March 22, 2026

Markets are now being forced to price three competing macro regimes at once: an energy-driven inflation shock, a potential growth slowdown, and a Goldilocks scenario supported by resilient earnings. The past week’s headlines and data reinforce that all three paths are credible—and that sector leadership will hinge on which transmission mechanism dominates.

The most immediate and visible force is inflation, and the catalyst is energy. The Strait of Hormuz remains only partially functional, with Iran allowing selective passage while continuing to target infrastructure. Saudi officials have explicitly warned that oil could exceed $180 per barrel if disruptions extend into late April, while Brent has already traded above $115–$119 during recent escalation. At the same time, LNG markets are tightening rapidly, with reports suggesting a global supply cliff within days as Middle East shipments stall.

These dynamics are no longer theoretical—they are feeding directly into inflation data. February PPI surprised sharply to the upside, with headline +0.7% m/m vs. +0.3% expected and core +0.5%. More importantly, the three-month annualized core PPI is running near 7.8%, the highest since 2022. Energy prices rose more than 2% in the report, but the breadth of the increase—across goods and services—suggests second-order effects are already taking hold.

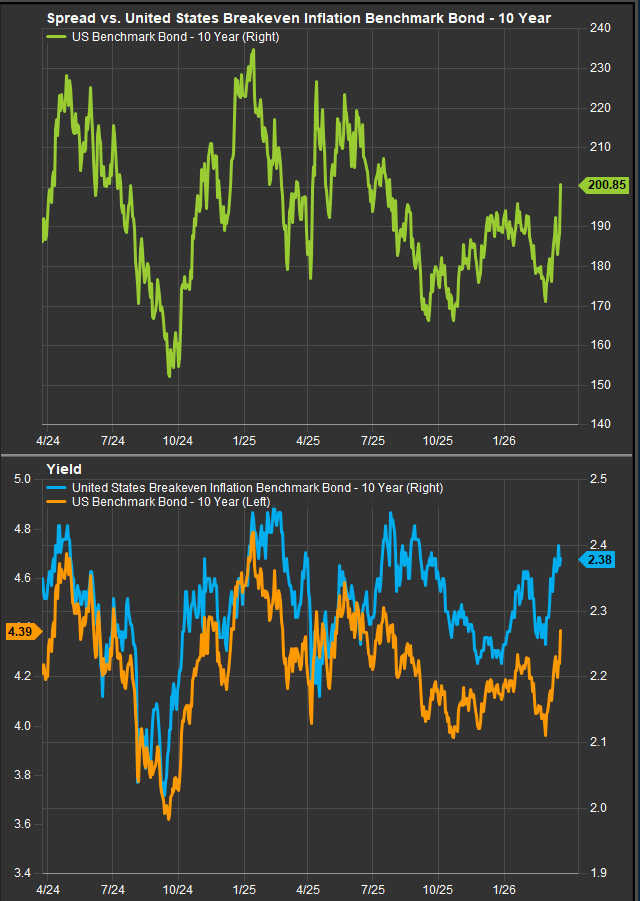

Our research suggests that real rates will be a key swing factor for sector performance. Higher real rates over sustained time periods would likely constrain credit and hinder Growth stocks.

Central banks are reacting accordingly. The Fed’s March meeting leaned hawkish, with Powell emphasizing uncertainty around energy-driven inflation and signaling that rate cuts may be delayed absent clear progress on goods disinflation. Market pricing has shifted dramatically, now reflecting no cuts and even ~17bp of hikes by year-end. In Europe, the ECB and BoE are facing similar pressures, with markets pricing renewed tightening cycles.

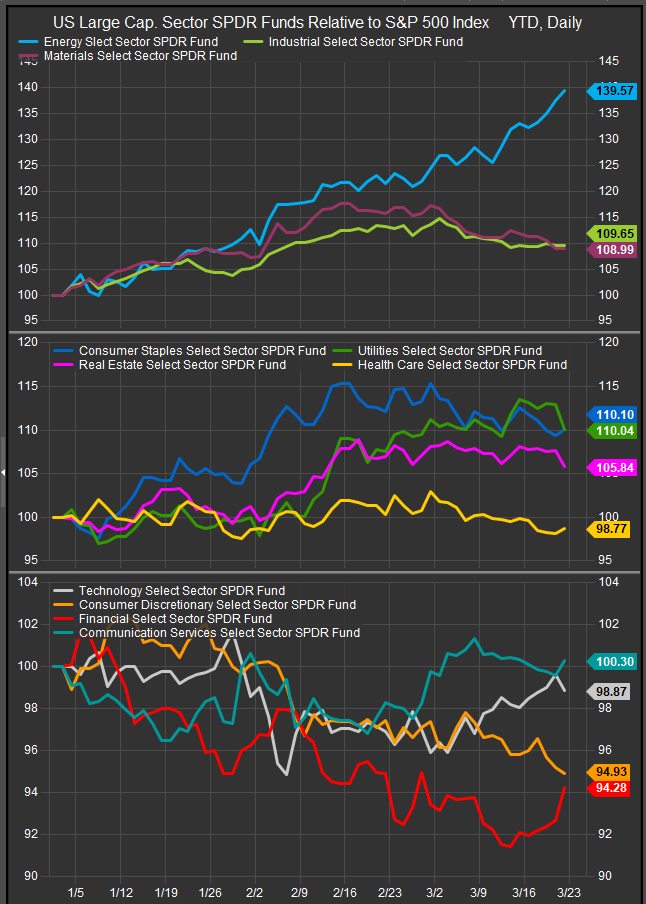

If this inflationary regime persists, sector leadership is straightforward. Energy remains the primary beneficiary, with direct earnings leverage to higher oil and gas prices. Materials follow, supported by rising commodity prices and supply constraints. Financials benefit from higher rates and inflation expectations, particularly if the curve steepens modestly. These dynamics are already visible in earnings expectations, with Materials projected to grow earnings by ~24.6% y/y and Financials by ~11.6%, second only to Technology.

