April 12, 2026

The market backdrop into late April is evolving in a subtle but important way. Rather than a full breakdown in growth, downside risks are re-emerging, driven by renewed geopolitical uncertainty, rising energy costs, and a sharp deterioration in consumer confidence. The failure of U.S.–Iran negotiations and continued tension around the Strait of Hormuz have reintroduced supply-side risks that are feeding directly into inflation expectations and market volatility.

Equities began pricing in a quick recovery; we think Oil prices are likely to remain high on difficulties in US/Iran negotiations.

At the same time, macro data is sending mixed signals. Core inflation remains relatively contained, but headline inflation is reaccelerating due to energy, which rose 10.9% month-over-month with gasoline up more than 21% . More concerning is the collapse in sentiment, with the University of Michigan index falling to 47.6 as households grow increasingly worried about inflation and economic conditions. This combination—sticky inflation alongside weakening confidence—creates a more fragile late-cycle environment where investors begin to prioritize income, stability, and real asset exposure.

\

\

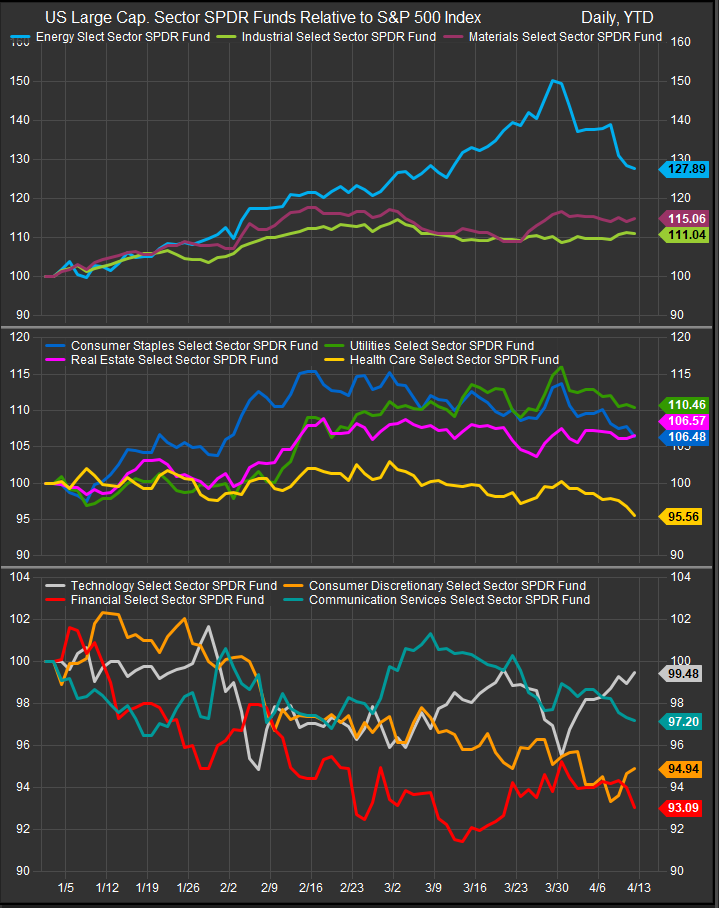

Sharp retracement in Energy Sector performance is likely setting up an accumulation opportunity.

Energy: Pricing Power in a Supply-Constrained System

Energy remains one of the clearest beneficiaries of the current macro setup. The re-emergence of geopolitical risk, particularly around global oil transit routes, is forcing markets to price a more persistent supply premium. Rising gasoline prices and logistical disruptions are already feeding into broader cost structures across the economy.

In this environment, Energy companies stand out for their direct leverage to commodity pricing, strong free cash flow, and capital discipline. Even if oil prices remain volatile, the direction of revisions risk is skewed higher. Importantly, Energy also serves as a portfolio hedge against further geopolitical escalation and inflation surprises, making it one of the more durable outperformers into the remainder of April.

Utilities: Low-Volatility Income Back in Favor

Unlike earlier in the cycle, Utilities are beginning to look more compelling as downside risks re-emerge.

While rate sensitivity remains a consideration, the broader context is shifting. As volatility rises and growth expectations become less certain, investors are increasingly willing to pay for stable cash flows, dividend income, and low volatility characteristics. Utilities offer exactly that—predictable earnings, regulated returns, and relatively low sensitivity to economic cycles.

Additionally, rising energy prices can, in certain cases, support revenue frameworks for regulated utilities, particularly where cost pass-through mechanisms exist. More importantly, if downside risks evolve into broader growth concerns, the market is likely to begin pricing a more dovish policy path. In that scenario, Utilities stand to benefit from declining yields and renewed demand for income-oriented assets.

In short, Utilities are transitioning from a rate headwind story to a defensive income opportunity, particularly in a market where stability is becoming increasingly valuable.

Health Care: Defensive Growth With Policy Support

Health Care continues to offer one of the cleanest combinations of earnings visibility and macro insulation. The sector is largely shielded from consumer spending volatility and geopolitical shocks, while also benefiting from structural demand trends.

Recent policy developments further enhance its outlook. Medicare Advantage rate updates came in stronger than expected, providing a tangible earnings tailwind for managed care companies. In a market where earnings uncertainty is rising, Health Care’s ability to deliver consistent growth independent of macro conditions makes it a core allocation.

