SPY June Outlook—Inflation concerns have faded in the near-term partly due to a struggling consumer. The outlook for June is mixed with seasonality a tactical negative historically against the backdrop of a longer-term bull market trend.

Price Action & Performance

The S&P 500 confirmed the bull trend higher in May with rates rolling over below cycle highs and Crude oil moving from near-term overbought to oversold. That led to outperformance from a mixture of Growth and min vol. sectors at the expense of cyclicality. We are seeing some narrowing of breadth and leadership beneath the surface, so it’s hard to be extremely aggressive in our positioning, but the bull trend remains intact over the longer-term and commodities prices have firmed, but are short of breaking out, so we give the benefit of the doubt to Growth leadership and remain long XLK and XLC after our pivot in mid-May.

Economic and Policy Drivers

May’s CPI report came in a shade lower than expected which combined with another blow-out quarter from NVDA to shift the narrative back towards the potential of Growth stocks and AI. Despite a slightly softer inflation print, the market still swings on hawkish/dovish commentary from the Fed. And we are still seemingly in a feedback loop where weak eco data puts downward pressure on rates which in turn spurs investors to bid up equities which then rekindles the specter of inflation pressure. Our fundamental insight is that the consumer is showing weakness as the cost of financing and various services has risen more than the broad inflation gauge. The housing market has slowed, and discretionary spending has been weakening despite higher equity prices. Expect this dynamic to continue unless the Fed. signals a more decisive policy change towards easing rates. We’ve seen this reflected in earnings with XLP constituents COST and WMT posting big beats on consumers trading down to find value.

How Can Sector Investing Help?

This month we are recommending investors lighten up on Consumer exposure and we are expecting rates flat to lower and equities likely to consolidate. We expect the weakest sectors to be Discretionary (XLY), Energy (XLE), and Real Estate (XLRE). We have written several times about deterioration in the Discretionary sector, from consolidation in homebuilders and slowing home sales, home improvement sales, auto sales and overall spending. Our research suggests a flat-to lower rate environment backed by a strong equity uptrend, typically supports a mixture of Growth and Defensive exposures. We also see a propensity for the market to rotate in and out of Tech and Cyclicality with the former outperforming in May while the latter had been the place to be from February through April. With that backdrop we are advocating to underweight XLY (continues to deteriorate), XLE (volatile, negative crude trend) and XLRE (a structural laggard in the cycle). We would counsel to take excess funds from the underweight sectors and put them in a mix of longer-term Growth leadership (XLK, XLC) and a mix of lagging cyclicality and defensive exposures in case there is a more serious correction in YTD winners as the calendar moves to its seasonally weak period.

In Conclusion

Last month was more stalemate between Fed policy and Inflation gauges. Almost in the background, the equity markets continued higher. We are now in the summer of an election year which typically sees equity markets consolidate into November 5th. We will start the month positioned for rates to stay flat and for equities to grind sideways over the intermediate term while respecting the strongest longer-term outperformance trends in XLK and XLC.

ETFsector has created the Elev8 Sector Selection Portfolio as a framework for establishing a differentiated view on a monthly basis vs. our S&P 500 benchmark. Our starting weights for June are as follows:

| Sector SPDR | +/- |

| XLC | 3.22% |

| XLK | 2.92% |

| XLI | 2.46% |

| XLP | 1.98% |

| XLB | 1.68% |

| XLU | 1.52% |

| XLF | 1.10% |

| XLV | 1.02% |

| XLRE | -2.18% |

| XLE | -3.86% |

| XLY | -9.86% |

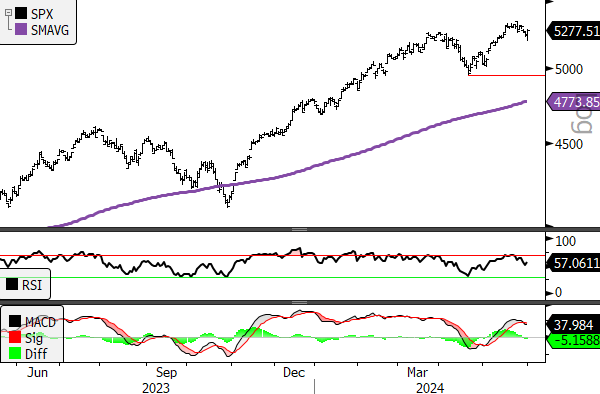

Chart | S&P 500 Technicals

S&P 500 12-month, daily price (200-day m.a.|14-day RSI|12, 26, 9 MACD)

- S&P 500 re-established its uptrend in May

- MACD and RSI momentum gauges are showing negative divergence which is often a precursor to more prolonged consolidation

- Consumer Discretionary looks like the weakest sector from a Technical and Fundamental Perspective

Data sourced from Bloomberg