March 1, 2026

Markets have moved from pricing theoretical geopolitical risk to absorbing live military escalation. Direct U.S.–Israel strikes on Iran, retaliatory missile launches at U.S. bases in Bahrain, Qatar and the UAE, and sharply reduced commercial traffic through the Strait of Hormuz have injected a visible risk premium into crude. The U.S. military presence in the region is reportedly the largest in more than two decades, including deployment of the USS Gerald Ford carrier group and stealth aircraft. Against that backdrop, WTI finished the week near $67 (+0.7%) and Brent near $72.50 (+1.3%), both touching their best levels since July, while refined products posted even stronger gains, with RBOB up nearly 4% on the week.

What makes the move notable is that it has occurred alongside decidedly non-bullish inventory data. The DOE reported a +15.99M barrel crude build — the largest in more than three years — as refinery utilization fell 2.4 points to 88.6%, net crude imports rose more than 400K bpd, and the crude supply adjustment factor surged by 2.739M bpd. U.S. production remains near record levels at roughly 13.7M bpd. Cushing stocks increased by 900K barrels. At the same time, Saudi exports are reportedly running roughly +400K bpd above January levels, and OPEC+ agreed to raise quotas by approximately 137K bpd beginning in April. In short, the physical balance sheet has loosened even as price has firmed. The market is trading geopolitical insurance, not confirmed supply destruction.

That distinction matters for Energy sector positioning. Historically, war-driven oil spikes persist only when barrels are meaningfully removed from the market. Thus far, despite missile exchanges and slowed shipping, there is no confirmed blockade of Hormuz and no multi-million-barrel/day outage. Energy equities have responded constructively but not euphorically, suggesting investors view the move as a hedge rather than a structural inflection. Upstream producers and integrated majors offer geopolitical leverage, but absent sustained disruption, retracement risk remains meaningful.

Based on the technical setup, we expect WTI Crude prices to test towards $80/bbl at minimum which intimates some upside for Energy stocks.

The inflation implications are more durable. January core PPI accelerated +0.8% m/m — the strongest monthly increase since March 2022 — and +3.6% y/y, well above expectations. Trade services rose +2.5% m/m, transportation and warehousing +1.0%, and construction +1.2%, underscoring renewed price pressure in areas sensitive to fuel and logistics costs. If crude remains elevated, that impulse could persist just as labor momentum moderates, with initial claims holding near 212K and nonfarm payrolls expected to rise only about +60K in February versus +130K previously. That combination — firmer inflation and softer growth — supports precious metals and selective Materials exposure, but it does not argue for broad-based cyclical enthusiasm. Industrial inputs remain dependent on sustained manufacturing strength, and ISM is expected to ease from January’s 52.6 print.

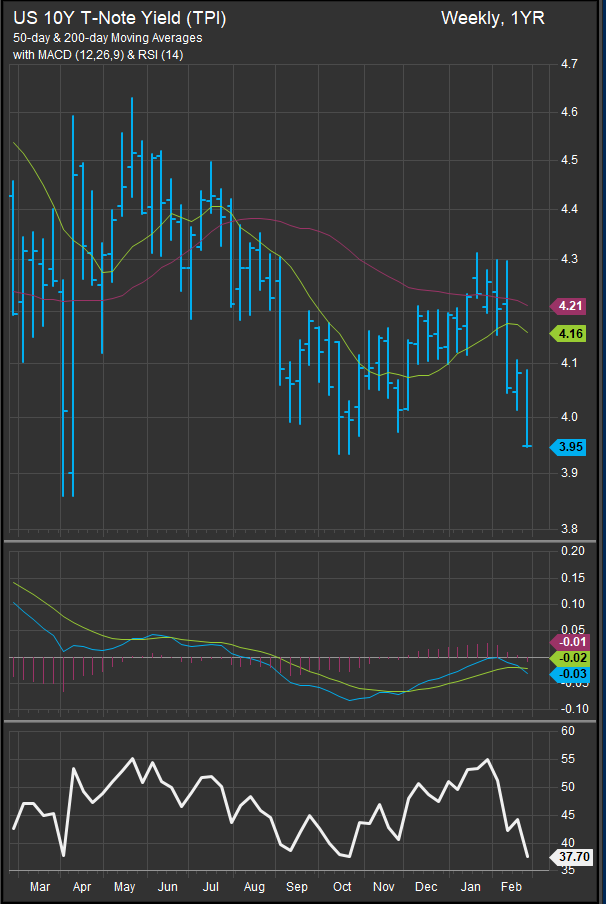

US Treasury Yields are moving towards 52-wek lows favoring continued rotation into defensive sectors.

We’re expecting the S&P 500 to retest near-term support at the 6500 level at minimum. Price structure remains constructive above the 6147 level.

