The key point from last week is that the market did not behave the way it normally does when the macro data come in strong. The inputs were bullish. The price action was not. Friday’s selloff—Nasdaq -4.18%, S&P 500 -2.64%, Russell 2000 -3.47%, SOX down more than 10%—tells investors that the market is no longer rewarding good news in the most crowded parts of the tape. That distinction matters. The week featured a run of data that, in a healthier market, should have supported a continuation rally. The May payroll report came in at 172K versus 86K expected, unemployment held at 4.3%, and wage growth cooled to 0.3% m/m, which would ordinarily be read as “strong enough for growth, not so hot that it forces immediate Fed tightening.” ISM manufacturing and services both beat expectations, new orders improved, and the Citi U.S. Economic Surprise Index reached its highest level since October 2023. Fund flows were supportive too, with BofA highlighting a tenth straight week of inflows into U.S. equity funds. On top of that, the week’s bullish note underscored continued AI infrastructure demand through strong commentary from Hewlett Packard Enterprise, Dell, Broadcom, TSMC, and ASML. In short, the setup was constructive.

Chart (Above): S&P 500 has near-term support at the 7333 level. Corrections contained by the February price high at 7002 conform to the long-term uptrend pattern. 6618 is where the price structure is flipping to a bearish message.

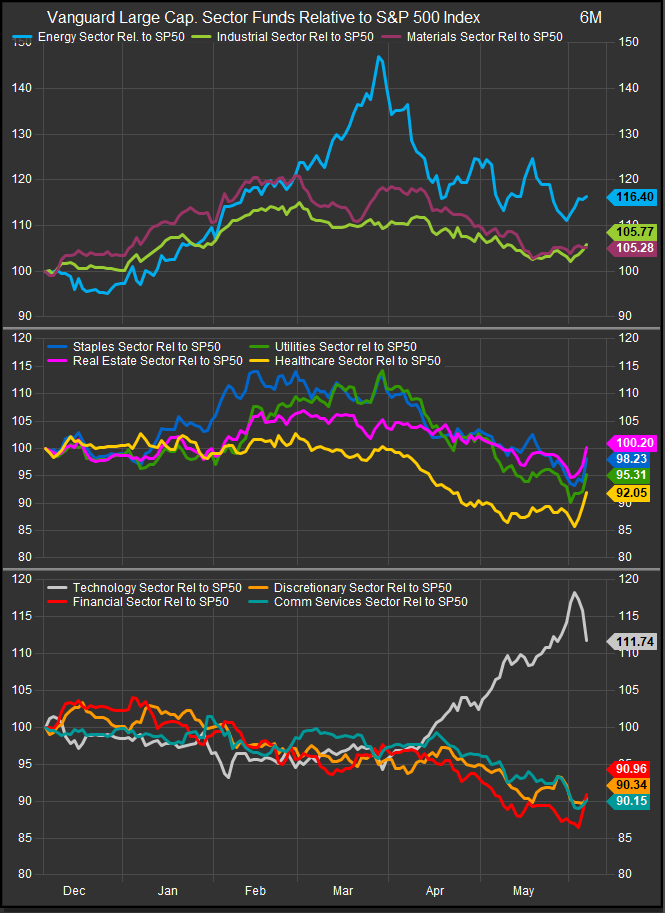

NOTE: For this discussion, we’re using the Vanguard U.S. sector ETFs as sector proxies. Ultimately, we think Tech shares will regain leadership if the business cycle continues to expand. While Friday’s Tech sell-off was sharp, the test of the outperformance trend is ahead of us. If Investors shrug at an oversold accumulation opportunity, that will be a bearish “tell”.

But the market did not finish the week like a market embracing that setup. Instead, it sold off hardest exactly where leadership had been most crowded: semiconductors, networking, hardware, and software. That is the first and most important conclusion. Investors are starting to question whether the strongest macro backdrop still deserves the same valuation premium in Technology and AI that it received over the past year. The week’s bearish note gave several reasons why. Broadcom’s results and guidance underwhelmed against a very high bar, with softer near-term AI semiconductor guidance, no lift to FY27 expectations, and lingering concern about customer diversification and Google TPU competition. Goldman Sachs also noted that the cumulative outperformance of S&P 500 momentum versus low volatility is now approaching Tech Bubble-era extremes. In other words, the market is no longer just evaluating AI on fundamentals; it is evaluating it as a crowded positioning and valuation risk.

That creates a more difficult setup for VGT and, to a lesser extent, VOX. The bullish anchor for those sectors remains clear. FactSet still expects Technology to post around 45% earnings growth in Q1, with semiconductors at roughly 95%, and the sector remains the dominant contributor to index-level earnings expansion. (advantage.factset.com) As long as AI capex remains strong, Technology has the best structural growth in the market. But what Friday showed is that this may no longer be enough by itself. For the selloff to turn into a more sustained rotation away from the AI trade, investors would need to see more than one disappointing guide. They would need evidence that the returns on AI spending are being pushed further out, that customers are becoming more price sensitive on token costs, that open-model competition is eroding pricing power, or that capital intensity is forcing companies into weaker financing decisions. The late-week discussion around Google’s equity raise, the potential SpaceX IPO as a source-of-funds event, and scrutiny of OpenAI’s token economics all point in that direction.

