February 22, 2026

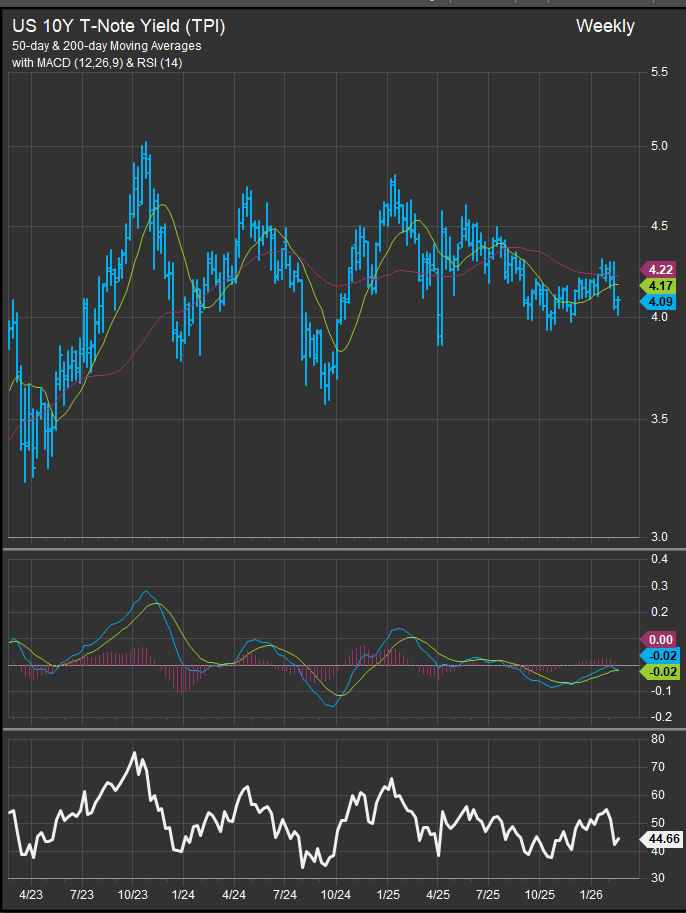

The market is at an inflection point, and the deciding variable remains interest rates. The U.S. 10-year Treasury yield has been oscillating in the low-4% range — high enough to pressure equity multiples, but not high enough to choke off risk appetite outright. Whether investors lean further into defensives or rotate back into oversold Growth exposure will hinge on whether that rate backdrop remains stable.

The Macro Backdrop: Slowing but Not Stalling

The economic data paint a late-cycle picture rather than a recessionary one. Q4 GDP came in at +1.4%, below the prior quarter’s +4.4%, signaling deceleration. However, industrial production rose 0.7% month-over-month in January, and core capital goods shipments (a proxy for business investment) climbed 0.9% m/m — both stronger than consensus expectations. Manufacturing PMIs have cooled but remain in expansion territory above 50.

Inflation remains sticky. Core PCE rose 0.4% m/m in December and 3.0% year-over-year — the highest since late 2023. That limits the Federal Reserve’s flexibility and helps explain why markets still price the first rate cut around mid-year.

Earnings remain a bright spot. S&P 500 Q4 earnings growth is running above +13% y/y, roughly five percentage points ahead of initial expectations. That is not consistent with imminent contraction.

In short: growth is moderating, inflation is uneven, but corporate profitability is resilient.

S&P 500 price action has shown weakening momentum since October 2025. Near-term price support resides at the 6530 level.

The Defensive Argument

The case for defensive positioning rests on three pillars: rate sensitivity, geopolitical risk, and late-cycle dispersion.

If the 10-year yield were to break materially above the low-4% range, financial conditions would tighten meaningfully. Real Estate, Utilities, and high-multiple equities would face renewed pressure. Defensive sectors such as Health Care and Consumer Staples — represented by ETFs like XLV and XLP — tend to outperform when volatility rises and earnings expectations flatten.

Insurance stocks, for example, have been under pressure despite benefiting from higher investment income. Names like Travelers (TRV) and Allstate (ALL) have lagged amid catastrophe-loss volatility and reserve scrutiny. This illustrates how late-cycle environments punish even steady earners when uncertainty rises.

Energy, by contrast, has benefited from geopolitical tension and oil strength. ETFs like XLE have outperformed amid concerns over potential U.S.–Iran escalation. Midstream MLPs — accessible via vehicles such as AMLP — continue to offer yields well above 6%, supported by fee-based cash flows and relatively stable volume demand. As long as rates remain near current levels, that income premium looks attractive.

The Growth Argument

The counterargument is that Growth has already digested much of its valuation excess.

