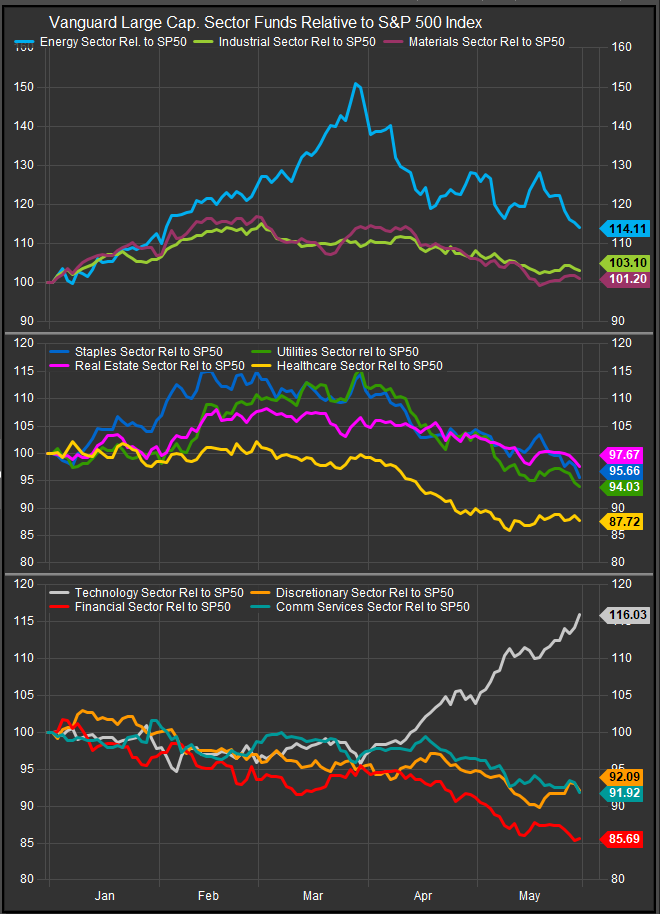

May marked a clearer recognition phase for equities: investors have largely embraced the AI paradigm and are now discounting a full long-term build-out of capability across compute, memory, networking, cloud infrastructure, software, power and cooling. The result was a strong tape at the index level, with the Dow, S&P 500 and Nasdaq ending May at record closes, but the sector story remained highly concentrated. StreetAccount’s May recap showed Technology up 15.91% for the month, while most other sectors lagged, including Energy, Utilities, Staples, Financials, Real Estate, Industrials, Communication Services and Materials.

That narrow leadership is important. It suggests the market has high conviction in the AI infrastructure build-out, but much less conviction about the downstream effects of the new paradigm. Investors can see the demand for servers, semiconductors, memory, cloud capacity and data-center equipment. What is still uncertain is who ultimately captures the productivity gains once AI is embedded across the broader economy. It is not obvious that established operating companies will have an advantage in applying AI to legacy business models. In many cases, the largest public companies outside the AI ecosystem may be the most exposed to systemic disruption because they control the biggest profit pools, customer relationships and workflow bottlenecks for AI-native competitors to attack.

The latest data reflected that divide. Broad-market equity exposure performed well, but the real leadership sat in AI-linked technology. Semiconductor, software, cloud, quantum and broader AI ETFs delivered some of the strongest monthly gains, with SOXX up 26.5%, QTUM up 22.9%, AIQ up 22.3%, IGV up 20.3%, SMH up 19.9% and VGT up 17.4%. Flows also showed investors continuing to fund the theme, particularly in software, semiconductors, quantum and AI-oriented exposures. This was less a normal growth rally than a repricing of the physical and software architecture required to support a new computing era.

The Technology Sector is the only alpha source in the S&P 500 at the sector level in 2026

AI, but most specifically the AI infrastructure component is juicing returns in the near-term. The AI infrastructure focused TCAI ETF has lapped the traditional AI exposures since the beginning of 2026.

The earnings and headline backdrop reinforced the same conclusion. StreetAccount highlighted continued AI tailwinds from intense compute demand and expansive capex plans, while also noting that investors and policymakers are still debating monetization, ROI and the timeline for productivity gains. Q1 earnings also showed a large divergence between the Magnificent 7 and the rest of the market, underscoring why investors remain willing to pay for proximity to the AI operating stack.

For sector investors, this favors Technology, but with more selectivity. The market is rewarding the sellers of AI capability before it rewards the users of AI capability. Semiconductors, memory, networking, cloud infrastructure, AI software, data management and power-adjacent hardware remain the cleanest ways to express the build-out. At the same time, positioning is crowded. Weekend headlines flagged rising scrutiny around momentum, concentration and leveraged exposure to AI leadership, while “tokenmaxxing” and AI spending discipline are emerging as early reminders that enterprise ROI still matters.

Industrials and infrastructure are becoming the second layer of the AI trade, but the market is still selective. Solar was a standout in the latest data, and defense/aerospace exposures also performed well, supported by power demand, data-center infrastructure needs and rearmament themes. Utilities, however, lagged despite the obvious AI electricity-demand story. That distinction matters: the market appears more willing to pay for equipment, cooling, grid and infrastructure suppliers than for regulated utility exposure where capex funding, rate sensitivity and politics may dilute the benefit.

Energy was the clearest laggard. Oil fell sharply in May as U.S.-Iran deal hopes pressured crude, and the latest data showed broad weakness across energy and oil-services exposures. Energy remains useful as a geopolitical hedge and cash-flow sleeve, but it was not aligned with the month’s dominant AI recognition trade.

The consumer, financial and healthcare sectors look more complicated. Consumer resilience remains intact at the aggregate level, but StreetAccount noted growing concern around affordability, lower-income stress, buyer caution and a widening K-shaped backdrop. Financials face a similar issue: AI can improve underwriting, service, compliance and advisory workflows, but it can also attack legacy cost structures and distribution advantages. Healthcare has meaningful AI applications, but leadership remains more catalyst-driven than sector-wide.

The outlook into June remains constructive, but the message is not to simply chase beta. The equity market is still willing to fund the AI build-out, and the latest data show that investors continue to reward the areas closest to visible capex. But narrow leadership also reflects unresolved uncertainty about the next stage of the AI paradigm: which incumbents become more valuable, which merely spend to keep up, and which are structurally disrupted. For now, sector investors should stay aligned with AI infrastructure and its physical enablers, while remaining cautious toward large non-AI incumbents whose legacy business models may prove more vulnerable than advantaged.

Disclaimer

This material is for informational purposes only and does not constitute investment advice or a recommendation to buy or sell any security, sector, ETF or strategy. Market views are based on the latest available source data and are subject to change.