April 5, 2026

The market is being asked to do something genuinely difficult right now: price a war with no clear endpoint, absorb a labor market that is softening but not breaking, and separate the durable structural winners from the cyclical noise. The headlines from this week sketch a reasonably clear map of where risk is concentrated and where opportunity is quietly accumulating.

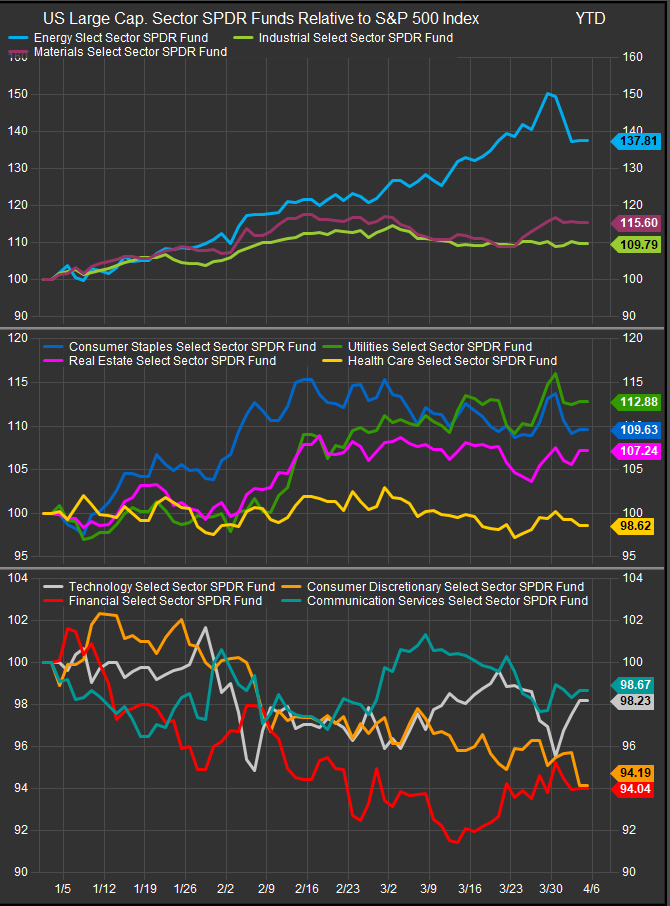

Energy: The Most Asymmetric Trade in the Market

No other sector offers this combination of visible upside, quantifiable supply math, and genuine tail risk—in both directions.

The arithmetic is stark. UBS estimates a current supply shortfall of roughly 12 million barrels per day. BofA warns that a sustained loss of more than 10M bpd could push Brent crude to $150–$200/bbl. Gulf producers have cut at least 10M bpd; the Hormuz closure alone removed roughly 20M bpd of crude and refined products from global trade. Roughly 60% of that has been offset through pipeline rerouting, inventory drawdowns, and strategic reserve releases. Those buffers are finite and visibly eroding.

The demand destruction that economists have been modeling as a risk is beginning to materialize as a fact. Shell is already flagging jet fuel reductions. Eight countries have implemented work-from-home mandates; twelve have imposed fuel price controls. JPMorgan warns that roughly 5M bpd of Saudi bypass capacity is now at risk from Houthi escalation—a dynamic that could add another $20/bbl to prices on its own.

OPEC+’s in-principle agreement to raise May production quotas by 206,000 barrels is largely symbolic given how much Mideast output is shut in. The real story is the structural elevation in the war risk premium, which is not going away before the Monday press conference, Tuesday’s threatened strikes on Iranian power plants, or any near-term diplomatic development.

Sector posture: Overweight. The energy sector is the most direct expression of the macro environment. Integrated majors and LNG producers with global diversification have the earnings power and the balance sheets to absorb volatility while capturing upside. Pipeline and infrastructure operators benefit from the permanent re-routing of trade flows regardless of how the conflict resolves. The setup favors Energy over every other sector in the market today.

Despite some near-term rotation into Growth-exposed sectors, Energy remains supported by macro level tailwinds.