Against this macro backdrop, the portfolio debate sharpens: lean further into low-volatility defensives or accumulate oversold Technology? February’s rotation already pressured high-multiple Growth. Nvidia erased roughly $260B in market value in a single session despite delivering a ~$2B revenue beat and a ~$6B raise, while more than $220B in software ETF market cap evaporated during the AI-disruption-driven selloff earlier in the month. Block’s decision to cut roughly 40% of its workforce and CoreWeave’s plan to spend $30–35B in 2026 capex against $12–13B in expected sales amplified concerns about AI ROI and white-collar displacement. Yet positioning data showed record short exposure in Software & Services, and Nvidia maintained 75% gross margin guidance with continued visibility into Blackwell demand. Dell projected AI server revenue doubling to $50B by FY27. Flows into U.S. equities remained positive, with roughly $37B year-to-date inflows.

Resources focused and defensive sectors have already seen inflows in 2026. We think that continues in the near-term.

Geopolitical escalation typically drives capital toward Utilities, Consumer Staples, Healthcare and other low-beta exposures, particularly with the 10-year Treasury yield hovering near 4%. That ballast remains appropriate while escalation risk is high and crude is bid on fear. However, if Hormuz remains open and inventories continue to build, the oil spike could prove temporary, inflation expectations stabilize, and compressed Technology valuations re-rate quickly. In that scenario, investors who abandoned Growth entirely risk missing the rebound.

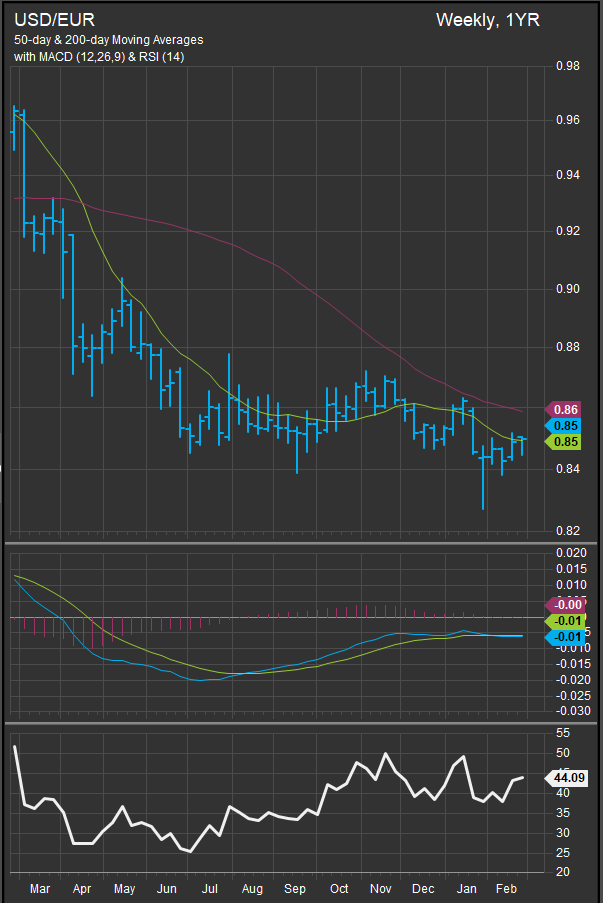

Near-term, USD has strengthened. This could eventually challenge the near-term rise in commodities prices…

However, in the near-term the Bloomberg Commodities Index is being bought near overbought levels.

The data therefore argue for balance rather than binary positioning. Energy exposure can serve as geopolitical insurance given active military engagement, but the +15.99M barrel inventory build and rising OPEC supply caution against aggressive overweights. Materials exposure should skew toward precious metals rather than broad industrial cyclicals given the +0.8% core PPI shock and moderating growth signals. Low-volatility sectors provide stability if escalation deepens, yet selectively adding to high-quality, oversold Technology franchises is justified by positioning unwind and durable compute demand.

In a market where record inventory builds coexist with missile exchanges and inflation acceleration, prudence favors hedged portfolios — defensive enough to withstand escalation, but flexible enough to participate if the war premium fades. With a backdrop of economic late-cycle to consider, we think investors will start out on a cautious footing. Further down the road when the dust settles, there may be some interesting buying opportunities if rates go lower.

Sources

- U.S. Energy Information Administration (EIA) – Weekly Petroleum Status Report (week-ended 20-February 2026)

- U.S. Energy Information Administration – Natural Gas Storage Report

- OPEC+ April production quota announcement

- Vortexa crude export and floating storage data

- Bloomberg – Oil markets, OPEC+ policy, CoreWeave capex plans, payroll expectations

- Reuters – Middle East military developments; Saudi export data; PPI coverage

- Financial Times – OPEC+ output decision; AI capital expenditure commentary

- CNBC – Block workforce reduction; Nvidia coverage

- U.S. Bureau of Labor Statistics – January PPI report

- CME Group – WTI/Brent futures pricing

- Conference Board – Consumer confidence (February)

Additional charts and data sourced from FactSet Research Systems Inc.