Narrations of a Sector ETF Operator

Week Ended March 27: Navigating Stagflation Signals, Conflict Crosscurrents, and AI Disruption

Another risk-off Friday caps a fifth consecutive weekly decline for the S&P 500, with the Nasdaq limping to its tenth down week in the past eleven. The culprit is familiar by now: a toxic cocktail of geopolitical uncertainty, sticky inflation, and a bond market that refuses to cooperate. But beneath the headline malaise, sector rotations are telling a more nuanced story—one with actionable implications for ETF operators willing to look past the noise.

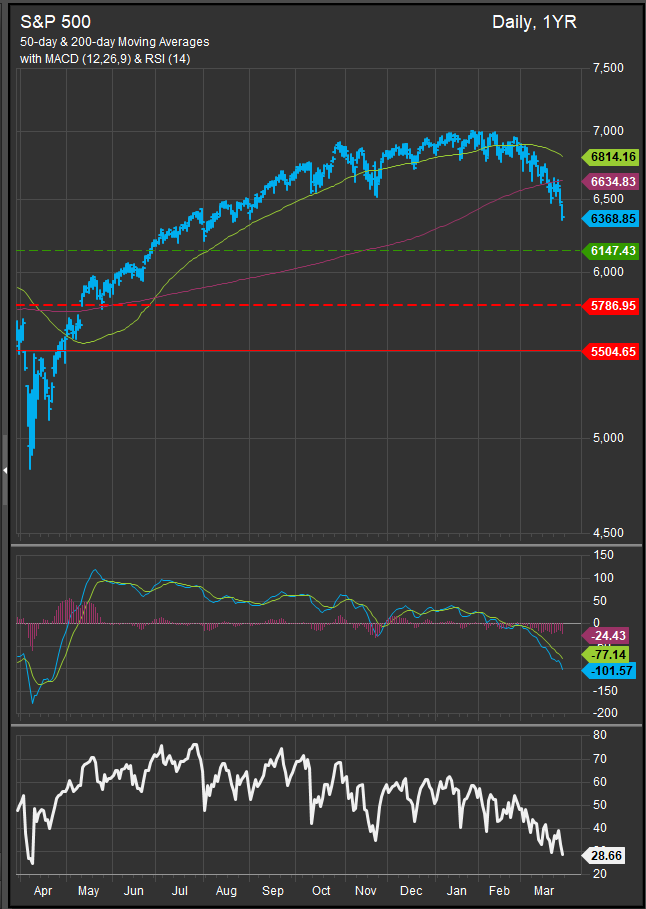

The S&P 500 is below near-term support at the 6500 level. We expect downside likely between the 5786 and 6147 levels.

Real Yields continue to rise in the near-term, pressuring credit sensitive areas of the equity market as well as the consumer more broadly.

Energy: The Obvious Winner, But With Caveats

Energy remains the standout beneficiary of the Iran conflict’s escalation. Crude strength continues to lift the sector, and the fundamental backdrop has only intensified: JPMorgan flagged a 155-million-barrel drawdown in global oil inventories in the first three weeks of March alone, and reports suggest at least 40% of Russia’s export capacity remains offline following Ukrainian drone attacks.

The Strait of Hormuz “tollbooth” dynamic—Iran selectively allowing passage for diplomatic leverage—keeps supply uncertainty elevated. Trump’s latest 10-day extension on threatened strikes against Iranian energy infrastructure buys time but resolves nothing. With 50,000 US troops already in the region and another 10,000 reportedly under consideration, the trajectory remains anyone’s guess.

Positioning idea: XLE and XOP remain the go-to plays, but the risk-reward is getting crowded. For those seeking asymmetric exposure, energy services (XES) and midstream (AMLP) offer leverage to sustained elevated prices without the same degree of headline sensitivity. Keep position sizes disciplined—this is a momentum trade with a binary tail risk.

