastructure story, and Cerebras’ IPO showed that public-market appetite for AI compute remains deep. Reuters also reported that Cisco now expects roughly $9 billion of AI infrastructure orders in fiscal 2026, underscoring that AI demand is spreading from chips into networking and data-center architecture.

But the bearish counterpoint is equally important: breadth remains weak, semiconductor positioning is stretched, Treasury yields have broken higher, oil and freight costs are pressuring inflation, and consumer-facing sectors are beginning to show stress. That does not mean the bull market is over. It means investors still need evidence that the rally can move from AI exceptionalism to earnings breadth.

The Core Question: Can AI Become a Broad Market Multiplier?

The market is currently pricing AI as both a growth theme and a macro offset. The bull case is that AI capex keeps earnings momentum alive even as rates stay higher and energy prices pressure consumers. Nvidia’s recent market-cap surge, Cisco’s networking strength, and the Cerebras IPO all support the view that AI infrastructure demand remains real, visible, and supply constrained. Cerebras raised $5.55 billion in its IPO, with Reuters describing the offering as the largest IPO of 2026 and highlighting heavy demand for AI chip exposure.

However, sector investors should distinguish between AI beneficiaries and AI beneficiaries broad enough to validate a bull market. A contained AI boom can lift semiconductors, networking, electrical equipment, data-center power, and select software. A broad bull market requires AI demand to spill into productivity, margins, capital spending, and earnings revisions across more of the index.

Investors should look for four confirmations:

First, earnings breadth must improve. The rally becomes more credible if forward earnings revisions turn positive not just for semiconductors and mega-cap platforms, but also for Industrials, Financials, Materials, Utilities, and select Consumer companies.

Second, equal-weight and small/mid-cap participation must strengthen. If the S&P 500 rises while market breadth deteriorates, the message is concentration, not broad risk appetite.

Third, AI capex must translate into revenue for suppliers beyond Nvidia. Cisco is a good example because its results suggest networking demand is becoming part of the AI infrastructure stack, not an afterthought.

Fourth, AI must stop being funded purely by valuation expansion. A sustainable bull market needs operating leverage, cash-flow growth, and visible returns on investment. If the market starts to believe that AI spending is rising faster than monetization, the leadership group can remain profitable but derate.

Inflation Risk Is Rising, Not Falling

Inflation risk has clearly moved higher. The debate is no longer whether inflation is easing fast enough; it is whether the energy shock is becoming embedded in transportation, food, freight, and services prices.

The April CPI report showed headline CPI up 0.6% month over month and 3.8% year over year, while core CPI rose 0.4% month over month and 2.8% year over year. Energy was up 17.9% year over year, and food was up 3.2%. The PPI data were even more concerning for margins: final demand prices rose 1.4% in April, with final demand goods up 2.0% and final demand services up 1.2%. BLS said over 40% of the goods increase came from a 15.6% jump in gasoline, while jet fuel, diesel fuel, vegetables, industrial chemicals, and residual fuels also rose.

That is a problem for sector allocation because it shifts the inflation narrative from “sticky but easing” to “energy-led and broadening.” The EIA’s May outlook assumes the Strait of Hormuz remains effectively closed until late May, with shipping only beginning to pick up in June, and estimates that Gulf producers shut in roughly 10.5 million barrels per day of crude production in April. The IEA similarly reported that global oil supply fell another 1.8 million barrels per day in April, bringing cumulative losses since February to 12.8 million barrels per day.

The implication is straightforward: inflation risk is rising because the shock is hitting both consumer prices and corporate input costs. It is also complicating Fed policy. Reuters reported that the 10-year Treasury yield rose to around 4.60% and the 30-year yield to roughly 5.13% on May 15 as oil, inflation, and rate concerns pressured bonds.

What Would Make the Bull Market More Believable?

A broad bull market requires evidence that the economy can absorb higher rates and higher energy costs without forcing earnings downgrades. Retail sales offered some support: Census data showed April retail and food services sales rose 0.5% from March and 5.2% from a year earlier, with nonstore retailers up 11.1% year over year. That argues against an immediate consumer break.

But the details matter. The weekend headlines pointed to higher gasoline, grocery inflation, negative real wage pressure, and underperformance in retail and consumer-facing pockets of the market. For a broader bull market to become credible, investors need to see consumer resilience in real terms, not just nominal sales boosted by higher gas and food prices.

The most important confirmations would be: lower oil volatility, stabilizing long-term yields, broader earnings revisions, continued capex strength outside mega-cap Tech, and improving market breadth. Without those, the market can still rise, but it remains more of a concentrated AI-and-energy-security trade than a durable broad-cycle advance.