The Technology sector’s forward P/E premium versus the S&P 500 has compressed significantly from 2023–24 extremes. ETFs like XLK and QQQ have traded sideways as investors reassessed AI capital intensity. Nvidia (NVDA) has been rangebound despite continued data center demand, reflecting caution rather than deterioration.

At the same time, business equipment production rose 0.9% m/m, and manufacturing output saw its largest increase in nearly a year. That aligns with continued AI infrastructure and industrial capex momentum.

AI competition fears are clearly in the headlines. OpenAI’s revised compute target of ~$600B through 2030, versus previously discussed trillion-dollar infrastructure narratives, has sparked debate about monetization timelines. Software names have lagged, with investors scrutinizing margin durability and customer spending patterns.

Yet earnings data remain supportive. Semiconductor and hardware suppliers continue to guide for double-digit revenue growth tied to AI workloads. Industrial automation and design software companies have cited expanding usage rather than shrinking demand.

If real yields stabilize or drift modestly lower — not because of recession, but because inflation moderates — Growth multiples could expand from more sustainable levels.

The Q’s have been faded since October but have a chance to bounce off oversold levels. The key will be whether buyers can push the momentum oscillator above the 60 level. Failure to do so confirms the waning risk appetite narrative.

Real Estate: Early Signs of Stabilization

Housing starts surprised to the upside at 1.4 million annualized units, the strongest since mid-2025. However, pending home sales declined again, underscoring affordability constraints. REIT ETFs such as VNQ have attempted to base but remain sensitive to rate direction. A sustained drop in yields would likely catalyze stronger performance; a rate spike would delay recovery.

So Which Case Is Stronger?

At present, the data do not demand an outright defensive pivot. Earnings growth above +13% y/y, improving capital goods data, and stable consumer spending suggest the economy is not contracting.

However, inflation at 3.0% core PCE and tariff escalation create upward pressure on yields. If the 10-year remains anchored near current levels, the environment supports a selective re-risking into high-quality Growth — particularly large-cap franchises with durable free cash flow and global scale.

If yields rise meaningfully or geopolitical tensions intensify, defensives and income-oriented sectors regain the upper hand.

The Balance

The more compelling approach may be a barbell strategy:

- Maintain exposure to Energy (XLE), midstream income (AMLP), and high-quality Financials.

- Gradually add oversold Growth via XLK or QQQ where valuations have normalized.

- Hold Health Care and Staples as volatility ballast.

This is not a binary risk-on or risk-off moment. It is a rate-sensitive environment where discipline matters more than narrative.

While the US 10yr Treasury Yield has been sensitive to inflation, the longer-term path has been sideways to lower since late 2023.

The deciding factor will not be tariff headlines or AI debates alone. It will be whether the bond market signals stability — or stress. If shorter duration yields move higher, it means the Fed. has lost control. That doesn’t seem like the cogent risk at the moment, but with commodities prices surging recently on renewed USD weakness, it isn’t totally off the table. Keep a close eye on the MAG7 at oversold levels. Low rates plus a Mag7 bounce is a clear recipe of cycle continuation. Low rates and continued strength from Utilities, Staples and Healthcare is a signal investors are moving towards the exit on the cycle.

Sources

-

U.S. Bureau of Economic Analysis (BEA)

-

Q4 GDP (Advance Estimate)

-

Personal Consumption Expenditures (PCE) Price Index

-

-

U.S. Bureau of Labor Statistics (BLS)

-

Industrial Production

-

Manufacturing Output

-

Consumer Price Index (CPI)

-

-

Federal Reserve (FOMC Minutes & Statements)

-

January FOMC Minutes

-

Policy rate expectations

-

-

FactSet Research Systems

-

S&P 500 Q4 earnings growth (~+13% y/y)

-

Sector earnings revisions

-

Forward P/E comparisons (Technology vs. S&P 500)

-

-

S&P Global

-

Flash Manufacturing and Services PMI (February)

-

-

CME Group – FedWatch Tool

-

Market-implied rate cut probabilities

-

-

U.S. Census Bureau

-

Housing Starts

-

New Home Sales

-

Durable Goods Orders

-

-

NYSE / ETF Sponsor Data (State Street, Invesco, BlackRock, Alerian)

-

Sector ETF performance and valuation data for:

-

Technology (XLK, QQQ)

-

Energy (XLE)

-

Real Estate (VNQ)

-

Health Care (XLV)

-

Consumer Staples (XLP)

-

Midstream / MLPs (AMLP)

-

-

Additional charts and data sourced from FactSet Research Systems Inc.