However, inflation is not a clean positive for equities. Higher input costs are beginning to pressure margins across transportation, airlines, and consumer sectors. United Airlines, for example, is now planning for oil to remain above $100 through 2027 and has already cut capacity expectations. Fertilizer and food supply disruptions are also emerging, raising the risk of broader consumer pressure. If sustained, this environment transitions from inflationary to stagflationary.

That transition introduces the second path: recession risk.

There are already early signs of demand softening beneath the surface. January new home sales fell to 587K vs. 720K expected, the lowest level since October 2022. Small business optimism has declined for two consecutive months, and retail participation—historically a key marginal buyer—has fallen sharply, with JPMorgan noting retail flows down 43% since the conflict began. At the same time, capital is rotating defensively, with money market fund assets reaching a record $8 trillion, signaling elevated risk aversion.

Financial conditions are also tightening. Treasury volatility has surged, private credit is back under scrutiny with over $10B in redemption requests, and equity positioning remains elevated despite recent de-risking. If oil remains above ~$105–$110 for a sustained period, it begins to act as a tax on consumers and businesses, raising the risk that inflation translates into demand destruction.

In that environment, sector leadership shifts decisively. Defensive sectors—Utilities, Healthcare, and Consumer Staples—outperform due to earnings stability. Cyclicals, including Industrials and Financials, come under pressure as growth expectations deteriorate. Even Energy, while initially supported by pricing, can face downside if demand begins to weaken materially.

And yet, despite these mounting risks, a third outcome remains firmly in play.

Earnings continue to act as a stabilizing force. FactSet data shows S&P 500 earnings expected to grow ~11.6% in Q1, marking the sixth consecutive quarter of double-digit growth, with revenues growing ~9.4%. Technology remains the clear leader, with ~41.7% earnings growth, driven by sustained AI investment.

Corporate commentary reinforces this strength. Nvidia’s latest disclosures point to over $1 trillion in AI-related bookings through 2027, while Micron reported strong demand and supply tightness tied to AI infrastructure. Even outside of Technology, companies such as FedEx delivered earnings more than 25% above expectations, raising guidance and highlighting stable demand conditions.

This creates a plausible Goldilocks scenario in which energy-driven inflation proves temporary, central banks avoid over-tightening, and earnings growth continues to anchor equity markets. Notably, strategists from Goldman Sachs and Morgan Stanley have not materially reduced year-end S&P targets, citing strong earnings momentum and AI-driven capex as key supports. Morgan Stanley explicitly noted that this cycle differs from prior late-cycle periods because earnings are accelerating rather than decelerating into the shock.

Market internals also support this possibility. The negative correlation between the Mag 7 and the equal-weight S&P suggests that mega-cap leadership could reassert itself, particularly if macro volatility stabilizes. At the same time, contrarian indicators are flashing, with the AAII bull-bear spread below -20%, historically associated with strong forward returns.

The challenge is that all three regimes—inflation, recession, and Goldilocks—are currently coexisting. Inflation is rising, growth is showing signs of strain, and earnings remain strong. This creates a market characterized by factor and sector rotation rather than sustained leadership.

For investors, the implications are clear. Energy and Materials remain essential as inflation hedges, while Technology continues to offer the strongest earnings visibility and structural growth. Financials provide selective upside through rate sensitivity, but cyclicals tied to discretionary demand warrant caution. At the same time, maintaining exposure to defensive sectors is increasingly important as a hedge against a potential growth slowdown.

Ultimately, the key variable remains energy persistence. If oil stabilizes, the market is likely to rotate back toward Growth and earnings-driven leadership. If oil continues to rise and inflation becomes entrenched, Value and defensives will dominate.

The market is not being driven by geopolitics alone—but by how those geopolitical shocks translate into inflation, interest rates, and earnings. That transmission mechanism will determine the next phase of sector leadership.

Sources

- FactSet Research Systems / Earnings Insight – S&P 500 earnings (+11.6%), sector growth (Technology +41.7%, Materials +24.6%, Financials +11.6%)

- StreetAccount / FactSet Macro Summaries – Iran conflict developments, energy disruptions, sector performance trends

- Reuters – Oil price forecasts, Strait of Hormuz disruptions, central bank policy expectations

- Bloomberg – LNG supply risks, Treasury volatility, private credit stress, energy infrastructure attacks

- Financial Times – LNG market disruption, retail/private credit outflows, geopolitical strategy analysis

- Federal Reserve (FOMC, Powell commentary) – Policy outlook, inflation risks, rate path uncertainty

- JPMorgan, Goldman Sachs, Morgan Stanley Research – Positioning, earnings resilience, macro scenario analysis