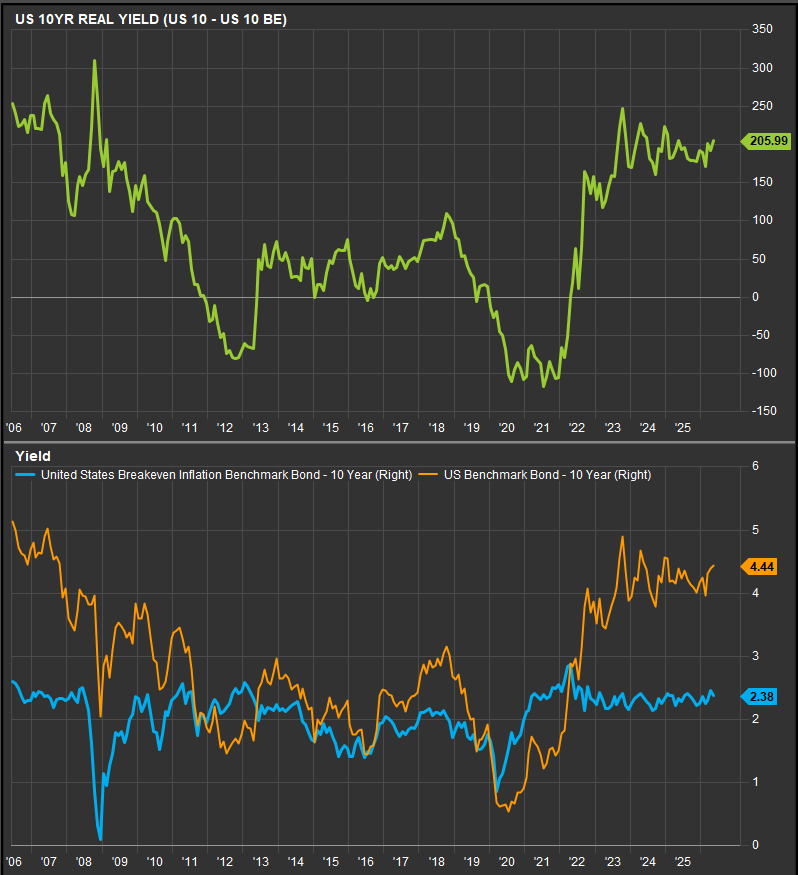

Exhibit 1. US 10-Year Yield, Breakeven Inflation and Real-Yield Proxy

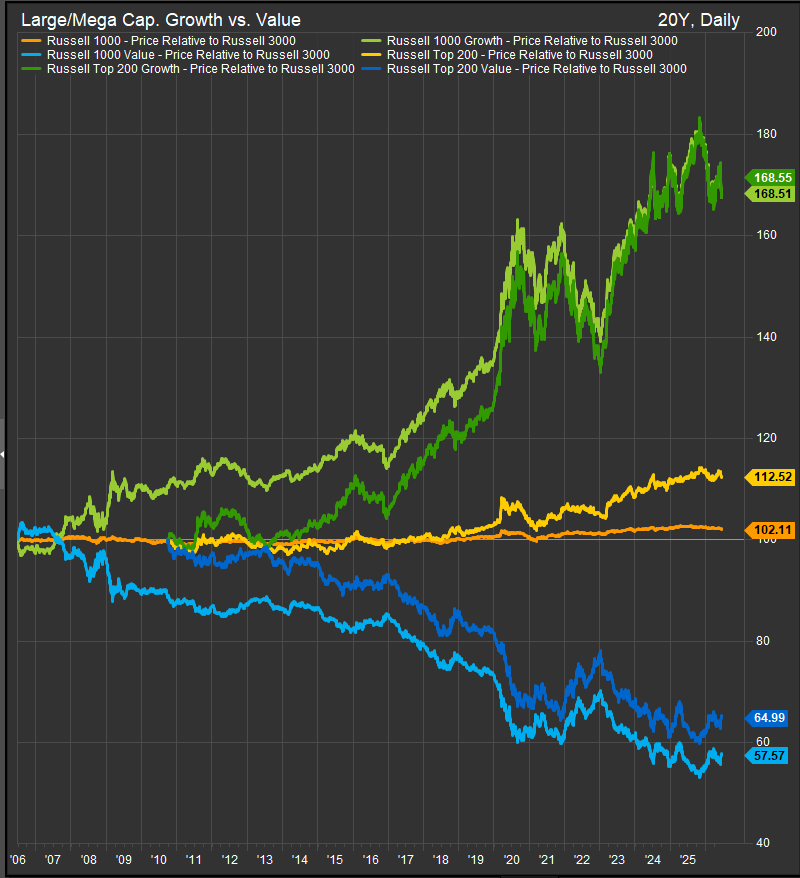

Exhibit 2. Large/Mega-Cap Growth vs. Value Relative Performance

The long-term relationship between rates and equity style remains intact: higher real yields raise the valuation hurdle for Growth, while higher nominal yields can support Value when they reflect stronger nominal GDP, inflation, and credit creation. The problem for broad Value is that the current rate backdrop is not simply a reflation trade. The 10-year Treasury yield is near 4.4%, breakeven inflation is near 2.4%, and the implied 10-year real-yield proxy is around 2.1%. That is a restrictive real-rate environment, not just an inflationary one.

That distinction explains why Growth has not broken down despite higher rates. The Russell 1000 Growth universe is heavily concentrated in Information Technology, Consumer Discretionary, and Communication Services. In ETF terms, iShares Russell 1000 Growth (IWF) is effectively a mega-cap technology and platform exposure, with Information Technology near half of assets and top holdings including NVIDIA (NVDA), Apple (AAPL), Microsoft (MSFT), Broadcom (AVGO), Amazon (AMZN), Alphabet (GOOGL), Meta Platforms (META), Tesla (TSLA), and Eli Lilly (LLY). That concentration has helped Growth because the earnings story is not just “lower rates.” It is AI compute, cloud capex, memory pricing, digital platforms, and balance-sheet strength.

By contrast, iShares Russell 1000 Value (IWD) is more diversified across Financials, Industrials, Health Care, Information Technology, Communication Services, Energy, Staples, and Discretionary. That makes Value less exposed to a single earnings engine, but also less directly tied to the AI capex cycle. Value needs broader earnings participation from banks, industrial cyclicals, energy, materials, staples, health care, and defensives. That breadth has not fully arrived.

