August 17, 2025

In last week’s missive, we noted the narrowing breadth of the bull market as the number of S&P 500 constituents trading above their 200-day moving average remains below 60% which is a lackluster reading with the Index recording several all-time high closes since the beginning of July.

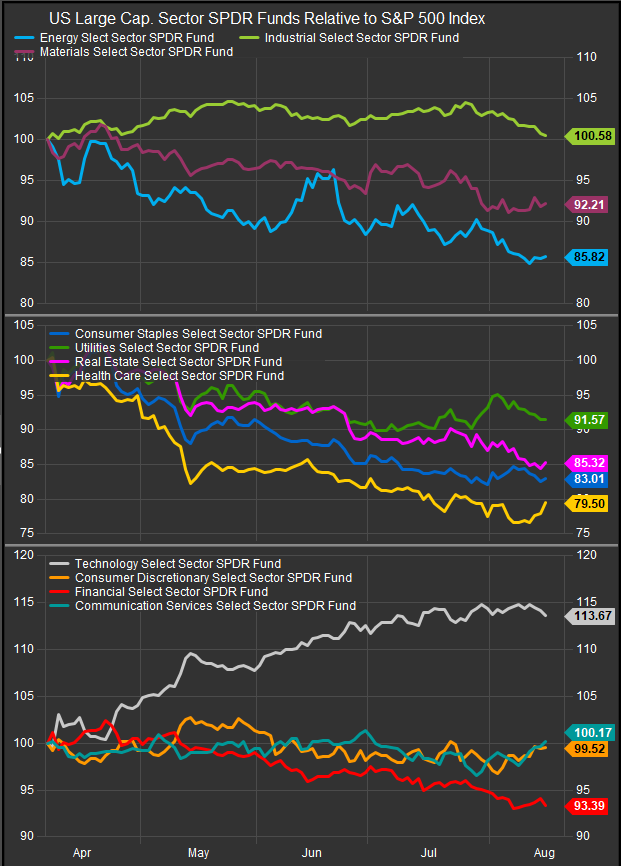

We’ve also noted that since the early April low, the Technology sector has been the only material outperformer and that commodities adjacent sectors (Energy, Materials & Industrials) and low vol. sectors (Utilities, Staples, Real Estate, HC) have been out of favor with Industrials a modest exception. Despite moderating inflation, Consumer Discretionary stocks have lagged as well and that starts to call into question the sustainability of the trend.

Are we all excited about AI? Sure we are. And this isn’t an “AI is a bubble” screed, but we come back to the same question we had last year around this time. If AI is worth so much, why aren’t a more diverse set of public companies benefitting from it. Where is the operational efficiency and productivity gains that will make big restaurant chains like SBUX and MCD more profitable? Why are financial stocks lagging when there is so much potential efficiency to be mined? When we look at sector performance off the April low (chart below), why are so few sectors outperforming?

Information Technology stocks have outperformed the S&P 500 by almost 14% since equities put in their low. The sector is now close to 40% of the S&P 500 by itself. Meanwhile, Consumer Discretionary and Financials stocks have lagged despite the index moving steadily higher. There’s a clear “FOMO” dynamic at play with AI.

With all that said, we finally have some action from the old school. Warren Buffett and Berkshire have stepped in to buy a stake in UNH (chart below) and may have put a backstop in for regular, run of the mill equities. UNH at one time in its history was a successful stock, the biggest health insurer with a massive customer base and a large market share. The important thing is Berkshire’s interest changes the perception of what the company is and its opportunity set and this could be what non-AI stocks need to flourish.

We think the $342 level is an important technical threshold and would confirm bullish reversal.

New technology paradigms have a way of making investors devalue previous modalities in favor of the new. Many of us remember the way the internet got ahead of itself in the late 1990’s. The internet was powerful and allowed for increased profitability, but the upfront projections for it were somewhat absurd. For example, we STILL have brick and mortar stores in 2025. We think the same psychology is at work with stocks and AI right now. AI may eventually give us medical advice, but it won’t hand us our pills and it won’t pay for them either.

We think Buffet’s move is important because it reminds us to value our sobriety and to focus on the bottom line of investments; is the business line profitable, sustainable and of value. Healthcare, Banking, Retail etc., it’s mundane, but these things aren’t going away, and AI isn’t going to do much for us if we don’t have them.

As investors move forward, they should be ready for some rotation out of the AI “FOMO” trade. The August-October period is often a volatile one as 3rd quarter earnings is usually where the rubber meets the road on guidance from early in the year vs. results. We would expect some reflation in Healthcare Sector stocks as well, now that the Oracle of Omaha has made his presence felt.

Patrick Torbert, Editor & Chief Strategist, ETFSector.com

Data sourced from FactSet Research Systems Inc.