MLP’s offer income along with exposure to the crude oil trade

Utilities and Staples: Defensive Rotation Has Legs

The week’s sector price action confirmed what the tape has been whispering: investors are rotating into defensives. Utilities and consumer staples were among Friday’s notable gainers, and the logic is straightforward. When bond volatility spikes—the MOVE index has been a widely discussed overhang—and stagflation signals emerge from the PMI data, capital seeks shelter.

The March S&P PMI paints an uncomfortable picture: business activity at an 11-month low, input costs posting their largest sequential increase in ten months, and selling prices rising at the fastest clip since August 2022. S&P’s chief economist flagged data pointing to just 1.0% annualized GDP growth alongside inflation potentially accelerating toward 4%. That’s the stagflation playbook, and it favors sectors with pricing power and stable demand.

Positioning idea: XLU offers the cleanest utility exposure, while XLP captures staples. Within staples, watch for M&A headlines—Unilever’s reported talks to merge its food business with McCormick could spark deal activity across the space. For a barbell approach, pair defensive ETF positions with short-duration bond ETFs (VCSH, JPST) to ride out rate volatility.

Technology: AI Disruption Theme Returns With a Vengeance

The AI disruption narrative roared back this week, and not in a bullish way. Software got hit hard following Anthropic’s computer control announcement—Claude’s new agent capabilities sparked renewed fears of labor and workflow displacement. IGV dropped 4.3% on Tuesday alone, its fifth 4%+ pullback of the year. Memory stocks, which had been AI’s biggest beneficiaries, took collateral damage after Google’s TurboQuant announcement suggested AI models could run on significantly less memory.

This is a classic “second derivative” problem: the market initially bid up everything AI-adjacent, and now it’s repricing which parts of the value chain actually benefit versus which get disrupted. Software-as-a-service names with sticky enterprise relationships may weather the storm better than commoditized players, but the sector remains in a show-me phase.

Positioning idea: Underweight broad software exposure (IGV) for now. If you want AI exposure, focus on infrastructure and compute (SMH for semis, or targeted positions in hyperscalers) rather than application-layer plays vulnerable to displacement. Thoma Bravo’s pushback—that AI disruption fears aren’t yet visible in actual software business performance—is worth noting, but the market is trading the fear, not the fundamentals.

Already discounted to structural support, further selling would set up significant downside targets.

The AI infrastructure trade, proxied here by semiconductor stocks, has been the most resilient throughout the cycle.

Financials: Private Credit Stress Bears Watching

Private credit concerns grabbed headlines again, and the data points are sobering. Investors sought to pull 11.2% from Apollo’s $25B BDC, though the fund’s 5% withdrawal cap limited redemptions. Ares Strategic Income Fund saw $1.2B in redemption requests against $525M returned. FS KKR’s credit rating was cut to junk by Moody’s on asset quality concerns. Blackstone’s flagship BCRED posted its first monthly loss in three years.

Goldman Sachs pushed back, arguing private credit stress is unlikely to generate large macroeconomic spillovers on its own. That may be true in aggregate, but for sector ETF positioning, the optics matter. Traditional bank ETFs (XLF, KBE) could face guilt-by-association pressure even as their direct exposure to private credit varies widely. Regional banks remain the wild card—any credit contagion narrative will hit them first.

Positioning idea: Neutral to underweight financials broadly. If forced to own the space, favor money-center banks (which have the balance sheet strength to weather credit stress) over regionals. Avoid BDC-focused vehicles until redemption pressures stabilize.

Industrials: A Mixed Bag With Supply Chain Undercurrents

Industrials are caught between competing forces. On one hand, conflict-driven supply chain disruptions are accelerating—helium constraints are starting to impact tech supply chains, automakers are reportedly “panic buying” aluminum, and Thailand’s fishing industry is near a standstill due to shipping disruptions. On the other hand, OECD marked up its 2026 US growth forecast partly on stronger-than-expected business investment and AI capex.

The March Richmond Fed Index offered a glimmer of hope, with new orders improving to +4 from -9 and shipments recovering. But the broader PMI picture remains soft, and employment fell for the first time in over a year as firms trimmed overhead.