The current news flow cuts both ways for rates. The US-Iran MOU and roughly 30% decline in WTI and Brent are disinflationary and should pressure breakevens lower. Lower gasoline prices also support the consumer and reduce the odds of an immediate growth scare. However, strong May retail sales, resilient jobless claims, firm regional Fed price data, hotter import/export prices, and a hawkish June FOMC argue against a clean decline in nominal yields. The Fed’s updated projections showed more concern about persistent inflation, and several policymakers now see the possibility of rate hikes in 2026.

The result is a mixed but investable setup: nominal yields may stay firm, breakevens may ease, and real yields may remain high. That favors companies with visible real earnings growth and balance-sheet strength. It does not favor companies that need lower discount rates to justify valuations.

The Growth playbook should therefore be selective. Favor Quality Growth, not broad Growth. The better exposures are profitable AI and cloud leaders such as NVIDIA (NVDA), Broadcom (AVGO), Microsoft (MSFT), Amazon (AMZN), Alphabet (GOOGL), Meta Platforms (META), and Oracle (ORCL); memory/storage beneficiaries such as Micron (MU), Western Digital (WDC), and Seagate (STX); and AI infrastructure enablers such as Vertiv (VRT), Eaton (ETN), Quanta Services (PWR), GE Vernova (GEV), Constellation Energy (CEG), and Vistra (VST). ETF expressions include iShares Russell 1000 Growth (IWF), Vanguard Growth (VUG), Vanguard Information Technology (VGT), VanEck Semiconductor (SMH), and Global X Data Center & Digital Infrastructure (DTCR).

Avoid broad Growth where the business still depends on future monetization, falling rates, or multiple expansion. That includes unprofitable software, speculative AI applications, weak-margin EV names, long-duration consumer internet laggards, and concept stocks that are not yet converting AI enthusiasm into earnings revisions or free cash flow.