Industrials and Materials: Defense Drives the Cycle

Trump’s proposed FY27 budget includes a $441 billion year-over-year increase in defense spending—a figure without modern precedent. That is not a political talking point; it is a revenue forecast for the defense industrial base.

The near-term operational constraint is interceptor missile supply. Defense analysts and the New York Times have been sounding persistent alarms about dwindling inventories. This conflict has consumed air-defense capability at a rate that surprised planners, and replenishment is a multi-year process. Companies with direct exposure to missile defense manufacturing and precision munitions are not merely budget beneficiaries—they are operationally essential in a way that creates durable demand regardless of when the conflict ends.

Aluminum and industrial metals deserve attention on the materials side. Emirates Global Aluminum and Aluminium Bahrain both reported significant damage from drone strikes, affecting roughly 4% of global primary aluminum supply. Infrastructure damage in a war zone does not get repaired quickly. The supply shock in aluminum is real, and it feeds directly into aerospace, automotive, and construction cost structures. ISM manufacturing prices jumped to 78.3 in March—the highest since June 2022—partly because of exactly this dynamic.

Sector posture: Overweight Industrials (defense), Neutral-to-Overweight Materials. The defense budget increase is large enough and durable enough to support multi-year earnings revisions upward. Materials is more complex—energy input cost pressure is a headwind for processing-intensive producers, but supply disruption is a tailwind for price realization. Be selective.

Technology: A Sector at War With Itself

Technology is not one trade right now. It is two trades moving in opposite directions simultaneously, and conflating them is a portfolio mistake.

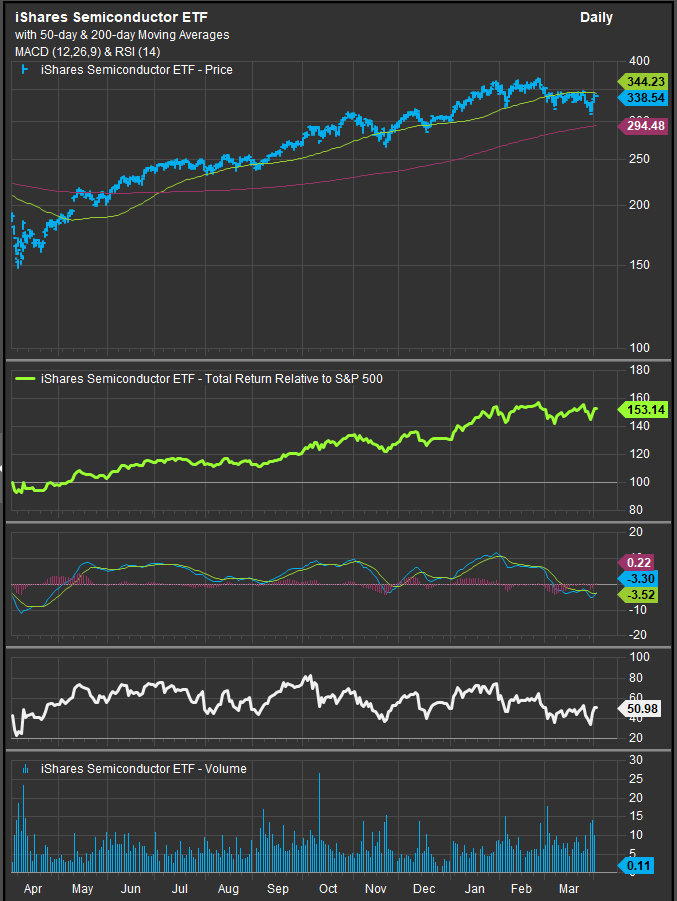

The semiconductor and AI infrastructure side is in what analysts are genuinely calling a supercycle. Samsung is expected to report a massive jump in operating profit driven by surging high-bandwidth memory demand. Foxconn is reporting strong AI-driven demand. OpenAI just closed a $122 billion funding round at an $852 billion implied valuation—the largest in venture history. KKR closed its largest-ever North American fund at $23 billion with AI and infrastructure as core themes. Capital continues to flow into this complex at a rate that has not slowed despite the geopolitical backdrop, which is itself a signal.