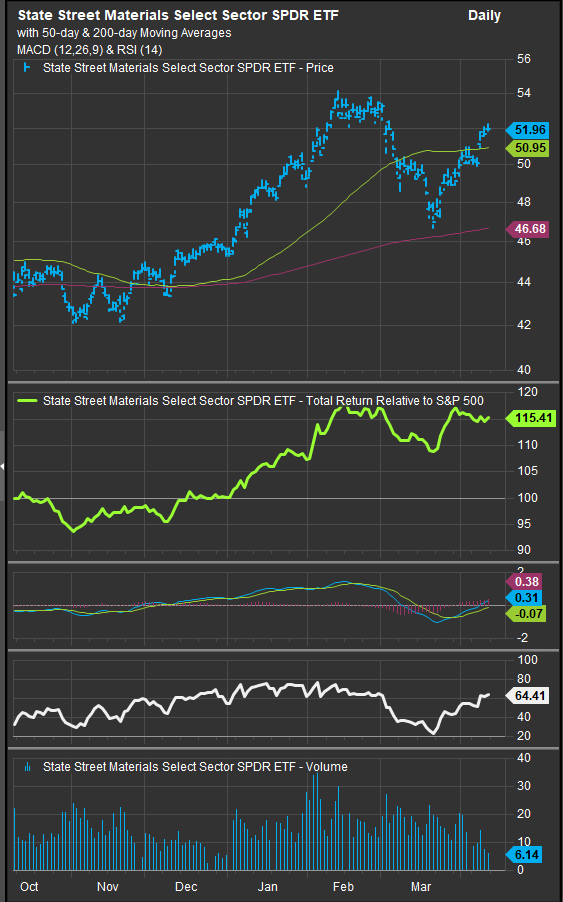

Precious Metals and Materials: Positioning for Policy Pivot

One of the more underappreciated opportunities in the current environment lies in precious metals, particularly gold.

We think investors will continue to buy resource focused exposures.

The combination of rising geopolitical risk, higher inflation expectations, and weakening consumer sentiment creates a classic setup for safe-haven demand. More importantly, if downside risks begin to translate into slower growth, the Federal Reserve may face increasing pressure to shift toward a more accommodative stance. Even though markets are currently pricing limited rate cuts, any shift toward easing would be highly supportive for gold and other precious metals, which benefit from lower real yields and currency debasement dynamics.

Materials more broadly remain tied to global growth expectations and have lagged amid concerns about China and manufacturing softness. However, within the sector, precious metals stand out as a distinct macro hedge, offering upside both in risk-off scenarios and in policy-driven reflation environments.

Industrials: Selective Strength Amid Divergence

Industrials remain supported by structural tailwinds such as infrastructure spending, reshoring, and defense demand, but the sector is becoming more internally differentiated.

Defense and aerospace are clear beneficiaries of rising geopolitical tensions, while energy infrastructure and capital goods tied to supply chain realignment continue to see support. However, transportation and logistics companies face margin pressure from rising fuel costs, highlighting the importance of subsector selection.

Industrials can still outperform, but leadership will likely be concentrated in areas aligned with policy and geopolitical priorities, rather than broad cyclical exposure.

Financials: Stable, but Increasingly Late-Cycle Sensitive

Financials remain supported by elevated rates and ongoing economic expansion, but the re-emergence of downside risks introduces new considerations.

Regulatory scrutiny around private credit exposure and growing concerns about redemption pressures point to potential vulnerabilities in credit markets. At the same time, higher energy costs and weakening consumer sentiment could eventually feed through to credit quality.

While Financials are not yet under significant pressure, they are becoming more sensitive to macro deterioration, suggesting a more neutral stance relative to earlier in the cycle.

Technology and Communication Services: Strong Foundations, Higher Volatility

Growth sectors remain underpinned by strong structural drivers, particularly in AI and digital infrastructure. Corporate commentary continues to highlight robust demand and investment, supporting earnings expectations.

However, the environment is becoming less forgiving. Rising inflation expectations increase discount rates, while valuation sensitivity and competitive pressures are beginning to weigh on performance. Software underperformance relative to semiconductors reflects this shift in investor preference.

The implication is that Technology remains a long-term leader, but near-term performance is likely to be more volatile and selective, favoring areas with clear earnings visibility.

Consumer Sectors: Pressure Building Beneath the Surface

Consumer-facing sectors are increasingly exposed as downside risks build. The collapse in sentiment, rising gasoline prices, and higher inflation expectations are beginning to weigh on purchasing behavior.

While some resilience remains, particularly among higher-income consumers, the broader trend points to growing demand fragility. This creates a challenging backdrop for Consumer Discretionary, while Consumer Staples offer relative stability but face margin pressures from rising costs.

Final Takeaway: Income, Stability, and Real Assets Poised to Regain Leadership

The re-emergence of downside risks is not yet signaling a contraction, but it is clearly reshaping sector leadership. The market is moving away from a pure growth-driven narrative toward one that emphasizes resilience, income, and macro hedging.

Energy and Health Care remain core outperformers, supported by pricing power and earnings visibility. Utilities are re-emerging as a low-volatility income play, particularly if rate expectations begin to shift lower. At the same time, precious metals offer a compelling hedge against both geopolitical risk and potential policy easing.

In contrast, consumer-sensitive sectors and rate-challenged cyclicals face increasing pressure, while Technology requires a more selective approach.

This is a market where defensive quality, income generation, and real asset exposure are once again at a premium, reflecting a late-cycle environment where risks are rising but opportunities remain for disciplined sector positioning.

NOTE: This article and the opinions expressed here in are for information purposes only and do not constitute investment advice.

- StreetAccount Macro Update

- Reuters – Oil markets and geopolitical developments

- Bloomberg – Energy logistics and Strait of Hormuz traffic

- Financial Times – Inflation and earnings trends

- CNBC – Energy prices and macro implications

- University of Michigan / Federal Reserve – Consumer sentiment and inflation expectations

Additional charts and data sourced from Factset Research Systems Inc.