March 15, 2026

The weekend headlines reinforce that markets are operating in a geopolitically driven macro regime. The escalation of the conflict with Iran has moved energy supply risk back to the center of the global economy. Shipping disruptions through the Strait of Hormuz, attacks on tankers and energy infrastructure, and retaliatory threats from Tehran are already tightening oil markets and raising the risk of sustained inflation pressure.

For investors, the key issue is not simply whether markets fall or rally in the coming weeks. The more important question is how portfolios should be positioned while geopolitical outcomes remain uncertain, and energy markets remain volatile.

The current environment is defined by three overlapping forces: an energy shock, renewed trade tensions, and early signs of tightening financial conditions. Together they are reshaping the risk profile across sectors.

Energy Shock Rewrites the Macro Narrative

The Strait of Hormuz normally carries roughly one-fifth of global oil supply, making it the most important energy shipping corridor in the world. Recent attacks on vessels and mining of shipping lanes have already slowed traffic through the strait, with analysts warning that even partial disruption could remove several million barrels per day from global markets.

Oil prices briefly surged back above $100 per barrel, and diesel markets have tightened sharply as traders attempt to reroute supply chains around the Persian Gulf. Governments are attempting to mitigate the shock through strategic reserve releases and emergency policy measures, but markets remain focused on the possibility that the conflict could spread or prolong shipping disruptions.

The consequences extend well beyond energy markets. Higher fuel costs ripple through transportation, agriculture, and industrial production. Reports already suggest that fertilizer and crop supply chains are becoming vulnerable to rising energy costs, while aluminum production has been curtailed because of logistical disruptions.

For investors, the energy shock is not simply a commodity story—it is a macro transmission mechanism affecting inflation, interest rates, and consumer purchasing power.

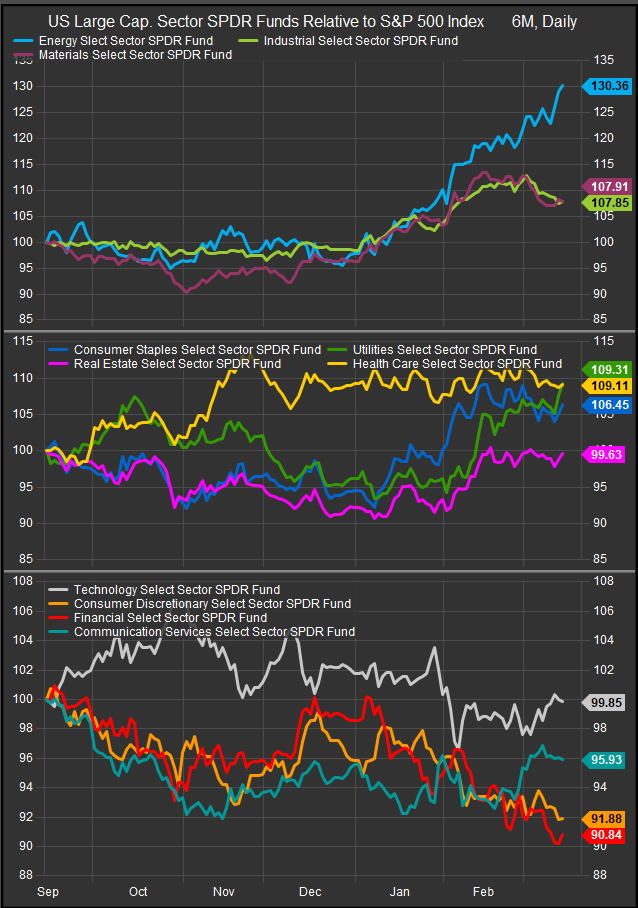

Cyclical Sectors: Direct Beneficiaries of the Energy Regime

Energy companies are the most obvious winners in this environment. With crude prices near $100 per barrel, analysts estimate that U.S. oil producers could generate more than $160 billion in annual free cash flow. These profits are likely to flow directly into dividends, share buybacks, and balance sheet improvements.

Energy security is also becoming a policy priority again. Governments are restarting offshore drilling operations, seeking alternative supply routes, and accelerating investment in energy infrastructure.

Materials companies benefit from the same dynamic. War-related supply disruptions tighten commodity markets, pushing up prices for metals, chemicals, and industrial inputs. Higher energy prices increase production costs across the economy, which often allows commodity producers to exercise pricing power.

Industrial companies represent the second-order beneficiaries of this geopolitical shift. Defense spending is already accelerating, with reports of a $20 billion Pentagon contract with Anduril illustrating the scale of military procurement underway. At the same time, countries are investing in ports, pipelines, and logistics infrastructure to reduce reliance on Middle Eastern shipping routes.

Taken together, these developments support the case for continued exposure to sectors tied to the physical economy—energy production, raw materials, and industrial capacity.