The consumer-facing side is a different story entirely. Nike’s 15.5% single-session collapse—its third-worst in history—was not a company-specific event. It was a message about consumer willingness to pay for premium discretionary technology and lifestyle products when energy costs are rising and labor market uncertainty is building. RH’s 19% drop told the same story from a different angle. March Challenger layoffs in technology are up 40% year-over-year; AI is now the leading stated cause of job cuts, accounting for 25% of total announced cuts.

The datacenter power story bridges both sides of the sector. New Jersey is the latest state grappling with electric rate spikes driven by datacenter load—a political and operational headwind for utilities, but a sustained tailwind for power generation and grid infrastructure investment that will compound for years.

Sector posture: Overweight semiconductors and AI hardware; Underweight consumer-facing software and platforms. The divergence within Technology will widen before it narrows. The structural winners are those supplying the physical layer of AI infrastructure. The laggards are those dependent on a consumer whose wallet is being squeezed from both ends.

Internet and Software stocks have been under pressure from AI disruption while Semiconductor stock have benefitted.

Utilities and Industrials (Power Infrastructure): The Overlooked Beneficiary

This theme sits at the intersection of Technology and Energy and deserves its own treatment. Datacenter load growth is creating electricity demand at a pace that grid infrastructure was not built to handle. States from New Jersey to Virginia are dealing with rate spikes and political backlash. That pressure does not resolve through conservation—it resolves through investment in generation capacity, transmission, and grid modernization.

Separately, the Iran conflict has elevated the strategic value of domestic energy infrastructure broadly. The combination of AI-driven power demand and war-driven energy security concerns creates a durable, bipartisan political tailwind for grid investment that cuts across both parties’ stated priorities.

Sector posture: Overweight Utilities with significant generation growth capex and industrial electrical equipment manufacturers. This is a patient trade with a multi-year payoff, but the entry point here—before the grid investment supercycle is fully priced—remains attractive.

Financials: Caught Between the Fed and the Credit Cycle

The Federal Reserve is effectively frozen. Powell’s message at Harvard was analytically correct and operationally unhelpful: Fed tools have limited impact on supply-side shocks, inflation expectations remain anchored, tariff-driven price increases are largely one-time. All true. Also true: March CPI is expected to show a sharp rise on gas prices, the Fed cannot cut into that, and the Senate Banking Committee’s April 16 hearing on Kevin Warsh’s Fed nomination adds political uncertainty to an already complicated picture.

The private credit stress signal from Blue Owl is worth taking seriously even if the systemic contagion risk is limited. Redemption requests of 22% at OCIC and 42% at OTIC—against a 5% withdrawal cap—are well above what the buyside expected. Powell’s reassurance that private credit is a small portion of the overall asset pool is technically accurate but incomplete: the sector’s opacity and embedded leverage mean that stress, when it surfaces, surfaces suddenly.

Sector posture: Underweight. Rate-sensitive net interest income is not recovering in this environment. Non-traded private credit carries liquidity risk that is not fully priced. The one area of relative interest is transaction-oriented investment banking, which is benefiting from the M&A wave—Q1 set a record for large deal count—but even that is a selective, not a broad-sector, thesis.

Consumer Staples: Consolidation as a Survival Strategy

The week’s M&A headlines—Unilever merging its food business with McCormick to create a $65 billion food giant, Sysco acquiring Jetro Restaurant Depot for $29.1 billion—are not coincidences. They reflect a sector under structural pressure consolidating to find the operating leverage and distribution scale it cannot generate organically. Shifting consumer preferences, rising energy input costs, tariff uncertainty, and slowing growth are the structural forces; M&A is the response.

Consumer confidence at 91.8 beat expectations in March, and February retail sales were the strongest since July 2025. The resilient consumer narrative is not dead. But the write-in responses in the Conference Board survey skewed pessimistic, and the gap between present-situation strength and expectations-component weakness is a classic late-cycle pattern.

Sector posture: Neutral-to-Overweight for staples with genuine pricing power and vertically integrated supply chains. The M&A consolidation wave creates event-driven opportunities. The macro backdrop—energy cost pass-through pressure, tariff headwinds—favors scale and supply chain control.