Positioning idea: Selective exposure here. Aerospace and defense (XAR, ITA) remain structurally supported by the geopolitical backdrop—10,000 additional troops to the Middle East isn’t bearish for defense contractors. Avoid transportation-heavy industrials (IYT) until shipping lane disruptions resolve.

Consumer Discretionary: Resilience Meets Caution

The consumer is bending but not breaking. Bank of America noted total card spending ex-gas slowed only moderately and remained solid at +3.6% y/y. Apollo flagged resilient daily data on airline travel and weekly hotel demand. US oil intensity of GDP is just 1.7% today versus 4.8% in 1974, suggesting the economy can absorb higher energy prices better than historical precedent might suggest.

But the UMich sentiment data tells a different story: final March consumer sentiment fell to 53.3, the lowest since December 2025. Year-ahead inflation expectations jumped to 3.8%, the largest one-month increase since April 2025. The short-run economic outlook plunged 14%. The consumer may still be spending, but confidence is eroding.

Positioning idea: Neutral on XLY for now. The Netflix price hike (Standard plan up 11.1% to $19.99/month) is a useful bellwether—if subscriber growth holds, it signals pricing power. Watch retail closely; JPMorgan’s note that retail investors “sold the rip” on Monday’s bounce (first net selling day in nine months) suggests the buy-the-dip reflex is fading.

Materials: Inflation Beneficiary, But Selectivity Required

Materials benefit directly from the inflation impulse. HB Fuller announced minimum 10% global price increases across all product lines. Dow is implementing a $0.30/lb increase in North American polyethylene prices in April—double prior estimates. Intel and AMD reportedly expect 10-15% price increases amid CPU shortages.

But materials are also exposed to demand destruction if stagflation tips toward recession. The OECD’s cooler 2027 growth forecast (1.7%, down 0.2pp) and the PMI’s employment contraction signal that the growth leg of the stagflation equation is wobbling.

Positioning idea: Favor materials with pricing power and defensive end markets (packaging, agricultural chemicals) over cyclically exposed names. XLB offers broad exposure, but consider more targeted plays like MOO (agribusiness) or PICK (metals and mining) depending on your inflation thesis.

Healthcare: The Forgotten Defensive

Healthcare has flown under the radar amid the geopolitical drama, but the M&A headlines suggest smart money is sniffing around. Merck’s $6.7B acquisition of Terns Pharmaceuticals and Estee Lauder’s reported talks to acquire Puig (albeit more consumer than healthcare) point to boardrooms putting capital to work despite uncertainty.

Healthcare offers defensive characteristics without the rate sensitivity of utilities. With bond volatility elevated and the 30-year mortgage rate at 6.43% (highest in five months), sectors less correlated to duration moves have appeal.

Positioning idea: Overweight XLV as a defensive allocation. Within healthcare, biotech (XBI) remains speculative but could benefit from M&A activity if deal flow accelerates.

The Macro Takeaway

This week crystallized the competing forces shaping sector allocation: stagflation signals favor defensives and inflation beneficiaries (energy, utilities, staples, materials with pricing power), while growth concerns and AI disruption pressure cyclicals and software. Private credit stress adds a financials wildcard. Geopolitics remain the dominant variable, and until the Iran situation resolves—in whatever direction—expect elevated volatility and thin liquidity to persist.

The 35% ETF share of trading volume (per Citadel Securities) reflects active shorting and hedging activity. Clean positioning data from Deutsche Bank (aggregate equity positioning at nine-month lows) and Goldman’s $55B CTA selling since March suggest the market is washed out—but washed out can get more washed out before it reverses.

Position defensively, keep duration short, and stay nimble. The April seasonality tailwind and month/quarter-end rebalancing flows may provide a tactical bounce, but the fundamental picture demands caution until clarity emerges on inflation, conflict resolution, and Fed reaction function.

Sources:

- FactSet StreetAccount – Primary source for all market data, headlines, and talking points referenced throughout the article

- PIMCO – Fixed income ETF trends and flow data pimco.com

- Alpha Ex Capital – Bond ETF liquidity benchmarks alphaexcapital.com