Growth Sectors: Structural Strength, Near-Term Headwinds

Technology and communication services remain the engines of long-term earnings growth. Artificial intelligence investment continues to accelerate, with companies such as Nvidia preparing new chips designed for the rapidly expanding inference market.

But the macro backdrop is becoming more complicated for growth sectors. Higher oil prices push inflation expectations higher and reduce the likelihood of aggressive rate cuts. Markets that previously expected multiple rate reductions now anticipate far fewer.

Higher interest rates increase the discount rate applied to future earnings, which tends to pressure valuations for long-duration growth companies.

Corporate headlines illustrate the tension. Meta is reportedly considering layoffs affecting up to 20% of its workforce as technology companies attempt to offset the enormous costs associated with AI infrastructure buildouts.

Technology remains a core structural sector, but its performance is likely to become more volatile if energy prices remain elevated and monetary policy remains restrictive.

Financial Stress Signals Emerging

Financial conditions are also tightening in subtle ways. Private credit markets—one of the fastest-growing areas of the financial system—are showing early signs of strain.

Reports indicate that major banks are marking down loans linked to private credit portfolios and tightening lending standards. Some private credit funds have already limited investor redemptions after experiencing unusually large withdrawal requests.

Analysts are increasingly concerned that rising defaults among highly leveraged borrowers could expose vulnerabilities in this market, particularly in sectors such as software where AI disruption may threaten traditional business models.

This does not necessarily imply a systemic financial crisis, but it does suggest that credit conditions are becoming less supportive for risk assets.

Consumer Pressure from Energy and Inflation

The consumer sector faces a different challenge: affordability.

Higher gasoline prices function as an immediate tax on households. Rising transportation and food costs reduce disposable income and weaken consumer sentiment. Surveys already indicate that inflation expectations have begun to rise again after several months of decline.

Consumer discretionary companies—particularly retailers, travel companies, and entertainment platforms—are highly sensitive to these shifts in purchasing power.

If energy prices remain elevated for an extended period, consumer spending growth could slow, putting pressure on earnings across the sector.

Tactical Portfolio Positioning

Given the combination of geopolitical risk, energy-driven inflation, and tightening credit conditions, the most prudent near-term portfolio stance is defensive rather than aggressively cyclical.

Low-volatility sectors provide the most effective hedge against a potential market correction while the outcome of the Iran conflict remains uncertain.

Health Care offers stable earnings driven primarily by demographic demand rather than economic cycles.

Consumer Staples benefit from consistent demand even when household budgets are under pressure.

Utilities provide predictable cash flows and often attract capital during periods of market stress.

Real Estate, while sensitive to interest rates, can offer income stability and diversification when volatility rises.

These sectors may not lead markets during strong economic expansions, but they can provide important protection when geopolitical shocks create uncertainty about growth and inflation.

At the same time, investors should approach Financials and Consumer Discretionary sectors with caution. Credit stress emerging in private markets raises the risk of tighter lending conditions, while rising energy costs threaten consumer purchasing power.

Both sectors are particularly vulnerable if inflation remains elevated and financial conditions tighten further.

The Bottom Line

Markets are navigating a complex environment where geopolitics, energy supply, and monetary policy are interacting simultaneously.

The war with Iran has pushed oil markets back to the forefront of macro analysis. Elevated crude prices are feeding into inflation expectations, delaying potential rate cuts, and creating pressure on consumers and credit markets.

While sectors tied to the physical economy—energy, materials, and industrial capacity—continue to benefit structurally from this environment, the near-term risk of market volatility argues for a more cautious stance.

For now, the most sensible approach for sector investors is to tilt portfolios toward low-volatility defensive sectors while reducing exposure to financials and consumer-sensitive industries until the trajectory of the conflict and its impact on energy markets becomes clearer.

In a world where geopolitical risk can move oil prices overnight, portfolio stability may prove just as valuable as growth.

Sources

- Reuters – coverage of Middle East conflict escalation, shipping disruptions, and aluminum production cuts linked to Strait of Hormuz supply risks.

- Bloomberg – reporting on tanker attacks, oil market disruptions, Asian energy diversification, and macro implications of Persian Gulf shipping risks.

- CNBC – analysis of energy market reactions, Fujairah port disruptions, and macro commentary from U.S. officials.

- Financial Times – coverage of private credit market stress and geopolitical risk impacts on global markets.

- Goldman Sachs – commentary on Strait of Hormuz shipping flows and oil market disruptions.

- International Energy Agency – announcement of coordinated strategic petroleum reserve release plans.

- U.S. Bureau of Economic Analysis – PCE inflation and GDP revision data cited in macro discussion.

- U.S. Bureau of Labor Statistics – CPI inflation data referenced in the macro outlook

Other charts and data sourced from FactSet Research Systems Inc.