Consumer Discretionary: Fragile Until Proven Otherwise

Nike and RH said what needed to be said this week. The high-end consumer is being squeezed. Energy costs are rising. Labor market uncertainty is building. The expectation component of consumer confidence turned lower even as the present-situation index held up—a pattern that typically precedes softening in big-ticket and discretionary spending.

The US economy is outperforming its allies, and the labor market is not breaking: initial claims at 202,000 beat a 212,000 consensus, and the March payrolls print of +178,000 was well ahead of expectations. But the Challenger data—tech layoffs up 40% year-over-year, AI displacement now the leading stated cause—suggests the composition of labor market stress is quietly shifting.

Sector posture: Underweight. There is no credible near-term demand recovery catalyst, and the energy cost headwind is additive to existing tariff and macro pressures. The consumer is resilient; the consumer is not robust.

The Macro Frame and Portfolio Posture

The jobs data and ISM manufacturing data argue that the US economy is holding. The energy price data, the ISM prices component, and the CPI forecast argue that inflation is re-accelerating. The Fed cannot cut into that combination, and the conflict that is driving it has no credible off-ramp inside the next 96 hours.

Goldman Sachs noted that hedge fund net selling over the trailing six weeks was the third-largest in a decade. CTAs sold nearly $55 billion in US equities since the start of the war. The positioning bounce this week was real—but it was driven by short-covering and month-end dynamics, not by a fundamental change in the backdrop.

The S&P 500 is down 4.6% in Q1, its worst quarterly performance since Q3 2022. That is the market’s verdict on the current environment. The question for Q2 is whether the conflict provides the offramp investors are priced for, or whether Trump’s “extremely hard over the next two to three weeks” framing proves to be the more accurate guide.

Position for duration, not for the off-ramp. Our outlook on Technology nets out to a tactical underweight, as we think the market is overly optimistic about Iran off-ramp scenarios. We expect equities to test lower over the next several weeks. Market internals are nearing wash-out levels, but we haven’t seen signs of clear investor capitulation which typically arrive at major bottoms in the market.

| Sector | Posture |

| Energy | Overweight |

| Industrials (Defense) | Overweight |

| Technology (Semiconductors / AI Hardware) | Overweight |

| Utilities (Power Infrastructure) | Overweight |

| Materials | Overweight |

| Consumer Staples | Neutral-to-Overweight |

| Financials | Underweight |

| Consumer Discretionary | Underweight |

| Technology (Consumer Platforms / Software) | Underweight |

Sources

- Axios — Trump threats on Iranian power plants; FY27 defense budget

- Bloomberg — Hormuz strategic focus; OPEC+ quota increase; Iran “friendly ships” restriction; US reinsurance guarantees; Kevin Warsh Fed nomination hearing; Powell private credit comments

- Reuters — OPEC+ production agreement; Iraqi crude transit exemption; India Iranian crude purchase; ISM manufacturing; ADP payrolls; Foxconn earnings; Samsung operating profit; consumer M&A deals

- The New York Times — Interceptor missile supply concerns; Iranian officials’ negotiating posture

- Washington Post — F-15 crew recovery; post-Bondi cabinet replacement speculation

- CNBC — Nonfarm payrolls; Fed Governor Miran comments; Warsh nomination hearing

- Politico — Judge reaffirms Powell subpoena ruling; New Jersey electric rates; Trump speech reaction

- CBS News — Chicago Fed Goolsbee on rate cuts

- Financial Times — Private credit stress; Blue Owl redemption requests; jet fuel demand destruction

- Goldman Sachs (via Bloomberg) — Hedge fund net selling; CTA positioning

- UBS — Supply shortfall estimate; Brent crude price target

- BofA — Oil price spike scenario; consumer energy spending share

- JPMorgan — Saudi bypass capacity risk; Asian demand destruction measures

- Wells Fargo — US oil intensity per $1,000 GDP

- IEA — Gulf production cuts; Hormuz trade flow disruption

- EIA — Benchmark crude price context

- Challenger, Gray & Christmas — March job cut report

- Conference Board — March consumer confidence

- S&P Global — Final March Manufacturing PMI