World-Wide Wednesday | Examining the case for US vs. Ex-US Exposure as Investors Price in the End of Hostilities

Potential crowding risk into the domestic AI trade keeps international equities vital to a stable, well-balanced portfolio.

Potential crowding risk into the domestic AI trade keeps international equities vital to a stable, well-balanced portfolio.

Downside risks are re-emerging as geopolitical tensions, rising energy costs, and weakening sentiment reshape markets. Utilities regain appeal as low-volatility income, while Energy and precious metals benefit from inflation and policy uncertainty, driving a shift toward defensive, income-oriented sector positioning.

Since late March, falling Treasury yields have reflected more than softer macro expectations. ETF flows show investors already rotating for easier policy, favoring semiconductors, dividends, infrastructure, and selective real assets, while that very equity rotation may eventually limit how far yields decline.

Factor Friday: Interest Rates in Focus as Factor Leadership is in Potential Transition Read More »

Geopolitical events have equities in correction, but underneath the surface there is a clear ongoing shift towards physical assets and infrastructure.

Thematic Thursday: What ETF Flows Are Telling Us This Week Read More »

COMMENTARY: The S&P 500 declined -2.1% for the week ending March 27, 2026, as markets faced renewed pressure from rising interest rates and persistent inflation concerns. Stronger-than-expected economic data pushed Treasury yields higher, reinforcing expectations that the Federal Reserve may keep policy restrictive for longer. At the same time, a notable rebound in commodity prices—particularly

Performance Summary: Week Ending March 27th, 2026 Read More »

The S&P 500 declined 1.9% for the week, reflecting a combination of macroeconomic uncertainty and geopolitical risk. Energy (+2.8%) was the clear outperformer, benefiting directly from rising crude oil and natural gas prices. Supply disruptions tied to geopolitical conflict pushed oil prices above $100 per barrel during the week, driving strong earnings expectations across the sector. Key contributors included Exxon Mobil and Chevron, which carry significant index weight, along with strength in companies such as ConocoPhillips and EOG Resources. The sector’s performance reflects its leverage to commodity prices, which acted as a hedge against broader market weakness.

Performance Summary: Week Ending March 20th, 2026 Read More »

Growth versus Value leadership hinges on interest rates: rising yields driven by energy-led inflation favor Value, while stable or declining rates support Growth. The decisive factor is whether oil shocks sustain inflation or fade, allowing central banks to maintain or ease policy

Factor Friday: The Interest Rate Lens Driving Factor Leadership Read More »

Geopolitical escalation in the Middle East and rising oil prices are reshaping the macro landscape. While energy and industrial sectors benefit structurally, near-term portfolio strategy favors defensive sectors as investors hedge against inflation risk, credit tightening, and uncertainty surrounding the Iran conflict’s trajectory

March 10, 2026 The rebound in U.S. Growth stocks—particularly across Information Technology and Communication Services—has puzzled many sector investors given the sharp escalation in geopolitical risk surrounding the Iran conflict. Oil prices have surged, volatility has increased, and strategists warn that prolonged conflict could trigger a broader market correction if energy disruptions intensify. Yet despite

Tactical Tuesday: Interpreting the Growth Rally During the Iran Conflict Read More »

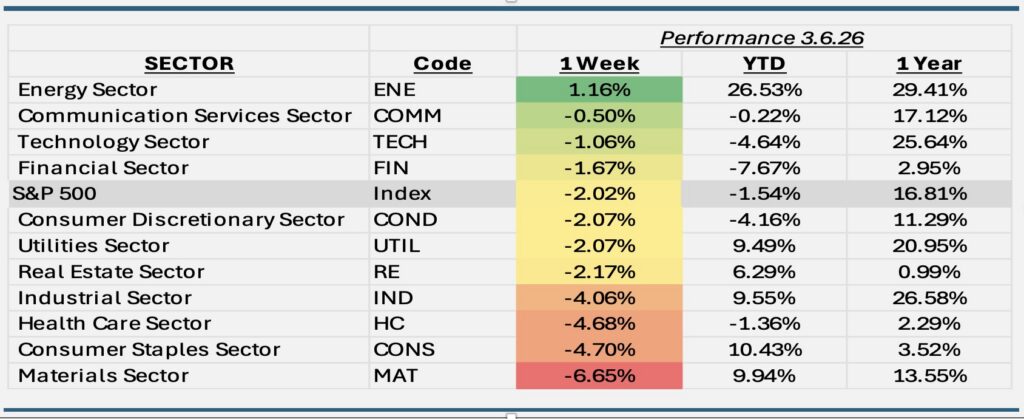

Crude oil surged to its highest level in over two years as the conflict in Iran escalated, raising fears of prolonged supply disruptions. Energy Sector is up 26.53% YTD in 2026.

Weekly Sector Performance Table Read More »