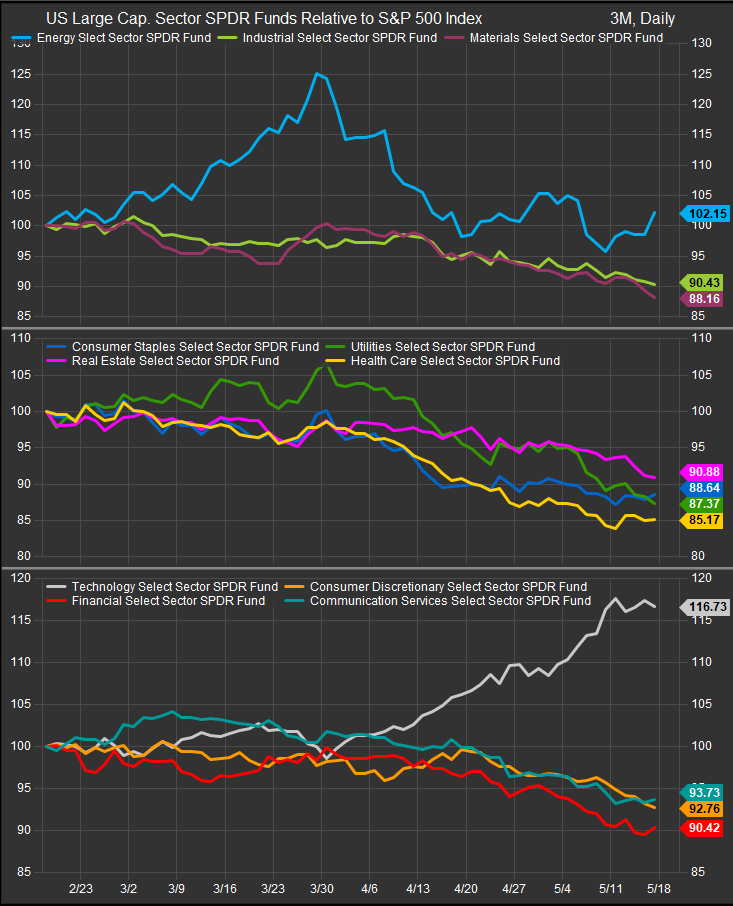

Sector Positioning: Favor Scarcity, Pricing Power, and AI Adjacency

The sector strategy should lean into groups with direct earnings support from the current news flow while reducing exposure to sectors absorbing the inflation shock.

Technology remains an overweight, but the preference should be for AI infrastructure rather than all growth. Semiconductors, networking, data-center hardware, memory, power-management chips, cooling, and infrastructure software remain the cleanest beneficiaries. Cisco’s order strength shows that AI demand is broadening into the networking layer, while Cerebras’ IPO shows that capital markets still want new AI compute exposure. The risk is positioning. When semiconductor sentiment becomes extreme, investors should own the theme but avoid treating every AI-linked stock as equally attractive.

Industrials should remain a favored sector because AI, defense, electrification, and energy security are all capital-spending stories. Electrical equipment, grid services, data-center construction, power systems, defense primes, aerospace suppliers, and engineering firms are better positioned than traditional cyclical Industrials. This is where the AI boom can become a broader sector multiplier.

Utilities are no longer just a bond proxy. The sector faces pressure from higher Treasury yields, but power demand from data centers and grid reliability needs create a differentiated upside case. Investors should favor utilities and power infrastructure companies with visible load growth, constructive regulation, and data-center exposure rather than generic defensive yield exposure.

Energy remains a tactical overweight. The sector benefits directly from constrained supply, geopolitical risk premia, higher crude prices, and energy-security spending. The risk is that any credible Hormuz reopening could compress the geopolitical premium quickly. Still, as long as the supply shock persists, Energy has one of the clearest positive earnings revisions paths.

Materials should be selective. Copper, metals, mining, and infrastructure-linked materials can benefit from electrification, AI power demand, and supply constraints. But chemicals, packaging, and margin-sensitive materials companies face input-cost pressure from energy, freight, and industrial inflation.

Consumer Discretionary should be underweight. Higher gasoline prices, negative real wage pressure, higher financing costs, and freight inflation are a difficult combination for autos, restaurants, travel, lodging, and lower-income retail. The April retail sales report shows consumers are still spending, but the sector risk is that nominal growth masks deteriorating affordability.

Real Estate remains vulnerable except for data-center-linked exposure. Higher long yields pressure cap rates, refinancing, and dividend-sensitive REIT valuations. Data-center REITs and infrastructure-linked real estate are exceptions, but traditional rate-sensitive REIT exposure remains difficult in a rising-yield tape.

Bottom Line

The market is not yet sending a clean broad-bull signal. It is sending a strong signal that investors still believe in AI infrastructure, energy security, defense spending, and strategic scarcity. That is enough to support leadership in Technology, Industrials, Utilities infrastructure, Energy, and select Materials. It is not yet enough to validate a broad bull market across consumer, real estate, small caps, and rate-sensitive cyclicals.

Inflation risk is rising, not falling, because the energy shock is now visible in CPI, PPI, freight, fuel, food, and bond yields. Until oil stabilizes and breadth improves, sector investors should stay selective: overweight AI enablers, power infrastructure, defense, and Energy; remain cautious on Consumer Discretionary, traditional Real Estate, and companies without pricing power.

Sources:

- StreetAccount weekend financial headlines and market commentary provided by the user

- Reuters

- Bloomberg

- CNBC

- Axios

- Financial Times

- Associated Press

- U.S. Bureau of Labor Statistics — CPI and PPI reports

- U.S. Census Bureau — April retail sales report

- U.S. Energy Information Administration — Short-Term Energy Outlook

- International Energy Agency — May Oil Market Report

- Federal Reserve / FOMC commentary

Disclaimer

This commentary is provided for informational and educational purposes only and does not constitute investment advice, a recommendation, or an offer to buy or sell any security, sector, ETF, or investment product. Views are based on current market conditions, news flow, and third-party data that may change without notice. Sector positioning opinions are not tailored to any individual investor’s objectives, risk tolerance, or financial situation. Investors should conduct their own research and consult a qualified financial professional before making investment decisions. Past performance is not indicative of future results