The second issue is rates. One reason the market reacted so negatively to otherwise solid growth data is that the Treasury market interpreted the same information as a reason to price fewer cuts and potentially more tightening. The bearish summary noted the 10-year yield back above 4.50% and the 30-year above 5%, with two Fed officials openly discussing the possibility of hikes later this year. That is exactly the kind of move that undermines long-duration Growth. It is also one of the clearest inflationary signals in the week’s news flow. The same note pointed to oil-market executives warning the White House that low inventories could send prices much higher, ISM prices-paid remaining elevated, and the Beige Book describing energy-related costs as the primary driver of broader pricing pressure. Add in tariffs, shipping costs, packaging, groceries, and fertilizer, and you have the outline of an inflationary environment that is no longer confined to just oil.

The question investors should ask is whether those inflationary trends are enough to tip the economy into recession. So far, the answer still looks like no. There are some caution flags. Initial claims rose to their highest level in four months. Challenger layoffs moved up to 97K, with Technology layoffs around 38K, and AI now cited as the reason for 40% of announced cuts in May, versus 7% in January. Productivity slowed sharply in Q1. The Beige Book described a bifurcated consumer, with lower-income households increasingly squeezed, while small businesses reported softer conditions and weaker capital-spending intentions. Those are not signs of a booming economy. But they are not yet signs of recession either. Claims remain low by historical standards, continuing claims are still stable, JOLTS openings surprised to the upside, and both ISM reports remain in expansion territory. The economy looks late-cycle, cost-pressured, and narrower—but not yet broken.

That matters for sector allocation. If the economy is not rolling over, but inflation and yields are becoming a bigger problem, the sectors likely to hold up best are the ones with a mix of pricing power, near-term cash flow, and less valuation sensitivity. That leaves VIS and VAW in a better tactical position than VGT in the very near term, even though Technology still has the stronger long-run earnings story. The industrials newsflow was quietly constructive: Fastenal’s demand improved, freight commentary was better than seasonal, and tariff relief supported machinery and HVAC. Materials still have strong earnings-growth expectations and benefit from an inflationary nominal backdrop. VDE remains useful as a hedge if oil risk re-accelerates, though it is more of a macro insurance position than the cleanest leadership trade.

Interest rates (above) are hooking higher in the near-term. That could exacerbate concerns over the longer-term credit cycle for the AI infrastructure build out.

So far, no signs that investors are stocking up on commodities in the near-term. 130 is a key support level.

By contrast, the weakest sectors still appear to be VHT, VFH, and the Consumer group (VCR and VDC). Health Care lacks the earnings acceleration and narrative support to attract capital in a tape dominated by AI and rates. Financials are stuck between higher rates that should help and private-credit concerns that still keep investors cautious. Consumer-facing sectors are the most exposed to exactly the combination the Beige Book described: rising prices, heavier credit-card usage, softer visits, and more evident stress among middle- and lower-income cohorts. Those sectors are where inflation and slowing demand can meet most painfully.

So what should investors take from all this? The market’s message is that strong macro data are no longer enough to keep the AI trade levitating on their own. If the market wanted to rally on good news, last week gave it plenty of reasons. Instead, it used that good news to push yields higher and question whether crowded Growth leadership still deserves the same premium. That does not mean the AI trade is over. It means the burden of proof is higher. Technology still has the best structural earnings. But for momentum in VGT and related AI exposures to remain bullish, investors now need more than capex strength—they need evidence that spending is monetizing efficiently, that rate pressure is stabilizing, and that token-cost and open-model concerns are not eroding the economics.

Until that happens, the next phase of the market is likely to be less about “buy all Growth” and more about whether leadership broadens into sectors like VIS and VAW—or whether the market’s late-week rejection of bullish inputs was the first signal that the AI trade is becoming harder to own at current valuations. From our view, bullish synergies with other sectors are an important next step for the AI trade to prove its merits. The near-term earnings advantages are clear for AI exposed companies, but the pool of beneficiaries needs to broaden in order for the trade to continue as the core of a strong business cycle.

Sources

- FactSet Research Systems / StreetAccount — Weekly bullish and bearish talking points, macro event recaps, sector-level narrative, and the June 6 U.S. market recap used throughout the analysis.

- FactSet Research Systems, Earnings Insight (June 2026) — S&P 500 and sector earnings-growth expectations, including Technology, semiconductors, Materials, and Financials.

- Vanguard — Sector ETF profiles used as proxies for U.S. sector performance: Technology (VGT), Industrials (VIS), Energy (VDE), Materials (VAW), Financials (VFH), Consumer Discretionary (VCR), Consumer Staples (VDC), Health Care (VHT), Utilities (VPU), Communication Services (VOX), and Real Estate (VNQ).

- MSCI Research — Factor and momentum research used to frame the persistence and reversal risks in concentrated leadership trades.

- AQR Capital Management — Institutional research on momentum crowding and reversal dynamics.

- Reuters — Reporting on oil-market developments, yield moves, and macro risk transmission relevant to energy, inflation, and equity positioning.

Disclaimer

This material is provided for informational and editorial purposes only and does not constitute investment advice, a recommendation, or an offer to buy or sell any security. Views expressed are based on information believed to be reliable as of the publication date, but accuracy and completeness are not guaranteed. Market conditions can change quickly, and past performance is not indicative of future results. Investors should consider their own objectives, risk tolerance, and financial circumstances before making investment decisions.