Value also needs to be selective. Favor Value with earnings support, not broad low-multiple exposure. Large-cap financials such as JPMorgan (JPM), Goldman Sachs (GS), Morgan Stanley (MS), Bank of America (BAC), and Wells Fargo (WFC) can benefit from firm nominal growth, capital-markets activity, and higher-for-longer rates. Insurers such as Chubb (CB), Progressive (PGR), and Aflac (AFL) remain cleaner high-rate beneficiaries than many regional banks.

Industrials are the most attractive bridge between Growth and Value. Machinery, electrical equipment, automation, defense, grid, and construction-infrastructure stocks can benefit from AI capex, reshoring, defense spending, and power demand. Examples include Caterpillar (CAT), Eaton (ETN), Emerson Electric (EMR), Parker-Hannifin (PH), Quanta Services (PWR), GE Aerospace (GE), GE Vernova (GEV), and RTX (RTX). ETF expressions include Vanguard Industrials (VIS), and iShares U.S. Infrastructure (IFRA).

Be more cautious on broad Value. Energy loses some leadership appeal when oil is falling. Regional banks remain exposed to credit, funding, and commercial-real-estate risk. REITs and housing are still rate-sensitive, even if lower oil supports consumers. Deep cyclicals need proof that earnings revisions are broadening beyond AI and large-cap financials.

The most actionable H2 2026 stance is a barbell: own profitable AI-linked Growth and Growth-adjacent industrial infrastructure, while adding selective Value in large-cap financials, insurers, industrials, infrastructure, and copper/materials. Avoid broad style labels. Broad Growth still contains too many expensive duration assets. Broad Value still contains too many businesses with weak earnings momentum or rate sensitivity.

The key message is simple: higher real yields have not killed Growth because AI earnings momentum has been strong enough to absorb the valuation headwind. But high real yields raise the bar for the next leg. Investors should favor companies that can grow earnings in real terms without needing lower rates. That still points to Quality Growth first, selective Value second, and broad style beta last.

Source notes: The investment update supports the oil, AI demand, retail sales, Fed, inflation, positioning, semiconductor-volatility, and credit-risk setup used in the report. BlackRock’s IWF fact sheet shows Russell 1000 Growth exposure led by Information Technology at 49.53%, Consumer Discretionary at 13.14%, and Communication at 12.10%, with top holdings including NVIDIA, Apple, Microsoft, Broadcom, Amazon, Alphabet, Meta, Tesla, and Eli Lilly. BlackRock’s IWD fact sheet shows Russell 1000 Value led by Financials at 19.93%, Industrials at 13.45%, Health Care at 11.67%, Information Technology at 11.66%, Energy at 7.69%, and Consumer Staples at 7.52%. Reuters reported that the Fed held rates steady in Warsh’s first meeting, while new projections showed nearly half of policymakers expected a rate hike by year-end 2026.

Sources

- FactSet/StreetAccount investment update, week ended June 18, 2026 — Used for the US-Iran MOU/oil selloff, AI demand narrative, May retail sales, Fed takeaways, positioning, semiconductor volatility, import/export prices, regional Fed price data, and credit-risk context.

- iShares Russell 1000 Growth ETF (IWF), BlackRock/iShares — Used for the Russell 1000 Growth sector-composition and top-holdings discussion. IWF’s sector exposure is heavily weighted toward Information Technology, followed by Consumer Discretionary and Communication Services.

- iShares Russell 1000 Value ETF (IWD), BlackRock/iShares — Used for the Russell 1000 Value sector-composition discussion and the more diversified Value profile.

- Reuters / Federal Reserve June 2026 coverage — Used for the hawkish Fed backdrop, including the unchanged policy rate, Warsh’s first meeting, reduced forward guidance, and projections showing roughly half of policymakers expecting at least one 2026 rate hike.

- Federal Reserve Summary of Economic Projections, June 17, 2026 — Used for the official inflation, policy-rate, and macro-projection framework behind the rate outlook.

- Reuters US-Iran / oil-sanctions coverage — Used for the energy-supply and inflation-risk discussion around Iran oil waivers, frozen assets, and the $300B development fund.

Disclaimer

This material is for informational and educational purposes only and should not be considered investment advice, a recommendation, or a solicitation to buy or sell any security, ETF, or strategy. Market conditions, rates, earnings expectations, and fund exposures can change quickly. Past performance is not indicative of future results. Investors should consider objectives, risk tolerance, liquidity needs, and consult a qualified financial professional before making investment decisions.