April 19, 2026

The current risk-on rally is being supported by a recognizable combination of forces: the market is increasingly willing to believe that the Iran conflict is moving, however unevenly, toward a more controlled phase; systematic and retail flows have turned supportive again; and the domestic macro backdrop still looks resilient enough to prevent an immediate growth scare. The headlines also continue to support the idea that earnings, especially in technology and AI-linked industries, remain the strongest fundamental anchor in the market. Those are the forces keeping equities afloat.

S&P 500 has rallied to fresh all-time highs but has priced in a very optimistic Middle East off-ramp scenario. We’d expect some backing and filling after headlines shifted negative over the weekend.

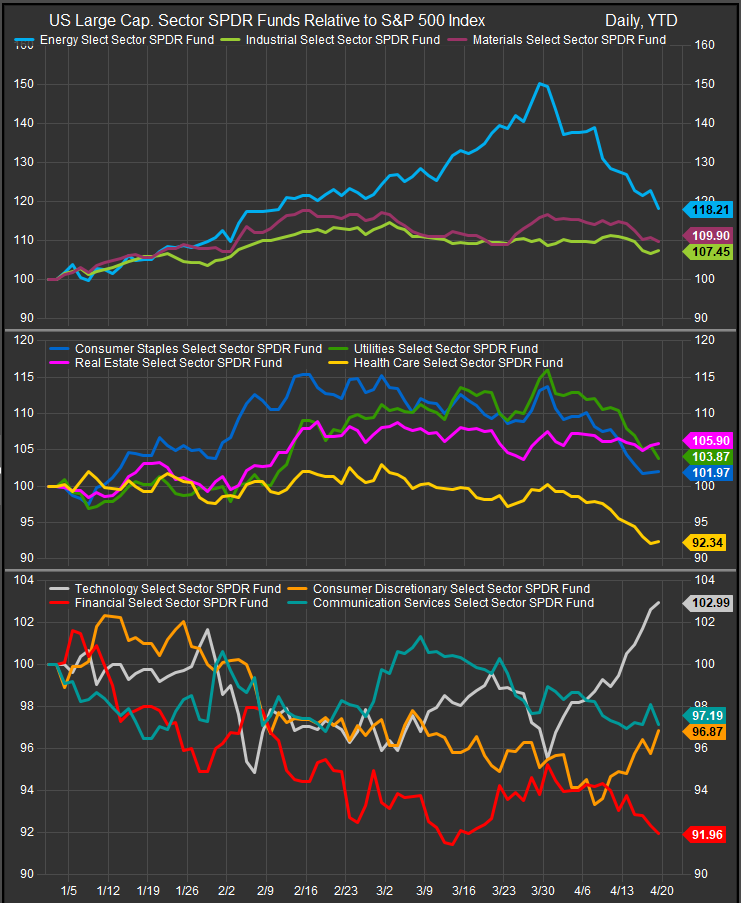

At the same time, the sectors most vulnerable over the next two weeks are becoming more obvious. If investors want to know where the market is least comfortable, the answer is increasingly Healthcare, Financials, and Consumer-facing sectors. That weakness is not just stylistic. It is tied directly to the macro and headline backdrop now unfolding.

The strongest support for the rally still sits with the parts of the market that have the clearest earnings momentum and the least immediate macro sensitivity. The weekend notes highlighted continued enthusiasm around AI demand, including Nvidia’s updated disclosure of more than $1 trillion in Blackwell and Rubin bookings through 2027, positive read-throughs from TSMC and ASML, and the expectation that AI-linked companies will drive more than 60% of S&P 500 EPS growth in the first quarter. FactSet’s latest earnings data reinforce that point: Technology is expected to deliver roughly 45.0% earnings growth in Q1, by far the strongest among all sectors, while overall S&P 500 earnings growth is projected at 12.6% with revenue growth near 9.8%.

The rally has been primarily about Technology stocks, though Discretionary names have bounced in relief as well as rates have moved lower.

That matters because it means investors still have a reason to buy the rally beyond short-covering or peace hopes. The market is not just trading the news cycle around Iran. It is also trading the fact that earnings growth remains concentrated in a narrow but powerful part of the market. That is why Technology and selective Communication Services continue to look like the leadership complex if the advance extends.

But the same weekend material also makes clear which sectors look weakest.

Healthcare is the first. FactSet expects Healthcare to post the largest earnings decline of any major sector in the quarter, at roughly -9.8% year over year, and even when adjusting for the Merck distortion, the sector’s improvement is only modest rather than decisive. In other words, this is not a sector coming into the current environment with strong momentum. Add in the broader market preference for AI, cyclicality, and structural growth, and Healthcare looks increasingly like a funding source rather than a destination for incremental capital. In a market where investors are rewarding earnings acceleration and secular visibility, Healthcare lacks the immediate catalyst that would let it keep up.

Financials also look weaker than the index-level optimism might suggest. On paper, the group still has decent earnings growth expectations, at about 15.1% for the quarter, and large banks have highlighted resilient consumer activity. But the market’s reaction to recent bank earnings was telling. Both JPMorgan and Goldman Sachs declined despite beating expectations, with investors focusing instead on lower net interest income guidance and softer trading performance. At the same time, private credit remains one of the market’s biggest latent worries, with redemption requests building and survey data continuing to identify shadow banking and private credit as the most likely source of a systemic event. This leaves Financials in an uncomfortable position: they are not weak enough to be treated as defensive, but they are not clean enough to be rewarded as cyclical leaders either. The sector is being asked to carry credit risk, rate volatility, and headline risk all at once.

The Consumer sectors look weakest of all on a near-term tactical basis. Recent headlines repeatedly point to a bifurcated spending environment, with lower-income households more exposed to higher energy prices and rate pressure. That matters more now because the Iran conflict is threatening exactly the parts of inflation that hit consumers fastest: gasoline, jet fuel, freight, fertilizers, and food-related costs. Even though there were some positive retail data points earlier in the week, the broader message is still one of fragility. Small-business optimism slipped back below its long-term average, earnings trends weakened, and more owners cited energy-driven uncertainty as a reason for caution. Within equities, luxury also disappointed, with several high-profile European brands missing expectations and citing Middle East disruption alongside softer aspirational demand. Consumer Discretionary looks especially exposed if oil remains high, while Staples may offer some defense but not enough growth to attract leadership capital.

The 4.2% level is setting up as a key potential pivot for the US 10yr treasury yield. Lower from here clears the way for stock level participation to broaden out.

This is what makes the current rally a bit more fragile than the headline index levels suggest. The market is advancing, but it is doing so with narrow participation, with a large share of gains still tied to Big Tech and with cyclical breadth failing to fully confirm the move. The weekend notes explicitly highlighted that only a handful of stocks were making new highs on some of the market’s strongest days, which is not the behavior of a broadly healthy advance. In that kind of tape, the weakest sectors are often the ones that fail first if the macro story deteriorates. Right now, that looks like Healthcare, Financials, and the Consumer complex.

The sectors most likely to benefit over the next two weeks remain the ones with the clearest earnings support and the least direct exposure to energy-sensitive consumer strain. Technology still stands out first, particularly semiconductors and AI infrastructure. Materials remain attractive as a secondary beneficiary given their earnings profile and inflation linkage. Energy still works as a hedge if the Hormuz situation worsens again, though it may be more tactical than structural if diplomacy continues to improve. By contrast, Healthcare lacks momentum, Financials are carrying too much credit and rate baggage, and Consumers remain the most exposed to the next leg of inflation pressure.

Crude price has come down about 30% in the past 2 weeks. Potential for an oversold bounce is growing.

The bottom line is that the rally still has real support behind it, but it is not broad enough to trust blindly. If investors want to stay constructive, they should do so through the sectors where earnings and thematic momentum are strongest. If they want to know where the market is most likely to stumble first, they should look at Healthcare, Financials, and the Consumer sectors, where the fundamental and macro support looks materially weaker right now.

Data sourced from FactSet Research Systems Inc. & StreetAccounts